What Happens After You Submit an R&D Claim? The 2026 HMRC Timeline

Is your R&D claim a finished task or a pending strategic asset? Many directors view the submission as the final hurdle, yet the period that follows is often the most critical for your quarterly financial planning. It's understandable to feel a sense of uncertainty or even anxiety whilst waiting for a response, particularly when you consider that approximately 17% of claims underwent compliance checks in the 2023/24 period. You've done the hard work of innovating; now you need to know exactly when that capital will return to your balance sheet.

This article explains exactly what happens after you submit an R&D claim, demystifying the "black box" of HMRC's internal review process for 2026. You'll learn the specific differences between the Merged Scheme and ERIS processing windows, and how to identify whether a routine check is actually a formal enquiry. We provide a clear, week-by-week timeline of the journey from the Additional Information Form review to the final delivery of your tax credit or cash payment, ensuring you can manage your cash flow with absolute professional certainty.

Key Takeaways

- Map out the specific 2026 processing windows for the Merged Scheme and ERIS to understand exactly what happens after you submit an R&D claim.

- Identify the critical role of the Additional Information Form (AIF) as the digital gatekeeper that determines the speed and success of your submission.

- Learn to differentiate between a standard HMRC verification and a formal compliance enquiry to maintain confidence in your financial planning.

- Understand the hierarchy of benefit delivery, including how HMRC prioritises offsetting current tax liabilities before issuing any cash credits.

- Discover how to use the post-submission window to refine your technical narratives and strengthen your position for the next innovation cycle.

The Immediate Aftermath: Verification and the Additional Information Form (AIF)

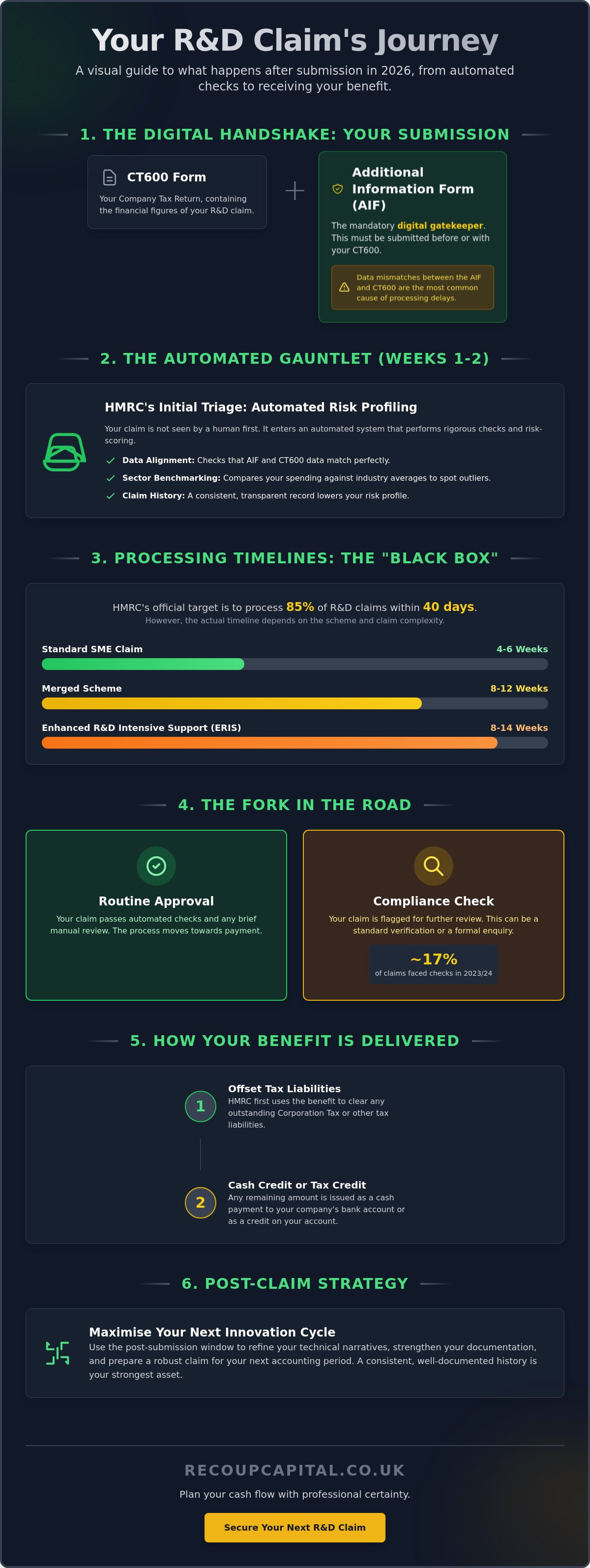

Once you click 'submit' on your Company Tax Return (CT600), the clock begins. But what happens after you submit an R&D claim isn't a manual review by a person immediately. Instead, your submission enters a rigorous, automated verification stage. This phase represents the bridge between your filing and the final HMRC approval. In 2026, this bridge is built almost entirely on the digital data provided in your Additional Information Form (AIF). It's a high-stakes period where the accuracy of your paperwork determines whether you move toward payment or toward a request for further information. The system is efficient. It's designed to process valid claims quickly whilst filtering out those that don't meet the strict criteria of the UK R&D tax incentive scheme.

The Mandatory AIF: Your Claim's Digital Passport

The AIF acts as the digital gatekeeper for your submission. You must submit this form via the government gateway before, or on the same day as, your company tax return. If you miss this step, HMRC's systems will automatically reject the R&D claim. This is a non-negotiable requirement. The AIF requires precise technical narratives that clearly articulate the scientific or technological uncertainty you've addressed. For a deep dive into these requirements, you can view our guide on R&D tax credits explained. The goal is to ensure the financial figures in your CT600 match the qualitative story in the AIF perfectly. A simple data mismatch here is the most common cause of avoidable processing delays.

HMRC Automated Risk Profiling

Whilst your claim sits in the initial processing queue, HMRC algorithms perform sophisticated risk-scoring. They compare your figures against sector-specific benchmarks to identify "outliers". If your expenditure on subcontracted R&D is significantly higher than the average for your industry, the system may flag your claim for closer inspection. Your previous history is equally important. A track record of transparent, accurate submissions lowers your risk profile and can speed up the journey to approval. Consistency in how you categorise your qualifying expenditure (QE) is vital for rapid processing. HMRC looks for logical patterns; sudden, unexplained shifts in your staff costs or consumable spending can trigger a manual review. Understanding what happens after you submit an R&D claim helps you prepare for these automated checks by ensuring your data is robust from the outset. This initial "validity check" is designed to filter out errors before a caseworker ever sees the file.

HMRC Processing Windows: How Long Until You Receive Your Benefit?

The period following your submission is often referred to as the "Black Box" period. This is the window where communication from HMRC typically falls silent, leaving many directors wondering about their cash flow timing. Understanding what happens after you submit an R&D claim requires a clear look at HMRC's internal clock for 2026. Whilst the official target is to process 85% of claims within 40 days, the reality depends heavily on which scheme you've utilised. Standard SME claims usually resolve within 4 to 6 weeks, but if you're filing under the Merged Scheme, you should plan for a window of 8 to 12 weeks. For those qualifying for Enhanced R&D Intensive Support (ERIS), the complexity of the 30% intensity threshold means a timeline of 8 to 14 weeks is more common.

It's important to distinguish between "Processing" and "Payment" status in your HMRC online portal. If your claim is "Processing", it's currently being handled by the automated risk filters or assigned to a caseworker for a manual check. Once the status shifts to "Payment", the technical review is complete and the financial benefit is being prepared for issuance. To ensure your submission moves through these stages without friction, you must submit an additional information form correctly before your tax return is filed. Any mismatch in this digital data can instantly reset your 40-day clock.

The 40-Day Roadmap

- Week 1-2: Your claim undergoes initial automated validation. The system checks that the AIF and CT600 data align and assigns an initial risk score based on industry benchmarks.

- Week 3-5: If your claim is flagged by risk profiles or if you are a first-time claimant, an HMRC R&D caseworker performs a technical review. They assess the narratives to ensure the project meets the definition of scientific or technological advancement.

- Week 6: Upon approval, HMRC calculates the final tax offset. If a cash credit is due, the instruction is sent to the central payment system for issuance.

Why Some Claims Take Longer

Several factors can extend your wait beyond the standard 40-day target. Peak tax seasons, specifically the months following December and March year-ends, see a significant surge in volume that can stretch HMRC resources. First-time claimants also undergo more rigorous manual verification as HMRC establishes a baseline for your business's R&D activities. If you're looking to streamline this process for future cycles, learning how to claim R&D tax credits efficiently can help you avoid common administrative traps that trigger manual delays. If you're currently in the waiting phase and feel concerned about a lack of updates, you can check our frequently asked questions for more specific guidance on typical caseworker behaviour during the "Black Box" period.

The Fork in the Road: Compliance Checks vs Routine Approval

The post-submission phase is rarely a straight line. Once your claim passes the initial automated risk profiling mentioned in previous sections, it reaches a decisive fork in the road. Understanding what happens after you submit an R&D claim means preparing for two distinct outcomes: routine approval or a compliance check. In 2026, HMRC has refined its approach, moving away from immediate forensic audits in favour of "nudge letters" for minor discrepancies. These letters serve as a gentle prompt to review specific data points without triggering a full-scale enquiry. However, if your claim contains significant outliers, such as unusually high subcontractor costs, you may face a formal compliance check. This is where HMRC's approach to handling claims becomes highly structured, prioritising transparency and evidence-based technical narratives.

Signs of a Successful Submission

For many businesses, the first indication of success is a "Notice of Amendment" to your Corporation Tax return. This document confirms that HMRC has accepted your figures and adjusted your tax liability accordingly. You should also keep a close eye on the "View liabilities and payments" section of your HMRC online service. A shift in these figures, often occurring whilst you are still in the 40-day window, is a strong signal that your credit is being processed for issuance. It is a moment of significant capital recovery. If 40 days pass without any direct contact from a caseworker, it typically indicates that your claim has cleared the technical review and is moving toward final payment authorisation. This silence is often the best news a director can receive regarding what happens after you submit an R&D claim.

Navigating an HMRC Enquiry

An enquiry shouldn't be a cause for panic, but it does require a disciplined response. Common triggers in 2026 include vague technical narratives that fail to articulate the scientific or technological advance or inconsistencies in qualifying expenditure. If you receive a formal enquiry notice, you generally have a 30-day window to respond. This is a critical period where the integrity of your claim is tested. Providing robust, project-level evidence is essential to satisfy HMRC's queries and avoid a reduction in your benefit. Because these challenges often target the technical validity of your innovation, having a specialist Enquiry Defence strategy is vital. Professional representation ensures that technical jargon is translated into the specific regulatory language HMRC caseworkers expect, protecting your capital recovery from unnecessary clawbacks. It transforms a potentially intimidating procedure into a manageable step toward your next innovation cycle.

Realising the Value: How Your R&D Benefit is Delivered

After your claim successfully navigates the technical review and risk profiling, the focus shifts to the financial mechanics of delivery. Understanding what happens after you submit an R&D claim is only half the battle; you must also understand how that value actually reaches your balance sheet. HMRC operates a strict hierarchy of benefit delivery. They don't simply issue a cheque for the full amount. Instead, the system is designed to settle any outstanding debts to the Crown before releasing capital to your business. This means your R&D credit will first be used to offset any existing Corporation Tax liabilities for the period in question. If you have already paid your tax bill, this usually results in a rebate for overpayment.

For profit-making SMEs, the benefit is typically a reduction in Corporation Tax. If your innovation has already been accounted for in a paid return, HMRC will process a refund directly to your nominated bank account. Loss-making SMEs have a different path. You may choose to surrender your R&D-linked losses in exchange for a payable cash credit. In 2026, those qualifying for Enhanced R&D Intensive Support (ERIS) can see a cash benefit of up to 27%, whilst those under the Merged Scheme receive a 20% taxable credit. It's a significant injection of liquidity that transforms technical effort into a strategic business asset.

Cash Credits vs Tax Offsets

Identifying the arrival of your benefit is straightforward if you know what to look for. Cash payments in your bank account are often labelled "HMRC Corp Tax" or "HMRC GBS". The actual value you receive depends on your company's specific circumstances and R&D intensity. To see how these figures are calculated for your specific sector, you can view our guide on R&D tax credits explained for UK limited companies. Whether it's a direct payment or a reduction in your next tax bill, the outcome provides essential capital for your next phase of growth. If you are unsure how to account for this credit in your quarterly reports, our team can help you integrate these strategic assets into your wider corporate finance planning.

The RDEC Payment Hierarchy

If your claim falls under the Merged Scheme or the traditional RDEC rules, HMRC follows a rigorous seven-step discharge process. This is more complex than the SME route because the credit is "above the line," meaning it impacts your EBITDA. The process begins by settling the current year’s Corporation Tax. Next, HMRC checks for other outstanding liabilities across the board, including VAT and PAYE arrears. Only after these steps are cleared does the remaining credit move toward a cash payment. This hierarchy ensures that your business is fully compliant with all tax obligations before the innovation incentive is realised. It’s a thorough process, but one that ultimately reinforces the financial stability of your innovating enterprise.

Post-Claim Strategy: Maximising Your Next Innovation Cycle

Whilst understanding what happens after you submit an R&D claim is essential for immediate financial forecasting, the most proactive businesses don't simply wait for the funds to arrive. They view the 40-to-90-day processing window as a strategic interval to refine their internal processes and prepare for the next financial year. The work doesn't stop at submission. It's during this time that you can transform a reactive tax exercise into a proactive innovation strategy. If HMRC provides feedback or raises queries, these shouldn't be seen as hurdles but as a roadmap for improving future technical narratives. This period is your opportunity to ensure that your business is not just claiming for past work, but is structurally optimised for future capital recovery.

By aligning your R&D efforts with other incentives, you can create a compounded financial benefit. For instance, qualifying intellectual property can be further leveraged through the Patent Box, potentially lowering your Corporation Tax to 10% on related profits. Similarly, any physical infrastructure or specialist equipment required for your projects should be reviewed for Capital Allowances. This holistic approach ensures that every pound spent on innovation is working as hard as possible for your bottom line.

Establishing a Real-Time Documentation Culture

The most successful claimants move away from the "year-end scramble" and adopt a monthly innovation tracking habit. Identifying new qualifying projects whilst your previous claim is still in the HMRC queue keeps the momentum high and ensures no technical detail is lost to time. It's much easier to capture the nuances of a scientific uncertainty as it happens rather than trying to reconstruct it twelve months later. Recoup Capital helps you maintain this "always-ready" compliance posture by providing structured frameworks for technical logs. This discipline reduces the administrative burden of future filings and significantly lowers your risk profile in the eyes of HMRC caseworkers. You're no longer just filing a report; you're building a transparent record of business growth.

The Power of Capital Recovery

It's time to reframe your R&D refund. It isn't a simple rebate or a windfall; it's a strategic growth fund designed to be reinvested into your next breakthrough. Whether you're exploring Land Remediation Relief for a new site or hiring specialist engineers, this capital provides the liquidity needed for rapid scaling. A success-based partnership with a specialist ensures that you can pursue these claims with zero-risk continuity, as your interests are perfectly aligned with the result. Ultimately, knowing what happens after you submit an R&D claim allows you to plan with confidence. It transforms a complex regulatory transaction into a long-term growth engine that fuels your company's competitive edge in the marketplace.

Turning Capital Recovery into Sustainable Growth

Navigating the "black box" period with confidence requires more than just patience; it demands a clear understanding of HMRC's 2026 procedural landscape. By mastering the nuances of the Additional Information Form and aligning your internal logs with caseworker expectations, you remove the friction from your capital recovery. Understanding exactly what happens after you submit an R&D claim is the key to turning a complex regulatory requirement into a predictable, strategic cash flow event for your business.

The journey doesn't have to be a source of anxiety. Our team of chartered tax accountants and technical specialists provides a protective guide through the complexities of HMRC's evolving standards. With a proven track record in high-value enquiry defence and a commitment to success-based fees, we ensure that your interests are always the priority. We only win when you do. It's time to stop viewing your tax credit as a mere refund and start seeing it as a strategic asset for your next breakthrough. Secure your innovation capital with Recoup Capital’s expert R&D specialists and take the first step toward a partnership that values your long-term growth as much as you do. Your next era of innovation is within reach.

Frequently Asked Questions

How do I know if HMRC has received my R&D claim?

You will know HMRC has received your claim when you receive an automated confirmation receipt via your Government Gateway account. This occurs immediately after you file your CT600 and Additional Information Form (AIF). This digital receipt is the first step in what happens after you submit an R&D claim, providing the reference numbers needed for any future correspondence with caseworkers.

Can HMRC change the amount of my R&D tax credit after I submit?

Yes, HMRC has the authority to adjust the credit amount if they determine that certain costs don't meet the qualifying criteria or if the technical narrative lacks sufficient depth. This usually happens during a formal enquiry where caseworkers might challenge the scientific or technological advancement. Having robust, contemporaneous documentation is the most effective way to protect your original valuation and ensure full capital recovery.

What happens if I made a mistake on my R&D submission?

If you discover an error, you can usually amend your Company Tax Return (CT600) within 12 months of the filing deadline. It’s vital to act quickly once a mistake is identified. Making a voluntary disclosure before HMRC identifies the error often results in significantly lower penalties and demonstrates a commitment to transparency, which can help maintain your company's low-risk profile for future innovation cycles.

Will an R&D claim trigger a full audit of my business tax affairs?

An R&D enquiry is typically ring-fenced to the specific technical and financial details of your claim rather than your entire business. Whilst HMRC has the power to look at other areas, a routine check into your innovation projects rarely triggers a full forensic audit of your entire tax history. They're primarily interested in the validity of the technical uncertainties and the associated qualifying expenditure you've identified.

How does the 2026 R&D intensity threshold affect my payment?

For accounting periods starting on or after April 1, 2024, the R&D intensity threshold is 30%. If your qualifying expenditure meets or exceeds this percentage of your total business spending, you qualify for Enhanced R&D Intensive Support (ERIS). This allows loss-making SMEs to claim a higher payable credit of 14.5%, which can result in a total cash benefit of up to 27% of your R&D spend.

What is the "Notice of Enquiry" and what should I do if I get one?

A Notice of Enquiry is a formal letter from HMRC stating they've opened a check into your claim. You shouldn't panic, but you must respond within the stated timeframe, usually 30 days. This is a critical stage in what happens after you submit an R&D claim, so it's vital to engage a specialist who can handle the technical correspondence and translate your innovation into the specific regulatory language caseworkers expect.

Can I track the status of my R&D claim online?

You can monitor progress through the "View liabilities and payments" section of your HMRC online services. Whilst it won't provide a minute-by-minute update, you'll see when your tax return has been amended or when a payment has been authorised. If your status remains "Pending" beyond the standard 40-day window, it often suggests the claim has been assigned to a caseworker for a manual technical review.

Why has my R&D payment been used to pay off my VAT bill?

HMRC operates a strict hierarchy of debt recovery before releasing any cash to your bank account. They'll automatically use your R&D credit to settle any outstanding tax liabilities, including VAT, PAYE, or previous Corporation Tax arrears. This ensures the business is fully compliant before receiving the remaining incentive as a strategic cash injection. Once these debts are cleared, the surplus is issued as a direct payment.