R&D Tax Credits for Loss-making Companies: A 2026 Guide to Cash Recovery

What if your company's balance sheet losses were actually your most potent tool for securing immediate, non-dilutive funding? It's a common misconception that HMRC only rewards the profitable; in reality, R&D tax credits for loss-making companies are designed to fuel the very businesses taking the greatest technical risks. You likely feel the pressure of cash flow constraints whilst scaling your innovation, wondering if your technical breakthroughs will ever pay for themselves before the next funding round.

We're here to help you transform those innovation costs into vital cash injections through the latest HMRC schemes. This guide explains how to navigate the 2024 merged scheme and the Enhanced Research and Innovation Support (ERIS) for R&D-intensive SMEs. You'll learn about the 30% intensity threshold, the 14.5% payable credit rate, and the specific compliance steps required to ensure your claim process is efficient and risk-free. By the end of this article, you'll have a clear roadmap to validate your innovation and secure the capital needed to fund your next phase of growth.

Key Takeaways

- Learn how to convert Corporation Tax relief into immediate cash injections, ensuring a lack of profit never prevents you from accessing vital HMRC incentives.

- Navigate the 2026 regulatory landscape by identifying whether your business qualifies for the Merged Scheme or the specific Enhanced R&D Intensive Support (ERIS).

- Discover the strategic advantages of surrendering losses to secure R&D tax credits for loss-making companies rather than carrying them forward for future use.

- Master the complexities of the PAYE cap and the 30% intensity threshold to protect your claim from scrutiny whilst maximising your capital recovery.

- Understand how partnering with specialists can transform your technical innovation into a strategic financial asset through a risk-free, success-based model.

Defining R&D Tax Relief for Loss-making UK Companies

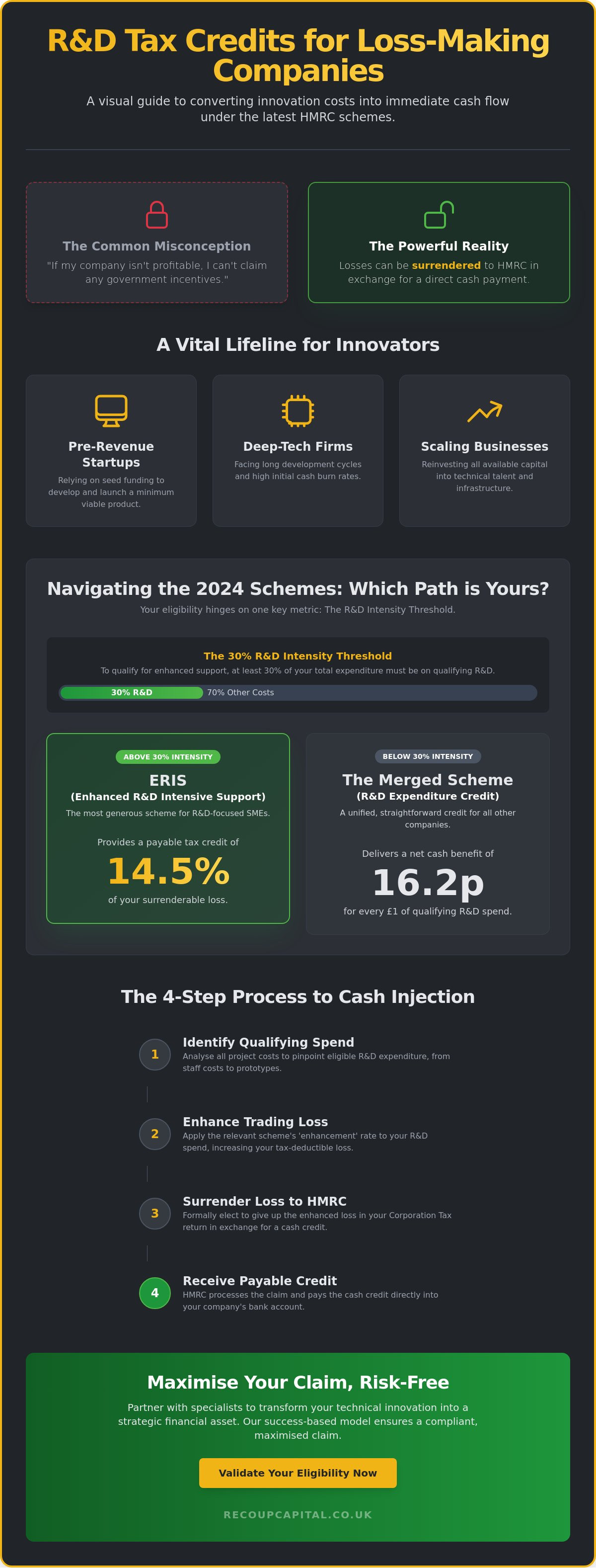

Many directors believe that if they aren't paying Corporation Tax, they're locked out of government incentives. This is a costly mistake. For innovative businesses, the UK R&D tax incentive is specifically designed to support those yet to reach profitability. It's a strategic funding tool that turns technical risks into liquid assets. Instead of waiting for future profits to offset costs, you can "surrender" your current trading losses to HMRC in exchange for a direct cash payment. Securing R&D tax credits for loss-making companies provides the runway needed to survive the "valley of death" during early-stage innovation.

This mechanism is particularly transformative for certain types of businesses:

- Pre-revenue startups relying on seed funding to reach a minimum viable product.

- Deep-tech firms with long development cycles and high initial burn rates.

- Scaling businesses reinvesting every penny into technical talent and infrastructure.

How the Cash Credit Mechanism Works

The process begins by identifying qualifying R&D expenditure and applying an "enhancement" to these costs. This creates a virtual deduction that increases your company's trading loss for tax purposes. Under the 2026 Merged Scheme, the credit is set at 20% of qualifying expenditure, though this credit itself is taxable. For those qualifying as R&D intensive under the Enhanced Research and Innovation Support (ERIS) scheme, you can claim a payable tax credit of 14.5% of the surrenderable loss. A surrenderable loss is the lower of the enhanced R&D top-up or the company’s total trading loss for the period. It's a precise calculation that transforms intangible innovation into tangible capital.

Qualifying as a Loss-making Entity

Your eligibility isn't determined solely by your bottom line on a spreadsheet. Accounting losses must be adjusted for tax purposes; items like depreciation are added back whilst capital allowances are deducted to reach a final tax position. It's also essential to consider group structures. If your company is part of a larger group, your loss-making status might be impacted by "connected parties" or shared resources across the organisation. Understanding these nuances is key to a successful claim. For a deeper dive into the fundamentals, you can find more about R&D tax credits explained on our dedicated resource page. This ensures your claim is built on a solid, compliant foundation that stands up to HMRC scrutiny.

Navigating the 2026 Landscape: The Merged Scheme and ERIS

The 2026 regulatory environment has simplified the landscape, but the choice between available pathways for R&D tax credits for loss-making companies remains a critical financial decision. Most businesses now fall under the Merged Scheme, which consolidated the previous SME and RDEC incentives into a unified "above-the-line" credit. However, for those whose primary business model is technical discovery, the Enhanced Research and Innovation Support (ERIS) provides a much-needed boost. Navigating the Merged R&D Scheme requires a precise calculation of your "intensity ratio" to avoid missing out on higher-tier funding.

The Merged R&D Expenditure Credit (RDEC)

The Merged Scheme offers a 20% gross credit on qualifying expenditure. Since this is an "above-the-line" incentive, the credit is treated as taxable income. For a loss-making entity, this means the gross 20% is reduced by the current Corporation Tax rate. If we assume a 19% tax rate, the net cash injection is 16.2p for every £1 spent. Whilst this is lower than previous SME rates, it provides a consistent, transparent return for larger loss-making firms or those who don't meet the intensity requirements. It's a straightforward path to capital recovery that rewards innovation without the complexity of meeting specific spend ratios.

ERIS: The Lifeline for R&D-Intensive SMEs

For loss-making SMEs where innovation is the core driver, ERIS is the gold standard. To qualify, your company must meet the "R&D intensive" criteria, meaning at least 30% of your total expenditure is dedicated to qualifying R&D. This 30% threshold is a hard limit; missing it by even a fraction of a percent defaults your claim to the standard Merged Scheme rates.

The benefit is substantial. ERIS allows for an additional 86% deduction on costs, with a payable tax credit of 14.5% of the surrenderable loss. In 2026, ERIS remains the most lucrative pathway for loss-making startups, provided their R&D intensity meets the 30% HMRC threshold. This results in a net benefit of approximately 27%, nearly double the standard rate. If you're currently scaling, our specialists can help you analyse your expenditure to ensure you're positioned for the maximum possible recovery. Understanding these nuances isn't just about tax; it's about protecting your company's future.

Strategic Choice: Surrendering Losses for Cash vs Carrying Forward

Deciding how to treat your technical deficit is a high-stakes corporate finance decision. For many, R&D tax credits for loss-making companies represent a choice between immediate liquidity and a future tax shield. Whilst the excitement of a cash injection is often the primary driver, it's vital to weigh the immediate value of cash-in-hand against the potential long-term benefits of carrying losses forward. This isn't just a tax filing step; it's a strategic move that dictates your company's financial flexibility for years to come.

The "time value of money" usually tips the scales toward surrendering the loss for cash. In an inflationary environment, £100,000 in your bank account today is significantly more valuable than a potential tax saving of the same amount three years from now. Cash provides the certainty needed to maintain momentum. However, if your business is on the cusp of significant profitability, carrying the loss forward could eventually offset profits taxed at the 25% main rate, potentially offering a higher total saving than the current credit rates. You must balance the urgent need for a "runway" against the long-term goal of minimising your effective tax rate.

When to Take the Cash Credit

For pre-revenue tech and biotech firms, cash is the lifeblood of innovation. Prioritising claiming R&D tax credits allows these businesses to extend their operational runway without giving up precious equity. This non-dilutive capital is often the difference between reaching a key milestone and needing an emergency funding round. When your burn rate is high and your focus is on technical survival, the immediate cash injection serves as a strategic asset to fund further R&D, hire specialist talent, or invest in critical infrastructure. It's a proactive way to fuel growth using the government's own incentive framework.

The Argument for Carrying Losses Forward

There are specific scenarios where holding onto your losses makes more sense. If your financial projections show a sharp pivot into high profitability within the next 12 to 24 months, those losses could be used to wipe out a 25% Corporation Tax bill. This is often more tax-efficient than surrendering them for a lower percentage credit today. Additionally, you must consider the role of "Loss Buying" rules during corporate acquisitions. If you're positioning the company for a sale, the value of carried-forward losses can sometimes be a point of negotiation, provided the trade remains the same. Navigating these complexities requires a partner who understands corporate finance as deeply as they understand tax law.

Calculating Eligibility and Overcoming the PAYE Cap

Securing R&D tax credits for loss-making companies often feels like a straightforward path to liquidity until the PAYE cap enters the equation. This regulation limits the amount of payable credit a company can receive to £20,000 plus 300% of its total PAYE and National Insurance liabilities for the period. HMRC introduced this measure to prevent fraudulent "shell companies" from claiming vast sums without actually employing technical staff or maintaining a physical presence in the UK. Whilst it protects the integrity of the scheme, it can inadvertently penalise genuine startups that rely heavily on external contractors or have founders taking minimal salaries to preserve cash.

There is a vital lifeline for businesses managing their own Intellectual Property (IP). You may be exempt from this cap if your company is actively creating, managing, or protecting its own IP and your expenditure on connected subcontractors and externally provided workers is less than 15% of your total R&D spend. Identifying these exemptions early is crucial for high-growth firms that don't yet have the UK headcount to support a large cash claim. HMRC's focus on HMRC R&D Tax Claim Transparency and AI signals a shift toward data-driven auditing, making it essential to document every technical uncertainty with precision.

Navigating the PAYE Cap Limitations

To calculate your "relevant liabilities" for the 3x multiplier, you must include the PAYE and NICs paid for all employees, not just those involved in R&D. If you're a startup with a low UK headcount but high qualifying spend, the £20,000 baseline offers some protection. However, using external contractors can be a double-edged sword; whilst they provide necessary expertise, they don't contribute to your PAYE threshold in the same way direct employees do. If you're unsure if your current structure meets the exemption criteria, speak with our technical team today to safeguard your claim.

Compliance and HMRC Enquiries

In 2026, the submission of the Additional Information Form (AIF) is a non-negotiable requirement for all R&D tax credits for loss-making companies. HMRC scrutinises these claims more heavily because the direct payment of cash represents a higher risk to the Treasury than a simple tax reduction. Forensic accounting is no longer optional; you must be able to justify why your project constitutes a technical advancement and how you've overcome specific uncertainties. A robust, evidence-based narrative is your best defence against a time-consuming enquiry, ensuring your capital recovery remains on track and risk-free.

Maximising Your Claim with Recoup Capital’s Success-Based Approach

Securing R&D tax credits for loss-making companies requires more than just technical knowledge; it demands a partner who understands the high stakes of your cash flow. We recognise that for a business in its growth phase, every penny of capital is a strategic asset. Our "No Win, No Fee" model is designed specifically to remove the financial barriers to entry for cash-strapped firms. This ensures your capital recovery journey is entirely risk-free, as our interests are perfectly aligned with the success of your claim. We don't just process forms. We act as a protective guide through the evolving regulatory landscape.

Our approach is led by chartered tax accountants who manage the entire technical narrative from start to finish. This is vital because HMRC now expects a level of forensic detail that generic platforms often fail to provide. We identify hidden costs that internal teams might overlook, such as specific software licences or employer pension contributions, ensuring no value is left on the table. By positioning these incentives alongside other opportunities like Capital Allowances, we help you build a holistic tax strategy that supports long-term stability rather than just a one-off payment.

Expertise Beyond the Paperwork

Success in R&D claims depends on the ability to translate technical risk into financial value. Our specialists possess deep industry experience across construction, engineering, and tech sectors. We don't just ask what you did; we ask why it was technically difficult. This proactive stance on compliance ensures that your claim meets the new transparency standards and the rigorous requirements of the Additional Information Form. Beyond the claim itself, we provide strategic advice on Corporate Finance to help you leverage your tax assets during business acquisitions or complex restructuring phases.

The Recoup Capital Difference

We view our clients as long-term partners rather than transactional entries in a ledger. This relationship-first approach means we stay invested in your future innovation, helping you refine your internal record-keeping to make future filings even more efficient. We reframe your tax returns as strategic tools for business growth, transforming a complex regulatory obligation into a streamlined funding engine. Our goal is to provide the professional authority you need to innovate with confidence, knowing your compliance is handled by experts. Book a no-cost introductory consultation with our R&D specialists today.

Turning Technical Risk into Strategic Capital

The 2026 tax landscape offers a powerful lifeline for innovative firms yet to reach profitability. By mastering the 30% intensity threshold for ERIS and navigating the nuances of the PAYE cap, your business can unlock vital liquidity that many directors overlook. Choosing R&D tax credits for loss-making companies over carrying losses forward provides the immediate non-dilutive capital required to extend your runway and fuel further discovery without sacrificing equity.

Our expert team of chartered tax accountants brings national coverage and specialist sector knowledge to every claim. We operate on a success-based, "No Win, No Fee" model, ensuring you receive professional, risk-free guidance that prioritises your bottom line. We're ready to act as your long-term partner, transforming complex regulatory requirements into a streamlined funding engine for your growth.

Don't let your innovation costs remain dormant on the balance sheet. Secure your non-dilutive funding with a specialist R&D claim assessment and take the next step toward a stronger financial future. Your technical breakthroughs deserve the capital to reach their full potential.

Frequently Asked Questions

Can my company claim R&D tax credits if it has never made a profit?

Yes, you can absolutely claim. HMRC designed these incentives to support technical innovation regardless of your current profitability. If your limited company is in a loss-making position, you can surrender those losses in exchange for a payable cash credit. This provides a vital cash injection to fund further research and development activities whilst you're still in your growth or pre-revenue phase.

What is the current R&D tax credit rate for loss-making SMEs in 2026?

In 2026, the rate depends on your company's R&D intensity. If you meet the 30% intensity threshold under the ERIS scheme, the payable tax credit is 14.5% of the surrenderable loss, resulting in a net benefit of approximately 27%. Companies that don't meet this threshold fall under the Merged Scheme, receiving a 20% gross credit that equates to roughly 16.2% net after tax.

How long does it take for HMRC to pay out a loss-making R&D claim?

HMRC typically aims to process R&D tax credits for loss-making companies within 28 to 40 days of submission. However, this timeline can vary depending on the complexity of your claim and current HMRC workloads. Since the introduction of the mandatory Additional Information Form, some claims may take longer if they're selected for a routine compliance check or a more detailed enquiry.

What is the PAYE cap and how does it affect my R&D tax credit claim?

The PAYE cap is a measure to prevent abuse of the scheme by shell companies. It limits the payable credit to £20,000 plus 300% of your company's total PAYE and National Insurance contributions. If your claim exceeds this amount, the cash payment is capped unless you meet specific exemption criteria related to the management of Intellectual Property and limited subcontractor spend.

Can I claim R&D tax credits for losses in previous accounting periods?

You can claim for any accounting period ending within the last two years. This statutory deadline is strict; if you miss it, the opportunity for capital recovery is lost. It's also important to remember that most first-time claimants must submit a Claim Notification Form within six months of the end of the accounting period to remain eligible for a retrospective claim.

Is it better to carry losses forward or surrender them for a cash credit?

This is a strategic decision. Surrendering losses for a cash credit provides immediate liquidity to extend your operational runway. Carrying losses forward might save you up to 25% in Corporation Tax once you become profitable, but this benefit is deferred and depends on future success. Most startups prioritise the "time value of money" and take the cash today to reinvest in innovation.

Does a loss-making company need to be R&D intensive to claim?

No, you don't need to be R&D intensive to access R&D tax credits for loss-making companies. Any company with qualifying expenditure can use the Merged Scheme. However, being "R&D intensive" (spending 30% or more of total expenditure on qualifying R&D) allows you to access the more generous ERIS rates, which provide a significantly higher cash return than the standard scheme.

How does the Merged Scheme affect loss-making companies compared to the old SME scheme?

The Merged Scheme replaced the old SME scheme for accounting periods beginning on or after 1 April 2024. It uses an RDEC-style "above-the-line" credit of 20% gross. For most loss-making SMEs, this is less generous than the old system unless they qualify for ERIS. The main benefit is a more unified, transparent system that applies consistently across companies of different sizes.