Subcontractor Costs for R&D Tax Credits: A 2026 UK Compliance Guide

In 2026, the success of your claim isn't determined by the size of your invoice, but by the "intent" written into your contracts before a single hour of work began. It's a significant shift that has left many firms feeling uncertain about how to handle subcontractor costs for R&D tax credits under the new Merged Scheme. You've likely spent years navigating the old SME and RDEC rules, and the fear that a simple categorisation error could trigger an HMRC enquiry is a valid concern for any forward-thinking business.

We understand that distinguishing between subcontractors and Externally Provided Workers (EPWs) feels more complex than ever. This guide is designed to transform that confusion into a strategic advantage, helping you master the new regulations to ensure your expenditure is both compliant and fully maximised. We will provide a clear framework for documenting R&D intent in your contracts and a detailed breakdown of qualifying costs, giving you the confidence that your next claim will withstand the highest levels of scrutiny.

Key Takeaways

- Understand how the unified Merged Scheme affects your claim rates and simplifies compliance for businesses of all sizes.

- Distinguish between subcontractors and Externally Provided Workers (EPWs) to avoid common categorisation errors in your CT600 filing.

- Learn to apply the "intended R&D" test to ensure your business retains the right to claim subcontractor costs for R&D tax credits.

- Identify the narrow exceptions to overseas expenditure restrictions that could still allow non-UK R&D activities to qualify for relief.

- Discover a forensic approach to documenting R&D intent in your contracts, creating a claim that is both maximised and robust against enquiry.

Navigating the Merged R&D Scheme: How Subcontractor Rules Changed

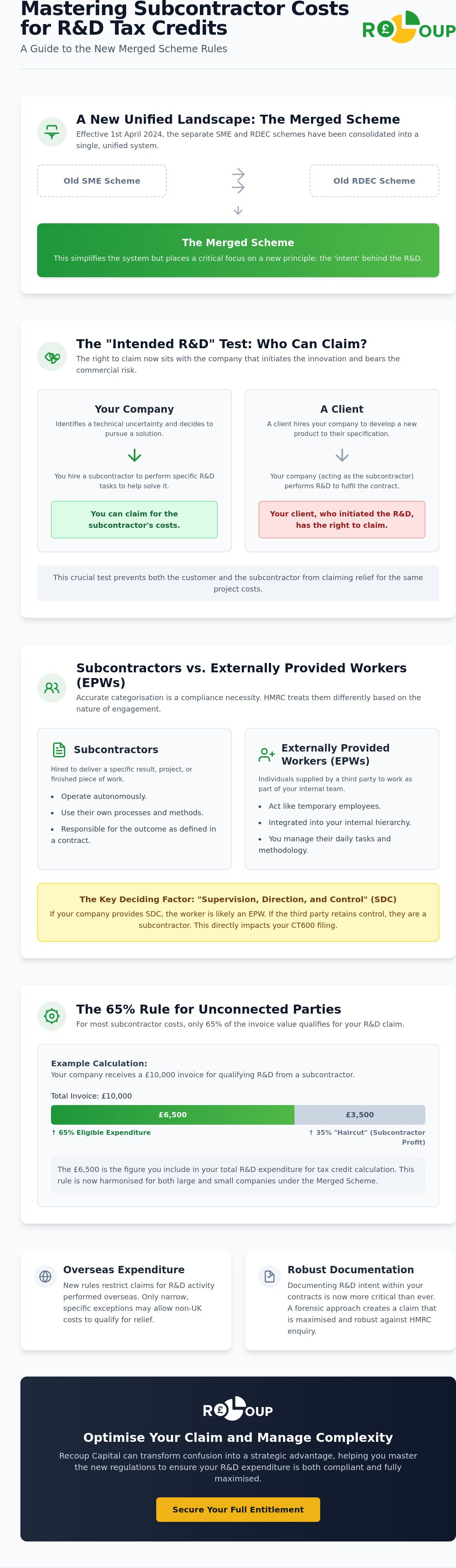

The UK's UK Corporation Tax system underwent a significant transformation on 1 April 2024. The previous SME and RDEC schemes were consolidated into a single, unified Merged Scheme. This transition was designed to simplify the landscape, yet it introduced fresh complexities for those claiming subcontractor costs for R&D tax credits. In the 2026 regulatory environment, the definition of "subcontracted R&D" focuses heavily on who initiates the innovation. If your business identifies a technical uncertainty and hires a third party to solve it, you are likely the party eligible for relief.

Subcontractor costs are payments made to a third party to perform specific R&D tasks on your behalf. The primary goal of the new rules is to prevent double-claiming on the same project. Historically, both the hiring company and the subcontractor might have attempted to claim for the same activity, leading to administrative friction and tax leakage. Under the Merged Scheme, the right to claim generally sits with the company that "intended or contemplated" the R&D before the work began. This ensures that the entity bearing the commercial risk and driving the innovation receives the financial reward.

The 65% Rule: What Remains for Unconnected Parties

For most claims involving unconnected subcontractors, the "65% rule" remains a cornerstone of the calculation. HMRC applies this 35% reduction, often called a haircut, to account for the subcontractor's profit margin. The government's objective is to subsidise the actual R&D expenditure rather than the markup applied by the service provider. This standardised approach provides a predictable framework for businesses to estimate their potential returns.

Consider a practical example. If your company receives a £10,000 invoice for qualifying R&D work from an unconnected software house, the calculation is straightforward:

- Total Invoice Value: £10,000

- Qualifying Percentage: 65%

- Eligible Expenditure: £6,500

This £6,500 is the figure you'll include in your overall R&D expenditure total when calculating your tax credit.

The Shift in Eligibility for Large vs Small Companies

The Merged Scheme has effectively levelled the playing field for subcontractor claims. Previously, large companies operating under the RDEC scheme faced significant restrictions when claiming for work performed by subcontractors. This often created a disparity between small and large innovators. Today, the rules are largely harmonised, meaning larger entities can now claim for 65% of their qualifying subcontractor costs just like their smaller counterparts.

This shift is a vital part of how R&D tax credits explained for the 2026 landscape reflect a more equitable system. It encourages larger businesses to collaborate with specialised third parties without losing out on tax efficiency. Whilst the administrative burden has increased through the mandatory Additional Information Form, the consistency across company sizes allows for more robust long-term financial planning and capital recovery strategies.

Defining Subcontractors vs EPWs: Which Costs Qualify?

Accurately identifying subcontractor costs for R&D tax credits is more than a clerical task; it's a compliance necessity. Whilst both subcontractors and Externally Provided Workers (EPWs) represent third-party expenditure, HMRC treats them differently based on the nature of the engagement. A subcontractor is typically hired to deliver a specific result or a finished piece of work. In contrast, an EPW is an individual provided by a third party to work as part of your internal team, effectively acting as a temporary employee for the duration of the project.

The distinction is vital when Navigating the Merged R&D Scheme. It centres on the concept of "supervision, direction, and control" (SDC). If your company manages the worker’s daily tasks, dictates their methodology, and integrates them into your internal hierarchy, they are likely an EPW. If the third party operates autonomously to meet a contractual specification using their own processes, they are a subcontractor. This categorisation directly impacts how you report figures on your CT600 and the supporting evidence required to withstand an enquiry.

Common examples of EPWs in the engineering and tech sectors include:

- Contract software developers integrated into your agile development cycles.

- Agency-supplied laboratory technicians supporting internal experiments.

- Temporary CAD technicians working under the direct instruction of your lead engineer.

Qualifying Expenditure for Externally Provided Workers (EPWs)

For EPWs, the 65% rule applies to the payment made to the staff provider or agency. To qualify, the worker must be supplied to your company by a third party under a contract. It's essential that the worker is not already an employee of your firm or a person with a contract of service with you. The key requirement is that the worker must be under your company’s supervision and control whilst performing the R&D. If you're unsure how to categorise your team's hybrid working arrangements, it's often helpful to review the specific criteria for claiming R&D tax credits before finalising your figures.

When a Specialist is a Subcontractor

Subcontractors are defined by their autonomous nature. They are experts engaged to solve a specific problem that your internal team cannot address. In the construction sector, for example, hiring a specialist firm to conduct complex soil analysis or structural stress testing constitutes subcontracted R&D. The specialist firm uses its own equipment and expertise to provide a technical report or solution. This differs from hiring general site labour through an agency, where those workers simply follow your foreman's instructions. In the subcontractor scenario, you are paying for a specialised outcome, not just hours of labour.

The 'Intended R&D' Test: Determining Who Can Claim

One of the biggest myths in the 2026 landscape is that the entity performing the technical work is automatically entitled to the tax relief. Under the Merged Scheme, the right to claim is determined by who "intended" the innovation at the point of contract. HMRC's "intended R&D" test is now the primary filter for eligibility, shifting the focus from the activity itself to the commercial decision-maker behind it. If your business identifies a technical uncertainty and hires a specialist to solve it, you are the party that "contemplated" the R&D, making you the rightful claimant for those subcontractor costs for R&D tax credits.

HMRC identifies the claimant by looking for the party that initiated the project and bears the ultimate financial risk. In complex multi-tier supply chains, this usually points to the customer at the top of the chain. Establishing this intent for claiming R&D tax credits should happen during the project’s discovery phase, not as an afterthought during year-end accounting. By aligning your project roadmap with the technical uncertainties you expect to face, you create a clear audit trail. This proactive approach is essential for Defining subcontractor costs and ensuring they are correctly attributed from day one.

Contractual Evidence: Protecting Your Claim

Contracts must do more than just outline deliverables; they need to reflect the R&D journey. Relying on standard "work for hire" or IP assignment clauses is often insufficient for HMRC. Your Master Service Agreements (MSAs) should explicitly mention the "resolution of scientific or technological uncertainties." Using specific terminology, such as "experimental development" or "technical feasibility studies," helps demonstrate that both parties understood the innovative nature of the work from the start. This documentation acts as a protective shield for your claim during an enquiry.

The Subcontractor’s Perspective: When Can They Claim?

Can a subcontractor ever claim? It's rare, but it happens. If a customer hires a specialist for a routine task, but the specialist discovers a technical hurdle the customer didn't anticipate, a "knowledge gap" exists. If the subcontractor then decides to solve this hurdle through their own internal R&D, they might have a valid claim. However, you must be extremely cautious. "Double dipping", where both the customer and the subcontractor claim for the same activity, is a major red flag for HMRC. Transparency between partners is the best way to avoid conflicting filings.

Overseas Restrictions and Connected Parties: Avoiding Pitfalls

The rules surrounding subcontractor costs for R&D tax credits became significantly more restrictive on 1 April 2024. One of the most impactful changes is the clampdown on overseas expenditure. HMRC now prioritises innovation that occurs within the UK, meaning that payments to non-UK subcontractors are generally excluded from your claim. If you've historically relied on international talent to drive your R&D, you must now demonstrate that your choice of location was a necessity rather than a cost-saving exercise. It's a high bar to clear, and documentation is your only defence.

To qualify for an exception, you must meet the "wholly unreasonable" test. This requires proving that the R&D could not have been performed in the UK due to specific geographical, environmental, or social conditions. For instance, conducting clinical trials for a specific population or testing hardware in extreme climates not found in Britain would likely qualify. However, a lack of local skilled labour or higher UK salary costs are explicitly rejected as valid reasons. If your project relies on international expertise, it's vital to speak with a specialist to verify if your overseas costs meet these narrow criteria.

Connected Subcontractors: The "Lower of" Rule

When you engage a "connected" party, such as a subsidiary or a sister company within the same group, the "65% rule" mentioned earlier no longer applies. Instead, HMRC uses the "lower of" rule. This means your claim is limited to either the payment made to the subcontractor or the actual "relevant expenditure" incurred by that subcontractor. Essentially, you cannot include the profit margin the connected company adds to the invoice. The government's goal here is to prevent groups from artificially inflating claims through internal markups.

To remain compliant, you need a clear breakdown of the subcontractor’s underlying costs. Your documentation should include:

- Direct staff costs, including salaries, NIC, and pension contributions.

- Software licences used specifically for the R&D project.

- Consumable items transformed or used up during the R&D process.

- Payments the connected party made to its own unconnected subcontractors, which are then subject to the 65% rule.

Under Generally Accepted Accounting Practice (GAAP), these payments must be brought into account within 12 months of the end of the accounting period to be eligible. Keeping detailed records of these internal costs is non-negotiable for a successful claim. If your group structure involves multiple entities collaborating on innovation, you'll need a robust inter-company accounting process to withstand an HMRC enquiry.

Optimising Your Claim: How Recoup Capital Manages Complexity

Recoup Capital operates with a clear, results-oriented philosophy. We don't believe in traditional sales pitches; we prefer to demonstrate our value through the tangible capital we recover for our partners. Identifying and documenting subcontractor costs for R&D tax credits is a forensic exercise that requires both technical insight and financial precision. Our success-based approach means we're fully invested in the accuracy and maximisation of your claim from the very first consultation. By viewing these credits through the lens of corporate finance, we help you reframe tax relief as a strategic asset for long-term business innovation.

Expertise matters when dealing with HMRC’s increasingly stringent compliance standards. Our team includes chartered tax accountants who understand the nuances of the Merged Scheme and the specific triggers for enquiry. We act as your professional shield, handling all technical queries and providing the authoritative voice required to justify complex expenditure. This relationship-first approach ensures that you can focus on your core business whilst we manage the intricate details of your claim.

Our Methodology: From Technical Assessment to Submission

Our process starts with a deep dive into your project's technical reality. We don't just look at invoices; we review the Master Service Agreements and project roadmaps that define your R&D intent. This ensures your contracts meet the "contemplation" test required for 2026 compliance. We take a meticulous approach to categorising your workforce, ensuring that EPWs and subcontractors are correctly identified to maximise your return under the 65% rule. Our sector-specific knowledge in engineering and construction is particularly valuable here. We understand the technical hurdles inherent in these industries, allowing us to identify qualifying activities that might otherwise go unrecognised.

Protecting Your Business from HMRC Enquiries

The best way to handle an enquiry is to prevent it from happening. Our rigorous documentation process creates a comprehensive audit trail that explains the "why" behind every cost. We proactively address potential red flags, such as overseas expenditure or connected party transactions, before the claim is submitted. If HMRC does raise a query, we don't step back. We take the lead in defending your claim, using our solid track record and technical expertise to resolve issues efficiently. We transform a potentially intimidating regulatory procedure into a streamlined opportunity for growth. Book a no-cost introductory consultation with our specialists today.

Secure Your Innovation Funding for the Future

The Merged Scheme represents a new era for UK innovation, where documentation and intent are just as valuable as the technical work itself. Success in 2026 hinges on your ability to prove who contemplated the R&D at the outset and ensuring your contracts reflect this reality. By accurately categorising your workforce and navigating the strict overseas restrictions, you protect your business from the risk of HMRC enquiries whilst ensuring no qualifying expenditure is left on the table.

Claiming subcontractor costs for R&D tax credits doesn't have to be a source of administrative stress. At Recoup Capital, our team of chartered tax accountants and R&D specialists bring deep expertise in the construction and engineering sectors to every assessment. We operate on a success-based fee structure, meaning our goals are perfectly aligned with yours: securing the maximum capital recovery your innovation deserves.

Don't leave your claim to chance in this high-scrutiny environment. Maximise your R&D claim with Recoup Capital and turn your compliance journey into a strategic business advantage. We're here to act as your long-term partner in growth.

Frequently Asked Questions

Can I claim for a subcontractor based outside the UK in 2026?

You generally cannot claim for overseas subcontractors in 2026 unless you meet very narrow and specific criteria. HMRC requires R&D activities to be performed within the UK to qualify for relief. Exceptions only apply if the R&D is physically impossible to conduct here, such as specific clinical trials or testing in extreme geographic conditions. Lower costs or a lack of local skilled labour are not valid reasons for an exception.

What is the difference between a subcontractor and an externally provided worker (EPW)?

The difference lies in the level of supervision, direction, and control over the individual. A subcontractor works autonomously to deliver a specific technical outcome or a finished piece of work. An EPW is an individual provided by an agency who works as part of your internal team under your direct management. This distinction is vital for your CT600 filing and ensures you apply the correct compliance tests.

How much of my subcontractor costs can I actually recover?

You can typically recover 65% of qualifying subcontractor costs for R&D tax credits when dealing with unconnected parties. This 35% reduction is applied by HMRC to account for the subcontractor's profit margin. If the parties are connected, the calculation changes to the lower of the payment made or the actual relevant expenditure incurred by the subcontractor, effectively excluding any internal mark-up from the claim.

What happens if both the customer and the subcontractor try to claim for the same R&D?

HMRC uses the "intended R&D" test to prevent two companies from claiming for the same activity. The right to claim sits with the company that contemplated and initiated the R&D before the contract began. If a customer hires a firm to solve a technical uncertainty, the customer claims. Subcontractors should only claim if they are performing R&D for their own purposes, independent of the customer's intent.

Do I need a written contract to claim for subcontractor R&D costs?

Yes, a robust written contract is essential for a successful claim in 2026. HMRC expects to see clear evidence that the R&D was intended and contemplated at the start of the engagement. Your contracts should explicitly mention the resolution of scientific or technological uncertainties. Without this documentation, it's difficult to prove that you were the party driving the innovation rather than just purchasing a standard service.

Is there a limit on the amount of subcontracted work I can include in a claim?

There is no specific monetary limit on the amount of subcontracted work you can include, provided the costs are qualifying. You can claim for 65% of the total eligible expenditure regardless of the project's scale. However, the overall payable credit is subject to a PAYE/NIC cap. This cap is £20,000 plus three times your company's total PAYE and National Insurance contributions for the period.

What specific documentation does HMRC require for subcontractor costs?

HMRC requires a detailed trail including contracts, technical project reports, and the mandatory Additional Information Form. You must be able to demonstrate that the subcontractor was performing R&D that you intended. Invoices should be clearly linked to specific R&D work packages. To justify subcontractor costs for R&D tax credits involving connected parties, you'll also need to provide evidence of the subcontractor's underlying costs.

Can I claim for subcontractors if I am using the new Merged R&D Scheme?

You can absolutely claim for subcontractor costs under the Merged R&D Scheme. One of the primary benefits of the new unified system is that it harmonises the rules for companies of all sizes. Large companies can now claim for 65% of their subcontracted R&D costs, which is a significant improvement over the previous RDEC restrictions. This creates a more consistent framework for managing innovation expenditure across your entire supply chain.