Qualifying R&D Expenditure for Tax Credits: The 2026 UK Guide

Identifying qualifying R&D expenditure for tax credits is no longer a simple box-ticking exercise; it's a precision operation that determines whether you secure a 20% taxable credit or trigger a stressful HMRC enquiry. With the transition to the Merged Scheme for accounting periods starting on or after 1 April 2024, the boundary between everyday operational costs and eligible innovation has shifted. You've likely felt the pressure of these legislative changes, perhaps worrying that the mandatory Additional Information Form (AIF) or the new 30% intensity threshold for loss-making SMEs will make your claim more difficult to justify.

It's understandable to feel cautious when HMRC is increasing compliance checks, but you shouldn't let technical confusion cost your business valuable capital. We'll show you exactly how to navigate the 2024, 2025, and 2026 rules to maximise your recovery whilst ensuring total compliance. This guide provides a clear list of eligible costs, from cloud computing to staffing, giving you the confidence to turn your technical uncertainties into strategic growth capital for reinvestment. We'll explore the specific mechanics of the Merged Scheme and the Enhanced R&D Intensive Support (ERIS) so you can claim every penny you're entitled to.

Key Takeaways

- Learn how to accurately identify qualifying R&D expenditure for tax credits under the Merged Scheme to ensure your claim reflects the full scope of your innovation.

- Understand the nuances of staffing costs and consumables, ensuring every hour spent resolving technical uncertainty is captured for maximum reinvestment.

- Discover how to include modern digital costs such as cloud computing and data licences, which are now central to 2026 R&D claims.

- Master the complex rules regarding subcontractors and externally provided workers to avoid common over-claiming errors that trigger HMRC enquiries.

- Protect your business by identifying hidden eligible costs whilst maintaining total compliance through a precision-led approach to your tax recovery.

Understanding Qualifying R&D Expenditure in the 2026 Landscape

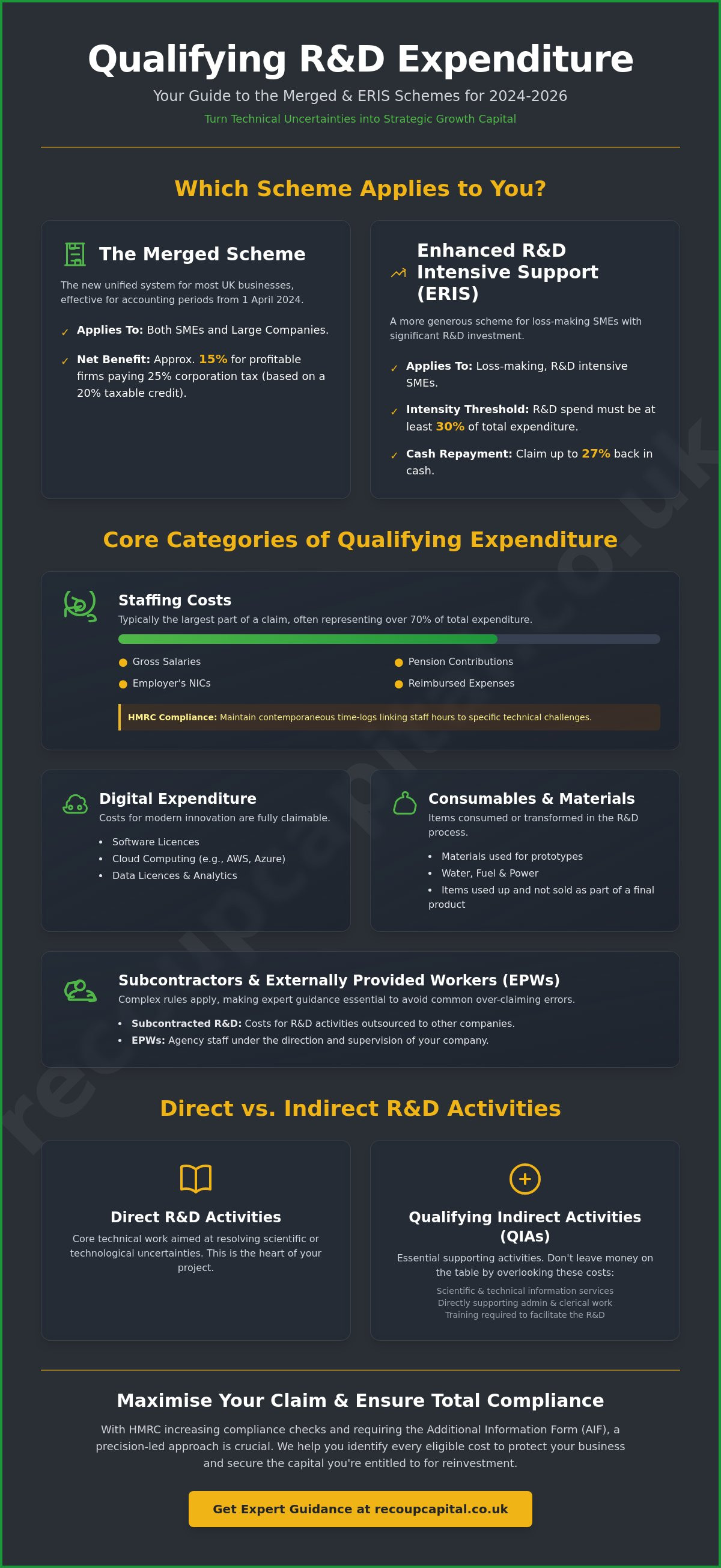

Qualifying R&D expenditure for tax credits represents the financial heartbeat of your innovation claim. It's the precise measurement of the investment your business makes to overcome technical challenges. In 2026, identifying these costs correctly is more than an accounting task; it's a strategic move that protects your business from the rising tide of HMRC compliance checks. Accurate identification serves as your primary defence against an enquiry, ensuring every pound claimed is backed by technical reality. We view these credits not as a one-off windfall, but as money for reinvestment. This capital allows you to fund your next cycle of innovation, helping your business thrive in a competitive market.

The Merged Scheme, which became mandatory for accounting periods beginning on or after 1 April 2024, has unified the rules for most businesses. For profitable companies paying the 25% corporation tax rate, the 20% taxable expenditure credit results in a net benefit of approximately 15%. However, if your business is loss-making and R&D intensive, you may fall under the Enhanced R&D Intensive Support (ERIS) scheme. To qualify for ERIS in 2026, your qualifying R&D expenditure for tax credits must meet the 30% intensity threshold. This is a reduction from the previous 40% requirement, opening the door for more SMEs to receive up to 27% back in cash. Your accounting period start date remains the most critical factor in determining which legislative framework applies to your claim.

The Merged Scheme and ERIS: Which Rules Apply?

Determining your eligibility depends heavily on your company's financial status and the date your accounting period began. The Merged Scheme now applies to both SMEs and large companies, simplifying the landscape into a single RDEC-style credit. If your company's R&D spend accounts for at least 30% of its total relevant expenditure, you'll likely benefit from the more generous ERIS rates. This distinction is vital for loss-making firms looking to secure the highest possible cash injection. We'll help you navigate these thresholds to ensure your claim is both maximised and compliant.

Direct vs. Indirect Qualifying Activities

To maximise your claim, you must distinguish between direct and indirect qualifying activities. Direct R&D involves the core technical work aimed at resolving scientific or technological uncertainties. If you're wondering what is R&D? in a broader sense, it's the systematic pursuit of knowledge to create new products or processes. Beyond the lab or the coding desk, you can also include Qualifying Indirect Activities (QIAs). These include:

- Scientific and technical information services used specifically for the project.

- Administrative and clerical activities that directly support the R&D.

- Training required to facilitate the R&D project.

You'll need to apportion time and costs carefully between these categories. Whilst direct activities are often easier to spot, missing out on QIAs means leaving money for reinvestment on the table. Precise apportionment is key to building a robust claim that stands up to HMRC scrutiny.

The Core Categories: Staffing, Consumables, and Materials

Staff costs usually make up the largest portion of any claim. For many UK businesses, this represents over 70% of their total qualifying R&D expenditure for tax credits. It's not just about who's in the lab; it's about identifying everyone contributing to the technical resolution. This includes developers, engineers, and project managers, but it also extends to those providing essential support. Identifying these individuals is the first step in transforming your payroll into money for reinvestment.

HMRC's focus on compliance has intensified throughout 2025 and 2026. They now expect a high level of detail regarding how staff time is recorded. Documentation is no longer optional. Maintaining contemporaneous time-logs that link specific hours to technical challenges is the most effective way to satisfy an inspector. If you're unsure how to structure these records, our expert team can provide clarity on the best practices for your industry.

Breakdown of Eligible Staff Costs

You can claim for gross salaries, Employer Class 1 National Insurance contributions, and pension contributions. However, the 2026 landscape requires precision with bonuses. Only bonuses that are "emoluments"—meaning they're part of the employee's reward for their R&D work—are typically eligible. Benefits-in-kind, such as company cars or private medical insurance, are strictly excluded from your calculations.

Pro-rating staff time is where many businesses stumble. If a software engineer spends 60% of their month on a new algorithm and 40% on routine bug fixes for an existing product, you must only claim for that 60% portion. This apportionment must be based on fact, not guesswork. Clear records ensure your claim remains robust under scrutiny whilst maximising the recovered capital you can put back into the business.

Materials and Utilities in the R&D Process

Consumable items are those "consumed or transformed" during the R&D process. This includes everything from chemical reagents to prototype components that are tested to destruction. A critical hurdle to watch for is the "First Sale" rule. If you create a prototype and later sell it to a customer, the material costs for that specific unit cannot be claimed. The logic is simple: the cost was recovered through the commercial sale, not the R&D investment.

Utility costs like water, fuel, and power are also eligible, provided they were used directly in the R&D activity. You'll need a logical basis for apportioning these. For instance, you might calculate the energy consumption of specific machinery or the square footage of a dedicated testing facility. According to the Official UK Government R&D Tax Relief Guidance, general administrative overheads like rent, business rates, and land taxes are ineligible. Focus your claim on the resources actually used up during the innovation phase to ensure total compliance.

Digital Expenditure: Software, Cloud Computing, and Data

The landscape of innovation has undergone a seismic shift toward digital infrastructure. Whilst traditional R&D might conjure images of laboratories and physical prototypes, modern breakthroughs often happen within virtual environments. For many tech-driven firms, software and cloud-related costs now represent the most significant portion of their qualifying R&D expenditure for tax credits. HMRC updated the rules to reflect this reality, ensuring that the UK R&D Tax Credit Scheme remains relevant for businesses operating at the cutting edge of software engineering and data science.

Identifying these digital costs requires a granular approach to your accounting. It isn't enough to simply point at a monthly subscription; you must demonstrate how that specific resource facilitated the resolution of technical uncertainty. When captured correctly, these expenses transform from overheads into strategic money for reinvestment. This capital allows you to scale your processing power or acquire more sophisticated tools for your next sprint. If you're unsure how these digital rules apply to your specific setup, it helps to see R&D Tax Credits Explained in the context of modern software development.

Qualifying Software Expenditure

You can claim for software licences used directly in your R&D projects. This includes specialised tools like CAD software, compilers, or testing environments. General-use software, such as your email client or accounting package, remains strictly ineligible. As SaaS (Software as a Service) subscriptions have become the industry standard, HMRC allows you to claim the R&D-attributable portion of these recurring costs. According to HMRC 2026 guidelines, software is defined as computer programs or code used directly to resolve scientific or technological uncertainty, excluding any software used for general administrative or commercial purposes.

Cloud Computing and Data Licences

Cloud computing costs are now a central pillar of many claims. If you're using AWS, Azure, or Google Cloud to provide the processing power or server space required for R&D testing, these costs are qualifying. The challenge lies in allocation. Most businesses use a single cloud infrastructure to support both R&D and live commercial operations. You must establish a robust methodology to apportion these costs, perhaps based on CPU usage or dedicated development environments, to ensure your claim stands up to scrutiny.

Data licence costs are also eligible, provided the datasets were purchased specifically for R&D purposes. This is particularly relevant for firms training AI models or conducting complex data analysis. There's a vital restriction to remember: you cannot claim for data licences if you have the right to sell the data or its derivatives to a third party. The data must be a consumable resource for your research, not a product for resale. Precision in these categories ensures you maximise your recovery whilst maintaining total compliance.

Subcontractors and Externally Provided Workers (EPWs)

Many companies rely on external expertise to drive their innovation forward. However, the rules for claiming these costs changed significantly for accounting periods beginning on or after 1 April 2024. Under the Merged Scheme, payments made to unconnected subcontractors are generally restricted to 65% of the relevant expenditure. This restriction reflects the fact that the subcontractor likely incurs their own overheads and profits, which HMRC does not want to subsidise twice. Understanding how to categorise these third parties is essential for a compliant claim and ensuring you receive the correct amount of money for reinvestment.

The most significant shift in the 2024/25 period was the introduction of overseas expenditure restrictions. Previously, UK companies could claim for R&D performed anywhere in the world. Now, for your costs to be considered qualifying R&D expenditure for tax credits, the R&D must generally be performed within the UK. This change aims to ensure that the tax relief directly benefits the UK economy and workforce. If you're managing a complex web of external partners, book a free 15-minute consultation to ensure your third-party costs are categorised correctly.

Navigating the Overseas Expenditure Rules

There are narrow exceptions where overseas costs still qualify. These are strictly limited to "unavoidable" circumstances where it would be impossible to conduct the work in the UK. For instance, if you're testing a new deep-sea sensor that requires specific oceanic conditions not found in UK waters, or if you need to access a unique clinical trial population, HMRC may permit the claim. Geographical, environmental, or legal requirements are the only valid grounds. Cost-efficiency or a lack of local talent are not considered valid excuses. You must document these reasons meticulously to avoid an immediate enquiry. For more on how HMRC is using technology to spot inconsistencies, see HMRC R&D Tax Claim Transparency and AI.

The Difference Between Subcontractors and EPWs

Distinguishing between an EPW and a subcontractor is vital because it changes how you calculate your claim. An EPW is typically an individual supplied by a staff provider who works under your direction and control, much like a direct employee. A subcontractor, by contrast, is usually an independent business tasked with delivering a specific outcome or piece of work. The contractual relationship determines the qualifying percentage:

- Connected Parties: If you use a subcontractor that is part of your corporate group, you can often claim 100% of the relevant costs, provided they are not making a profit on the transaction.

- Unconnected Parties: For third-party subcontractors, the 65% restriction applies to the lower of the payment made or the relevant cost incurred by the subcontractor.

- EPW Specifics: Like subcontractors, unconnected EPW costs are also restricted to 65%, but the individual must be subject to your supervision as to how the work is done.

Precision in these definitions prevents the type of over-claiming that triggers compliance checks. We help you audit these contracts to ensure your qualifying R&D expenditure for tax credits is calculated with total accuracy.

Maximising Claims Whilst Ensuring Total Compliance

Compliance isn't just about avoiding penalties; it's about building a sustainable innovation strategy. The rise of "R&D Cowboys"—firms that push the boundaries of eligibility without technical justification—has led to a significant increase in HMRC enquiries over the last two years. These aggressive tactics put your business at financial and reputational risk. Instead, we focus on a precision-led approach that identifies every legitimate pound of qualifying R&D expenditure for tax credits whilst ensuring your claim is ironclad. By linking every expense directly to a scientific or technological uncertainty, we transform your claim from a dry tax document into a powerful tool for reinvestment.

Preparing your technical narrative is the most critical part of this process. It's the story that explains why your expenditure qualifies, bridging the gap between your financial accounts and your engineering breakthroughs. HMRC expects to see how specific staff hours or material costs directly contributed to overcoming a technical challenge. When this narrative is robust, it acts as a shield, providing the transparency required to secure your funding without unnecessary delays. This strategic approach ensures you aren't just processing paperwork; you're securing capital to help your business thrive.

The Value of a Specialist Review

Generalist accountants do a fantastic job with standard corporation tax, but they often lack the deep technical expertise required for complex R&D claims. They might take a conservative stance to avoid risk, potentially missing 15% to 20% of eligible costs that a specialist would identify. Recoup Capital acts as your protective guide, digging deeper into your projects to find "hidden" costs in areas like software architecture or complex prototyping that others might overlook. Our Claiming R&D Tax Credits with Recoup Capital process begins with a low-friction, FREE 15-minute consultation to assess your potential without any sales pressure.

Preparing for an HMRC Enquiry

HMRC's current strategy involves a much higher volume of compliance checks, often triggered by simple red flags in expenditure reports. Claiming rounded figures or attributing 100% of a Managing Director's salary to R&D are common mistakes that invite scrutiny. You must maintain a robust audit trail, including project plans, meeting minutes, and the technical narratives we've discussed. Choosing the right partner is the most effective way to handle this new era of transparency. For more on selecting a compliant partner, read our guide on R&D Tax Credit Specialists UK. We stand by our results, ensuring that every claim we facilitate is backed by evidence and professional authority.

Turning Technical Uncertainty into Strategic Capital

Navigating the 2026 tax landscape requires more than just a list of costs; it demands a precision-led strategy. You've seen how the Merged Scheme and new digital expenditure rules for cloud computing and data licences have redefined what counts as qualifying R&D expenditure for tax credits. By meticulously documenting staff time and third-party contracts, you protect your business from the rising tide of HMRC compliance checks whilst securing vital money for reinvestment. This recovered capital is a strategic tool for your next cycle of innovation.

Our expert chartered tax accountants act as your protective guide, ensuring no eligible cost is missed. We operate on success-based fees with no upfront cost, embodying our commitment to being today's adviser and tomorrow's partner. Book your FREE 15-minute R&D expenditure consultation today to see how much capital your innovation could recover. Your technical breakthroughs deserve to be recognised. Let's work together to help your business thrive and lead the way in your industry.

Frequently Asked Questions

What are the main categories of qualifying R&D expenditure?

The primary categories include staffing costs, consumable items, software, cloud computing, data licences, and certain payments to subcontractors or externally provided workers. Staffing covers gross pay, Employer NI, and pension contributions for those directly involved in the project. Consumables include materials, water, fuel, and power that are transformed or used up during the research process.

Can I claim R&D tax credits for staff bonuses or dividends?

You can claim for bonuses if they are "emoluments" paid as a reward for R&D work, but dividends are strictly ineligible. Dividends are a distribution of profit rather than a direct cost of innovation. Because HMRC requires qualifying costs to be part of the payroll and subject to Class 1 National Insurance, dividend-based remuneration won't count toward your claim.

How has the Merged Scheme changed qualifying expenditure rules in 2026?

The Merged Scheme unified the R&D tax relief landscape for accounting periods starting on or after 1 April 2024, bringing SMEs and large companies under a single set of rules. It provides a 20% taxable credit, which offers a net benefit of approximately 15% for companies paying the 25% corporation tax rate. This change simplified the process by removing many of the previous distinctions between the old SME and RDEC schemes.

Can I include the cost of overseas subcontractors in my R&D claim?

Overseas subcontractor costs are generally excluded for accounting periods starting on or after 1 April 2024. You can only include these expenses if the work is considered "unavoidable" due to specific geographical, environmental, or legal requirements. HMRC no longer accepts cost-effectiveness or a lack of local UK talent as valid reasons for claiming overseas R&D expenditure.

Are rent and rates considered qualifying R&D expenditure?

No, rent and business rates are strictly excluded from qualifying R&D expenditure for tax credits. HMRC views these as general administrative overheads rather than direct costs of resolving technical uncertainty. To ensure your claim remains compliant, you should focus on capturing direct investment in people, materials, and digital infrastructure instead.

What percentage of subcontractor costs can I actually claim?

You can typically claim 65% of the payments made to unconnected subcontractors. If the subcontractor is a "connected" party, such as another company within your corporate group, you can often claim 100% of the relevant cost. However, this is provided the charge doesn't include a profit margin for the connected entity, ensuring the relief only covers the actual cost of the R&D performed.

How do I claim for cloud computing and data costs?

You claim for cloud computing and data by apportioning the costs based on their specific use in R&D activities. Since 1 April 2023, expenses for server space and processing power used for R&D testing or data analysis are eligible. You must maintain a clear methodology to exclude any portion of the licence or infrastructure used for commercial operations or data resale.

What happens if HMRC challenges my qualifying expenditure?

If HMRC challenges your qualifying R&D expenditure for tax credits, they'll open a formal compliance check to verify the technical and financial details of your claim. You'll need to provide your technical narrative and a robust audit trail that links every pound spent to a specific technical uncertainty. We act as a protective guide during this process, using our expertise to defend your claim with professional authority.