Patent Box vs R&D Tax Credits: A Strategic Comparison for UK Innovation in 2026

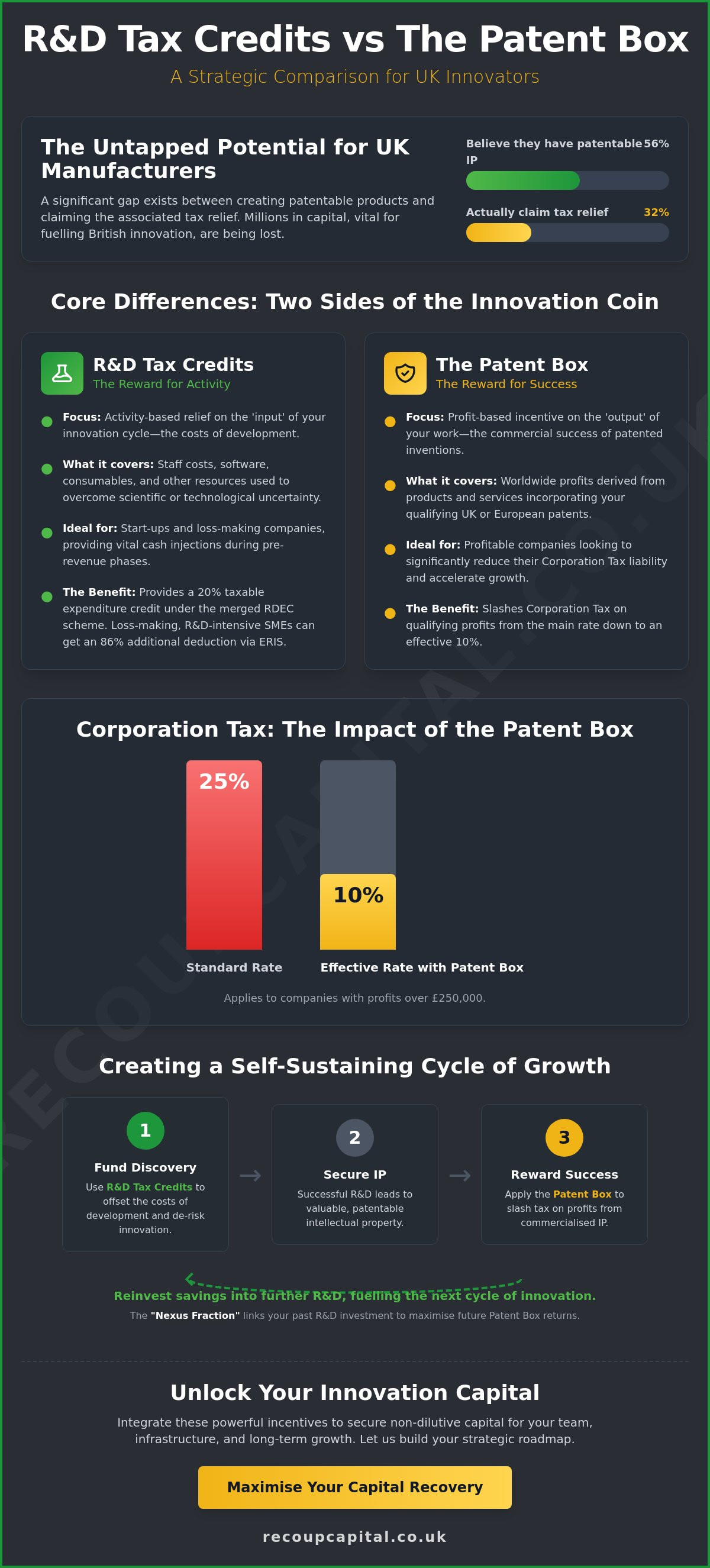

Did you know that whilst 56% of UK manufacturers believe they have created patentable products, only 32% have actually claimed the tax relief they deserve? This gap represents millions in lost capital that could be fueling British innovation. It is a common frustration for ambitious directors; you are working hard to innovate, yet a 25% Corporation Tax rate continues to swallow the budgets you need for hiring and infrastructure.

When weighing up patent box vs r&d tax credits, the complexity of managing multiple schemes can feel overwhelming, especially with the fear of HMRC scrutiny during a transition. This article will show you how to balance these incentives to significantly reduce your tax liability and generate the non-dilutive capital required for sustainable scaling. We will break down which scheme yields the highest ROI for your specific stage of growth and provide a clear roadmap for integrating IP protection into your broader financial strategy for 2026. You will discover how R&D tax credits fund the process of discovery whilst the Patent Box rewards the success of commercialisation, creating a self-sustaining cycle of growth.

Key Takeaways

- Understand the fundamental shift between activity-based R&D relief for your development costs and profit-based incentives for your commercialised intellectual property.

- Discover how a combined strategy for patent box vs r&d tax credits can slash your Corporation Tax to an effective rate of 10% on qualifying profits.

- Learn to calculate the "Nexus Fraction" to ensure your past R&D investments are working hard to maximise your future Patent Box returns.

- Recognise the strategic inflection point where shifting your focus toward IP-based relief accelerates business valuation and long-term scaling.

- Gain a clear roadmap for integrating these incentives to secure non-dilutive capital for reinvesting in your team and infrastructure.

The Innovation Funding Landscape: Patent Box vs R&D Tax Credits in 2026

The UK tax system offers two powerful levers to support your business growth. One focuses on the costs you incur during development, whilst the other rewards the profits you generate from those successes. Understanding the interplay of patent box vs r&d tax credits is no longer just a task for your accountant; it's a vital part of your 2026 growth strategy. With the main rate of Corporation Tax holding steady at 25% for companies with profits over £250,000, these incentives provide the liquidity needed to scale without diluting your equity.

We view these tax savings as "Innovation Capital." This isn't just a tax refund; it's a strategic reinvestment fund. By reclaiming cash from HMRC, you're effectively creating a non-dilutive stream of finance to hire top-tier engineers or upgrade your infrastructure. It's about turning a compliance requirement into a competitive advantage.

The Purpose of the UK Patent Box Regime

The government established the UK Patent Box scheme to ensure that the intellectual property (IP) created here stays here. It encourages companies to not only invent in Britain but also to keep the manufacturing and commercialisation of those inventions on home soil. If your company owns or has an exclusive licence for a qualifying patent, you can benefit from an effective Corporation Tax rate of just 10% on the profits derived from those patented products.

This 10% rate is a game-changer for tech and engineering firms. It provides a massive competitive edge, allowing you to retain more profit to drive further R&D. It represents the "output" side of the innovation cycle, rewarding the commercial success of your ingenuity and keeping the UK at the forefront of global technology.

The Enduring Value of R&D Tax Relief

Whilst the Patent Box looks at profits, R&D tax relief focuses on the "doing." It's often the first step in a company’s innovation journey. Under the current R&D tax credits explained framework, most companies now claim under the merged RDEC scheme, which offers a 20% taxable expenditure credit. For loss-making, R&D-intensive SMEs, the Enhanced R&D Intensive Support (ERIS) provides even deeper relief with an additional 86% deduction.

R&D credits support you when you're taking risks. They offset the costs of staff, software, and consumables used in the pursuit of a technical breakthrough. Whether you're a startup or an established manufacturer, these credits provide the early-stage fuel that eventually leads to the patentable IP rewarded by the Patent Box. Together, they cover the entire lifecycle of a product, from the first prototype to the final sale.

Core Differences: Activity-Based Relief vs Profit-Based Incentives

Choosing between patent box vs r&d tax credits isn't a matter of "either/or" but rather a question of timing and focus. R&D tax credits are activity-based, meaning they focus on the "input" of your innovation cycle. This includes the salaries of your technical team, software costs, and materials consumed during the development process. In contrast, the Patent Box is profit-based. It rewards the "output" of your hard work, specifically the commercial success of your patented inventions.

This distinction is vital for cash flow management. R&D credits are a lifeline for loss-making startups, providing cash injections that can keep the lights on during the pre-revenue phase. The Patent Box, however, requires your company to be profitable. It doesn't provide a cash refund in the same way; instead, it slashes the Corporation Tax rate on qualifying profits from the main rate of 25% down to an effective 10%. Whilst R&D credits cover the cost of discovery, the Patent Box covers the global sales of the final product.

Eligibility Criteria: Who Can Claim What?

To qualify for R&D tax relief, your project must seek to achieve an advance in science or technology by resolving "Scientific or Technological Uncertainty." It's about the technical challenge, not just the novelty of the product. For the Patent Box, the barrier is different. You must own or exclusively licence "Qualifying Intellectual Property," which typically means a patent granted by the UK Intellectual Property Office or the European Patent Office. For businesses involved in development and construction, Land Remediation relief can also play a role if you're bringing blighted land back into use. If you're unsure where your project sits, our specialists can help you identify your eligibility across these various schemes.

Financial Impact: Calculating the Benefit

The net benefit varies significantly based on your business model. Consider a profitable firm with a £1m turnover. If that firm has high development costs but low patentable profit, R&D credits will likely yield the higher ROI. However, as that product goes to market and generates high-margin sales, the Patent Box's 10% tax rate becomes incredibly lucrative.

HMRC applies a "Nexus" requirement to ensure these benefits aren't exploited. This rule links the tax relief directly to where the underlying R&D was performed. To get the full 10% rate, the majority of the development work must have been conducted within the UK. Forensic accounting is essential here to separate qualifying revenue from non-qualifying streams, ensuring every penny of profit is correctly attributed to the patent.

The Power of the Nexus: Using Both Incentives to Compound Growth

Treating these incentives as separate silos is a missed opportunity for strategic growth. When comparing patent box vs r&d tax credits, it is essential to realise they are designed to work in tandem. You don't have to choose one over the other; in fact, the UK tax system rewards those who use both. This synergy allows you to claim R&D relief for the development phase whilst simultaneously applying the Patent Box's 10% tax rate to the resulting profits. It's a dual-track approach that secures your financial present and your innovative future.

The technical bridge between these two schemes is the "Nexus Fraction." This calculation ensures that the tax benefit is directly proportional to the amount of R&D work actually performed by your company. HMRC requires absolute clarity in how these figures are derived, particularly in the current climate of HMRC R&D tax claim transparency and AI compliance. By linking your R&D expenditure to your patent profits, you create a robust, evidence-based claim that stands up to scrutiny.

The Virtuous Cycle of Innovation Funding

R&D claims provide the immediate cash flow needed to file and defend patents, which then unlocks the long-term 10% tax rate on commercial success. This cycle creates a financial "moat" around your business. You use tax savings to fund more R&D, which leads to more patents, which in turn lowers your Corporation Tax bill again. It is a self-sustaining engine for non-dilutive capital. To make this work, your technical documentation must be impeccable. Bridging the gap between your engineering teams and your IP department ensures that every technical breakthrough is captured for both an R&D claim and a potential patent application.

Optimising the Nexus Fraction

In plain English, the Nexus Fraction is a ratio that compares your in-house R&D costs against your total R&D spend, including outsourced work and IP acquisition. The higher your in-house activity, the higher your fraction, and the more profit you can shield at the 10% tax rate. We recommend organising your R&D activities to favour in-house development where possible to maximise this future benefit. General accountants often miss this interplay, failing to see how a decision about outsourcing today could negatively impact your Patent Box claim three years from now. A specialist perspective ensures your operational decisions are aligned with your long-term tax efficiency.

Implementation Strategy: When to Prioritise Patent Box over R&D Credits

Timing is everything in corporate finance. When you're weighing up the benefits of patent box vs r&d tax credits, you're essentially mapping out your company's future. There is a distinct "inflection point" where the focus shifts. This usually happens when your R&D expenditure begins to level off and your commercial profits from that innovation start to climb. At this stage, the 10% Corporation Tax rate offered by the Patent Box becomes your most potent tool for capital retention.

For many UK firms, particularly in the manufacturing and engineering sectors, this transition is transformative. It moves the conversation from merely recovering costs to maximising profit. This shift is a key component of a robust corporate finance strategy. It allows you to demonstrate to investors that your innovation is not just technically sound but also fiscally optimised for long-term scaling.

Lifecycle Planning for Innovative Firms

Your tax strategy should evolve alongside your product. We typically see this progression in three distinct phases:

- Phase 1: Seed and Startup. Your primary goal is survival and continued development. You should focus heavily on R&D tax credit claims to maximise cash flow and preserve your runway.

- Phase 2: Growth. As your technology matures, you begin filing patents. This is the time to start tracking your Nexus data meticulously, ensuring your internal processes are ready for a future Patent Box election.

- Phase 3: Maturity. Your product is in the market and generating significant revenue. You now utilise the 10% Patent Box rate to shield profits, using that retained capital to reinvest in your next cycle of R&D.

The Strategic Value of Intellectual Property

Adopting a "Patent-First" culture does more than just lower your tax bill; it builds a more disciplined business. By seeking patents early, you create a tangible asset that significantly increases your company's valuation. This is incredibly attractive to venture capital and private equity firms who want to see protected, high-margin revenue streams. It all starts with a solid foundation, which is why claim R&D credits in the first place. You're building the evidence base that proves your technical advancements are unique and valuable.

By integrating IP protection into your tax strategy, you're turning regulatory requirements into a engine for growth. If you're ready to see how these schemes can work together for your business, you can assess your potential returns with our expert team today.

Maximising Your Capital Recovery with Recoup Capital’s Strategic Partnership

Navigating the transition from development to commercialisation requires more than just a standard accounting service. It demands a partner who understands the "whole picture" of innovation capital. At Recoup Capital, we act as a protective guide through the complexities of the UK tax landscape, ensuring that your journey between patent box vs r&d tax credits is seamless and fiscally optimised. Our team of Chartered Tax Accountants brings the technical depth necessary to handle the rigorous requirements of the Patent Box, transforming what could be an intimidating regulatory procedure into a motivated opportunity for growth.

We believe in demonstrating value through results rather than traditional sales pitches. This is why we operate on a success-based fee model, aligning our interests directly with yours. By lowering the barrier to entry, we enable ambitious firms to explore these incentives without upfront financial risk. Choosing R&D tax credit specialists in the UK who also possess a deep mastery of intellectual property is vital for maintaining compliance whilst maximising your total capital recovery.

A Holistic Approach to Tax Efficiency

Our methodology goes beyond simple claim preparation. We take a forensic approach to identifying qualifying income that generalist accountants often overlook, ensuring that every penny of profit derived from your IP is taxed at the lower 10% rate. We also look for synergies with other incentives, such as Capital Allowances, to create a comprehensive strategy that protects your cash flow from every angle. This relationship-first approach is built on long-term collaboration; we aren't just here for a one-off transaction, but to support your innovation cycle as it evolves over the coming years.

Securing Your Future Growth

A properly structured tax strategy is a significant strategic asset. Beyond the immediate tax savings, a robust Patent Box claim significantly enhances your company's valuation during future corporate finance events. Potential investors or buyers view a 10% effective tax rate and a protected IP portfolio as indicators of high-quality, sustainable earnings. We take full responsibility for defending your claims against HMRC enquiries, providing the peace of mind that comes with 100% compliance.

By unlocking this internal capital, we help your business scale without the need for dilutive external funding. It is about turning your tax department into a profit centre. If you are ready to transform your innovation into a strategic financial tool, the next step is simple. Book a no-cost strategic innovation assessment with Recoup Capital and let us help you secure the capital your ingenuity deserves.

Secure the Capital Your Ingenuity Deserves

Mastering the synergy of patent box vs r&d tax credits is more than a tax exercise; it's a fundamental shift in how you fund your company's future. By bridging the gap between development costs and commercial profits, you create a self-sustaining cycle of non-dilutive capital. You've seen how the 10% effective tax rate can transform your bottom line once your IP matures, and how R&D relief provides the essential runway to get there.

With over 1,000 successful claims processed across the UK, our team of Chartered Tax Accountants and technical experts is ready to act as your protective guide. We operate on a success-based fee model to ensure our interests are perfectly aligned with your growth. It's time to stop leaving innovation capital on the table and start treating your tax returns as strategic assets.

Unlock your growth capital with a professional R&D and Patent Box assessment from Recoup Capital. We're here to help you navigate the complexities of 2026 regulations and turn your technical breakthroughs into long-term business success.

Frequently Asked Questions

Can I claim both R&D tax credits and Patent Box relief at the same time?

Yes, you can absolutely claim both incentives simultaneously for the same product or project. They are designed to be complementary; R&D tax credits offset the costs of development whilst the Patent Box reduces the tax on the resulting profits. Using them together is the most effective way to maximise your total capital recovery throughout the entire innovation lifecycle.

Does the Patent Box only apply to UK patents?

The scheme isn't restricted solely to patents granted by the UK Intellectual Property Office. You can also qualify if your patent is granted by the European Patent Office or specific national offices within the European Economic Area. This allows businesses with a broader international IP strategy to still benefit from the UK's competitive 10% Corporation Tax rate.

How much can I actually save with the Patent Box compared to R&D credits?

When comparing patent box vs r&d tax credits, the savings depend on whether you're spending on development or earning from sales. R&D credits provide a benefit of up to 20% on your qualifying expenditure. The Patent Box slashes your Corporation Tax rate from 25% down to 10% on qualifying profits. For high-margin products, the Patent Box often yields a larger long-term financial gain.

Do I need to be a profitable company to benefit from the Patent Box?

You generally need to be making a taxable profit to see the immediate benefits of the Patent Box. Unlike R&D tax credits, which can provide a cash payment to loss-making startups, the Patent Box works by reducing the amount of tax you pay on earned income. If your company is currently pre-revenue or loss-making, R&D credits are usually the better tool for preserving your cash runway.

What is the "Nexus Fraction" and why does it matter for my claim?

The Nexus Fraction is a mandatory ratio that determines how much of your profit qualifies for the 10% tax rate. It compares your in-house development costs against your total R&D spend, including outsourced work and IP acquisitions. If you perform most of your innovation in-house in the UK, your fraction remains high, allowing you to shield more of your profit from the standard tax rate.

Can software companies claim Patent Box relief?

Software companies can claim Patent Box relief provided their software is protected by a qualifying patent. Whilst obtaining software patents can be complex in the UK, it's increasingly common for technical breakthroughs in AI, cryptography, and data processing. If your software solves a specific technical problem and meets the IPO's criteria, it can unlock significant tax savings on your global sales.

How long does it take for a Patent Box claim to be processed by HMRC?

HMRC doesn't have a separate processing window for the Patent Box like the 28-day target for R&D claims. Instead, the relief is claimed as part of your annual Corporation Tax return (CT600). This means the processing time aligns with your standard tax filing cycle. It's vital to have your forensic accounting and technical evidence prepared well in advance of your filing deadline to ensure a smooth submission.

What happens if my patent is still "pending" - can I still claim?

You can't receive the 10% tax rate whilst your patent is still pending, but you can elect into the scheme to protect your future rights. Once the patent is granted, you're allowed to claim for the profits you made during the pending period, going back up to four years. This ensures that the long wait for patent approval doesn't result in you losing out on valuable tax relief.