Software Development R&D Tax Credit Examples: A 2026 UK Guide

What if the most valuable part of your latest sprint wasn't the code that worked, but the weeks your team spent failing to solve a complex integration problem? In 2026, HMRC isn't interested in your software's commercial utility; they want to see the technical "dead ends" you encountered. You've likely felt the frustration of sinking capital into solving "unsolvable" bugs, only to worry that your claim might trigger a compliance check. This guide provides the clarity you need by exploring specific software development R&D tax credit examples that distinguish between routine development and the genuine technological advances that qualify for the 20% merged scheme credit.

We'll help you transform that uncertainty into a strategic tool for reinvestment. You will discover a clear "yes/no" framework for eligibility, learn how to document the work of a "Competent Professional" correctly, and see how the 30% R&D intensity threshold impacts your claim under the Enhanced R&D Intensive Support (ERIS) scheme. We're moving beyond the traditional sales pitch to show you exactly how to secure the maximum capital recovered through a robust, HMRC-compliant technical report that stands up to scrutiny.

Key Takeaways

- Learn to distinguish between 'commercial innovation' and 'technological advance' to ensure your project meets HMRC’s 2026 criteria for scientific uncertainty.

- Use our detailed software development R&D tax credit examples to self-diagnose your projects and identify qualifying 'dead ends' that routine coding misses.

- Understand the shift to the Merged Scheme and how to correctly identify eligible expenditure, including cloud computing costs and technical salaries.

- Discover how to document your technical hurdles to satisfy the 'Competent Professional' standard and protect your business from increased HMRC scrutiny.

- Explore how a success-based partnership can help you recover maximum capital for reinvestment without the pressure of a traditional sales pitch.

Defining Software R&D in 2026: Beyond Routine Coding

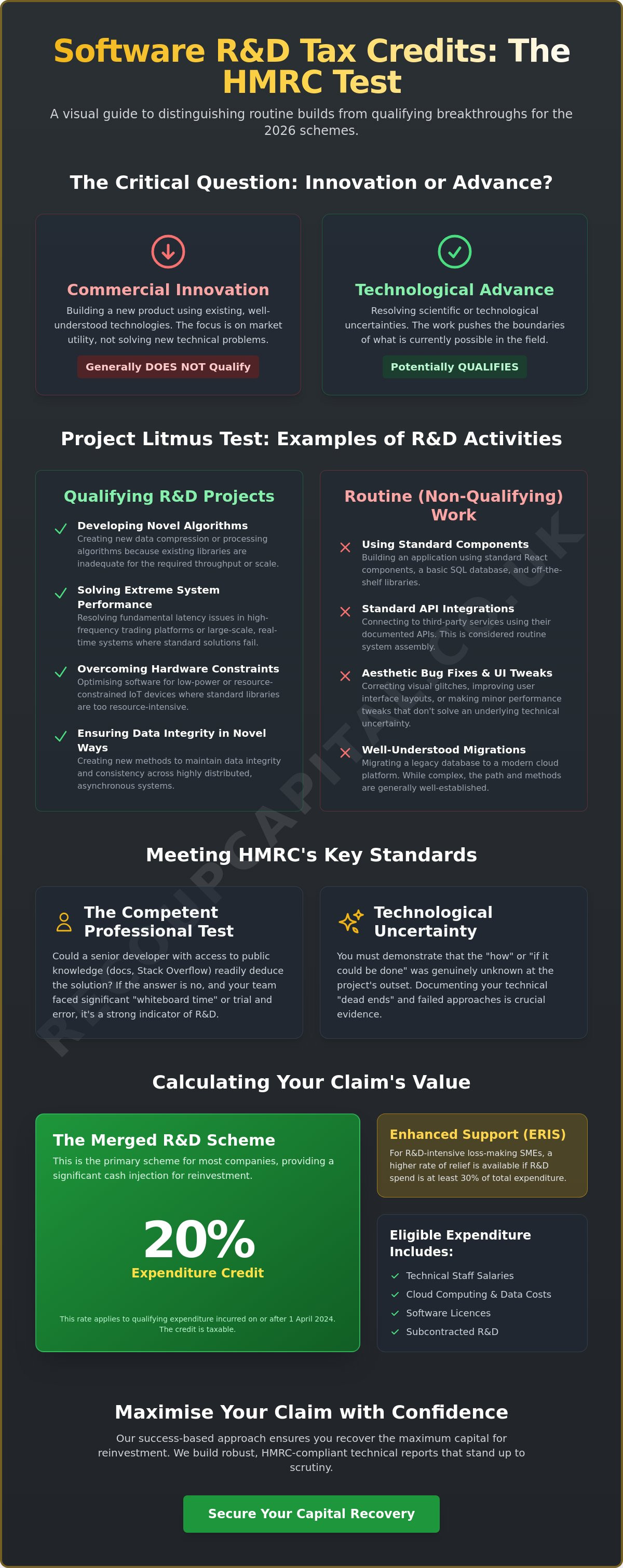

Software development is often a grind of trial and error. To HMRC, R&D specifically occurs when a project seeks to resolve a technological uncertainty through the lens of computer science. It isn't about the final product's utility or how well it sells; it's about the technical hurdles your team had to clear to make it function. Whilst many firms mistake commercial novelty for technical progress, the UK R&D tax credit scheme specifically rewards the latter. If you're building a "first-of-its-kind" application using standard React components and a basic SQL database, you've achieved commercial innovation. However, if you had to rewrite an underlying data compression algorithm because existing libraries couldn't handle the required throughput, you've likely made a technological advance.

Routine coding remains the most common reason for claim rejections. Standard API integrations, aesthetic bug fixes, or the assembly of existing software components do not qualify as R&D because the solution is "readily deducible" to any experienced developer. HMRC is increasingly vigilant, ensuring that only projects pushing the boundaries of what is technically possible receive support. This distinction is vital for businesses looking to recover money for reinvestment without triggering a compliance check.

The Competent Professional Test

In 2026, the "Competent Professional" is the ultimate gatekeeper for your claim. This person is typically a senior architect or lead developer with years of industry experience and up-to-date knowledge of standard practices. If your lead developer spent three weeks at a whiteboard because the solution wasn't in any documentation or Stack Overflow thread, that's a strong signal of R&D. The baseline of knowledge in 2026 is defined as the publicly available information, open-source libraries, and standard methodologies that a professional in the field is expected to possess and apply without significant experimentation.

Identifying Technological Uncertainty

Don't confuse complexity with uncertainty. A project can be massive and difficult without being R&D. For instance, migrating a massive legacy database to the cloud is complex, but the path is usually well-trodden. True uncertainty exists when the technical "how" or the "can it be done" is unknown at the start. We often see software development R&D tax credit examples involving extreme system latency in high-frequency trading or maintaining data integrity across highly distributed, asynchronous systems. For a deeper dive into these mechanics, you can find more information in our R&D tax credits explained guide. Hardware constraints, such as optimising software for low-power IoT devices where standard libraries are too heavy, also represent classic areas of technical struggle where software development R&D tax credit examples are frequently found.

Qualifying vs Non-Qualifying Software Projects: Key Distinctions

HMRC's lens has sharpened significantly over the last 24 months. Since the introduction of the merged scheme on 1 April 2024, the tax authority is looking for the exact moment commercial development crosses the threshold into technical research. This "boundary" is where your claim lives or dies. You must demonstrate that your work didn't just add a new feature for your users, but solved a technical problem that hadn't been resolved in the wider industry. Every claim now requires a mandatory Additional Information Form (AIF), which forces you to articulate these technical advances with precision. According to official HMRC guidance, the project must seek an "appreciable improvement" in the underlying technology. A minor tweak to a user interface or a standard security update won't pass muster; it needs to be a significant leap in performance, scalability, or technical capability.

When 'New to the Firm' Isn't Enough

It's a common trap to assume that because your team hasn't built a specific system before, the work must be R&D. If the solution is already discussed in public forums or available in open-source libraries, it's considered "readily deducible" to a competent professional. However, there's a vital exception. If a competitor has a similar feature but keeps the underlying architecture as a closely guarded trade secret, your effort to reinvent that technology from scratch might qualify. Standard "off-the-shelf" integrations, such as connecting a CRM to an email platform using a provided API, are almost always excluded from software development R&D tax credit examples because the technical path is already established.

Routine Maintenance vs Appreciable Improvement

Routine maintenance is the "business as usual" of the software world. This includes patching security vulnerabilities, updating a UI to match new brand guidelines, or porting an existing app to a newer version of an operating system. Contrast this with genuine R&D. If you're re-engineering a core processing engine to handle 10x the previous data throughput whilst maintaining sub-millisecond latency, you've moved into the realm of innovation. To determine if your project meets the "Appreciable Improvement" rule, consider this checklist:

- Does the work increase processing speed by a measurable, non-trivial percentage?

- Does it allow the system to scale to a significantly higher number of concurrent users than standard tools allow?

- Does it implement a new data structure that significantly reduces memory overhead?

If you're unsure where your project sits on this spectrum, we can help you assess your eligibility through a brief, technical-led conversation that cuts through the jargon.

Real-World Software Development R&D Tax Credit Examples

Seeing how other firms have successfully navigated the claim process is the most effective way to self-diagnose your own eligibility. HMRC focuses on the resolution of scientific or technological uncertainty. These software development R&D tax credit examples illustrate exactly where that uncertainty lives in modern codebases. You must maintain rigorous documentation throughout the development lifecycle to satisfy the HMRC guidelines for software R&D. Given the rise of automated coding tools, you should also review our guide on HMRC AI R&D claim transparency to ensure your technical reports aren't flagged by new compliance algorithms.

Example 1: Legacy System Re-architecture

A fintech firm attempted to migrate a monolithic COBOL system to a modern microservices architecture. The technical hurdle wasn't the migration itself, but the requirement for real-time synchronisation between the legacy database and the new services without any data loss. They had to develop bespoke middleware that managed "state" across distributed systems in a way that standard libraries couldn't achieve. This qualified as R&D because it resolved a specific technological uncertainty regarding data consistency in a hybrid environment. The project didn't just move data; it created a new method for ensuring integrity across incompatible architectures.

Example 2: Machine Learning & AI Integration

A health-tech company focused on developing a proprietary NLP model for medical diagnostic analysis. Whilst standard large language models are powerful, they often suffer from "hallucinations" that are unacceptable in a clinical setting. The R&D involved creating new algorithms to enforce factual accuracy within a constrained, highly specialised dataset of medical records. By pushing the boundaries of existing AI frameworks beyond what is readily available in open-source libraries, the project achieved a genuine technological advance. This work required significant experimentation to ensure the model could interpret complex medical terminology with 99.9% accuracy.

Example 3: Data Security & Cryptographic Innovation

A construction tech startup built a blockchain-based tracker for high-value materials. The primary obstacle was the high energy consumption of traditional proof-of-work mechanisms, which clashed with their sustainability goals. They developed a unique consensus mechanism that reduced energy usage by 85% whilst maintaining the same level of cryptographic security. This work advanced the field of distributed ledger technology and provided a clear instance of resolving a complex technical problem. It represents a significant jump in the efficiency of the underlying technology rather than a simple implementation of an existing blockchain platform.

Calculating the Value: Eligible Software R&D Expenditure

Identifying a technical advance is only half the battle. You must translate the software development R&D tax credit examples discussed earlier into a precise financial claim. Since 1 April 2024, the landscape has changed with the introduction of the Merged Scheme. This unified system provides a taxable expenditure credit of 20%. For profitable companies, this results in a net benefit of 15% after the 25% corporation tax rate is applied. If your business is a loss-making SME with an R&D intensity of at least 30%, you may qualify for the Enhanced R&D Intensive Support (ERIS), which offers a higher recovery rate of up to 27%.

Accuracy in your costings is the best defence against HMRC enquiries. You cannot simply guess the time spent on innovation; the tax authority expects a logical methodology for apportioning costs. This financial recovery represents significant money for reinvestment that can accelerate your roadmap. To understand how this capital can transform your business growth, explore why claim R&D tax credits before starting your calculation.

Staff Costs and Subcontractor Nuances

Staffing is typically the largest expenditure in software R&D. You should include gross salaries, employer National Insurance contributions, and pension payments. The challenge lies in "hybrid" roles. If a CTO spends 40% of their month in sales meetings and 60% resolving the complex middleware issues mentioned in our previous software development R&D tax credit examples, only the latter portion is eligible. For subcontractors, the general rule allows you to claim 65% of the invoice value. However, you must be aware of the 2024 restriction on overseas expenditure. Most payments to developers outside the UK are now ineligible unless the specific conditions for "unavoidable" overseas R&D are met.

Cloud Computing and Data Costs

Cloud computing costs from providers like AWS, Azure, or Google Cloud are now fully integrated into the R&D regime. You can claim for the instances and storage used specifically for R&D activities, such as running test environments or training new models. If you purchased datasets to refine a proprietary NLP algorithm, these costs are also qualifying expenditures. You must be disciplined in your exclusion of "routine" costs. Hosting fees for the final commercial version of your software do not qualify; the R&D boundary ends when the technological uncertainty is resolved and the product is ready for the wider market.

If you want to ensure your cost categories are fully optimised and HMRC-compliant, book a free 15 minute consultation to review your expenditure with our specialist team.

Maximising Your Software Claim with Recoup Capital

Securing the full value of your innovation requires a partner who understands both the nuances of tax legislation and the complexities of a codebase. We don't believe in the traditional sales pitch. Instead, we position ourselves as a protective guide through the intricacies of the UK tax system, acting as a bridge between your engineering team and HMRC. Our team of chartered tax accountants operates with a national reach, ensuring that every claim is backed by institutional credibility and a deep understanding of the 2026 regulatory landscape. We operate on a success-based fee structure; this means we only win when you do, ensuring our interests are perfectly aligned with your recovery goals.

The software development R&D tax credit examples we have explored throughout this guide demonstrate that HMRC is no longer satisfied with vague descriptions of "innovation." They require precise, technical evidence of scientific advancement. Recoup Capital provides the expertise needed to transform your technical struggles into money for reinvestment. We act as your "expert friend," handling the heavy lifting of documentation so your team can stay focused on building the next generation of software.

Our Technical Assessment Process

Our approach begins with a deep dive into your development cycles. We don't just look at your accounting software; we interview your lead developers and senior architects to extract the "technical gold" that HMRC expects to see. This forensic approach to cost identification ensures that no eligible expenditure, from cloud computing instances to specific developer hours, is missed. We look for the "dead ends" and technical hurdles that define genuine R&D. The result is the "Recoup Guarantee": a robust, evidence-based technical report designed to withstand the highest levels of scrutiny and secure the maximum capital for your business growth.

Navigating HMRC Compliance in 2026

Since the introduction of the mandatory Additional Information Form (AIF), the margin for error in software claims has vanished. We handle the entire AIF submission on your behalf, ensuring that the technical uncertainties and advances are articulated in a language that satisfies HMRC's specific 2026 criteria. Our role doesn't end with the submission. Should an enquiry arise, we act as your primary liaison with HMRC, defending the technical integrity of the claim until the funds are secured. We're here to make the process seamless, transparent, and highly efficient. If you are ready to explore your potential for recovery, claim your R&D tax credits with Recoup Capital today. We offer a FREE 15 minute consultation to help you determine your eligibility without any initial commitment. Today’s adviser, tomorrow’s partner; we're ready to help your business thrive.

Securing the Future of Your Innovation

The landscape of 2026 demands more than just a functional product; it requires a documented journey through technical uncertainty. You've seen how specific software development R&D tax credit examples, such as legacy re-architecture and cryptographic innovation, provide a clear roadmap for your own claim. By focusing on the resolution of scientific challenges rather than mere commercial features, you protect your business from HMRC scrutiny whilst unlocking significant money for reinvestment. Ensuring your technical "dead ends" are recognised as valuable assets is the first step toward a more resilient financial future.

Recoup Capital acts as your proactive guide, turning a complex government process into a seamless opportunity for growth. Our specialist chartered tax accountants have facilitated over £100m in capital for our clients, operating on a success-based fee model where we only win when you do. We don't just process paperwork; we act as your long-term partner in innovation. Book your FREE 15-minute R&D consultation today to discover how much capital your technical breakthroughs could recover. Your next sprint deserves the financial backing that only expert tax strategy can provide. Let's work together to help your business thrive.

Frequently Asked Questions

Can I claim R&D tax credits for SaaS development?

Yes, SaaS development qualifies when you resolve technical challenges like achieving sub-millisecond latency for 10,000 concurrent users or developing bespoke data synchronisation protocols. It isn't the delivery model that matters, but the underlying computer science. Routine web development is excluded, but projects that push the limits of scalable architecture are classic software development R&D tax credit examples that HMRC rewards.

Does building a mobile app qualify for R&D tax relief?

Building a mobile app qualifies if you overcome hardware constraints or develop new ways to handle data on-device. If your project involves optimising performance for low-power IoT sensors or creating a unique offline-first synchronisation engine, it meets the criteria. Simply porting a website to an app shell using standard frameworks is routine; true R&D requires resolving a technical "how" that isn't readily deducible.

What happens if my software project failed? Can I still claim?

You can absolutely claim for failed projects because HMRC rewards the attempt to resolve technological uncertainty. The fact that your team couldn't find a solution after months of experimentation is often the strongest proof of R&D. These "technical dead ends" demonstrate that the answer wasn't obvious to a competent professional, making the associated staff and cloud costs eligible for relief.

Is software R&D tax credit still available in 2026?

Yes, the scheme is very much active in 2026 under the Merged Scheme regulations that began on 1 April 2024. This unified system provides a 20% taxable credit for R&D expenditure. For loss-making, R&D-intensive SMEs, the Enhanced R&D Intensive Support (ERIS) continues to provide a more generous recovery rate of up to 27%, provided your R&D intensity stays above the 30% threshold.

Can I claim for the cost of my AWS/Azure servers?

You can claim for AWS, Azure, or Google Cloud costs that are directly attributable to your R&D activities. This includes computing power used for testing new algorithms or storage for datasets used in machine learning training. You must exclude any hosting costs for the final, commercially live version of the software, as these are considered routine operational expenses rather than research.

How much is the software R&D tax credit worth for a UK SME?

For most SMEs, the credit is worth a net benefit of 15% after corporation tax is deducted from the 20% gross credit. If your company is loss-making and meets the 30% intensity threshold for the ERIS scheme, the value increases significantly to 27%. These funds provide vital money for reinvestment, helping you accelerate your development roadmap and hire additional technical talent.

Do I need to be a 'tech company' to claim software R&D?

You don't need to be a "tech company" to claim; any business that develops bespoke software to solve technical problems is eligible. We often see software development R&D tax credit examples in the retail, construction, and manufacturing sectors. If your internal team is building proprietary tools to automate complex logistics or manage large-scale data integrity, you are likely conducting qualifying R&D.

What is the deadline for making a software R&D claim?

The deadline for submitting a claim is exactly two years after the end of the accounting period in which the expenditure was incurred. For example, if your financial year ended on 31 December 2024, you have until 31 December 2026 to file. Missing this window means you lose the opportunity to recover that capital, so it's vital to maintain accurate records and file promptly.