Manufacturing R&D Tax Relief Examples: Real-World Scenarios for 2026

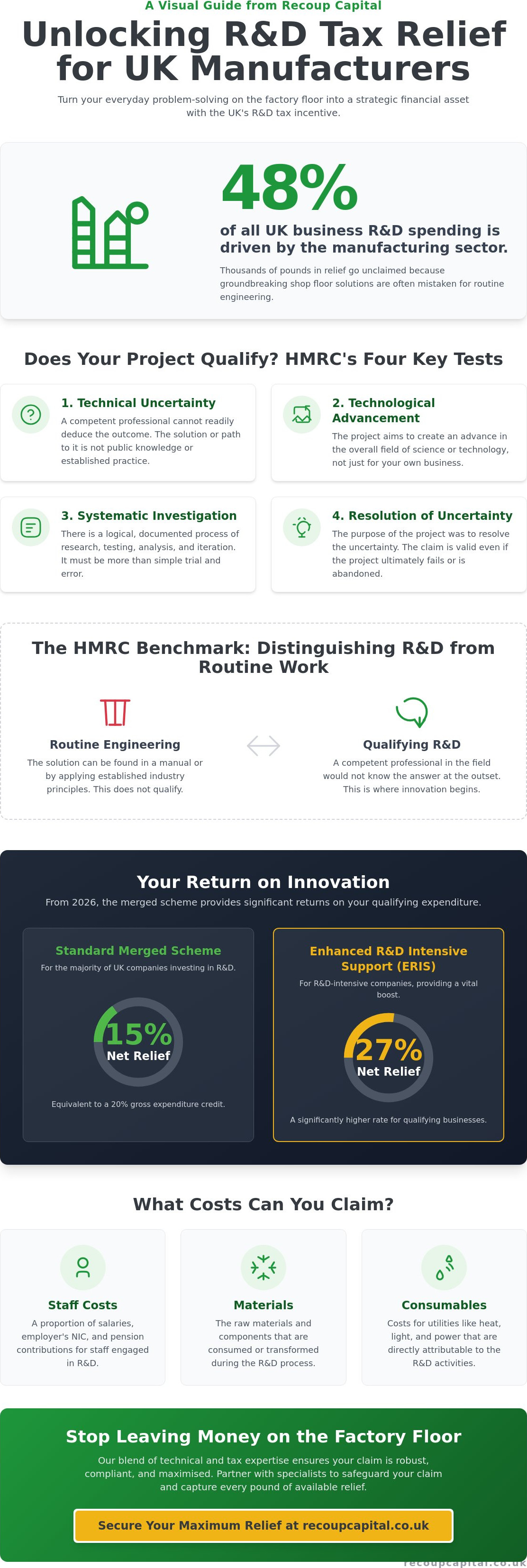

Did you know that the manufacturing sector drives nearly 48% of all UK business R&D spending? It's a staggering figure, yet many factory floor innovations go unclaimed because they're frequently mistaken for routine engineering. You likely recognise the frustration of solving a complex production bottleneck or refining a temperamental assembly process, only to wonder if HMRC would actually consider your solution "innovative" under the latest regulations. Distinguishing between standard practice and qualifying technical uncertainty is more critical than ever, especially with the increased scrutiny surrounding the mandatory Additional Information Form (AIF).

We've designed this guide to provide concrete manufacturing R&D tax relief examples that help you identify hidden claim opportunities and maximise your capital recovery. You'll discover how the merged scheme applies to your specific shop floor challenges in 2026, ensuring your technical successes are reflected in your bottom line. We'll preview real-world scenarios ranging from bespoke tooling to process automation, clarifying exactly which costs qualify for the standard 15% net relief or the 27% Enhanced R&D Intensive Support (ERIS) rate. It's time to stop viewing these technical hurdles as overheads and start treating them as strategic financial assets.

Key Takeaways

- Understand why manufacturing is the UK's powerhouse for innovation and how to reframe your technical problem-solving as a strategic business asset.

- Learn to distinguish between routine maintenance and genuine innovation by applying the "Competent Professional" test favoured by HMRC inspectors.

- Review five detailed manufacturing R&D tax relief examples that show you how to document the journey from technical uncertainty to a successful production outcome.

- Identify which specific staff, material, and consumable costs are claimable under the updated 2026 merged scheme regulations.

- Discover how a partnership with technical specialists can safeguard your claim against scrutiny whilst ensuring you capture every penny of available relief.

Beyond the Factory Floor: What is Manufacturing R&D Tax Relief?

R&D tax relief is a robust government incentive designed to reward companies that invest in technical problem-solving. It isn't a hand-out or a grant; it's a strategic mechanism that allows you to recoup a portion of the investment you've already made into innovation. Whilst many directors associate innovation with high-tech laboratories, the reality is that manufacturing is the UK's powerhouse for these claims. In fact, the sector accounts for nearly 48% of all UK business R&D spending, proving that the most valuable breakthroughs often happen amidst the noise of the production line.

The "Lab Coat Myth" frequently prevents eligible businesses from claiming what they're owed. You don't need a sterile environment or a team of scientists to qualify. If your engineers are currently battling to make a new material behave under extreme pressure, or if you're developing bespoke tooling to achieve tolerances that standard equipment cannot reach, you're likely performing R&D. By 2026, the landscape has shifted toward a single merged scheme for most businesses, providing a 20% gross credit that transforms these technical challenges into strategic financial assets. Reviewing specific manufacturing R&D tax relief examples helps clarify how these broad rules apply to your daily shop floor operations.

At its core, UK R&D Tax Credits aim to offset the financial risk inherent in trying something that might not work. Whether the project succeeds or fails is irrelevant to HMRC; the value lies in the attempt to overcome technical uncertainty.

The Four Key Criteria for Manufacturing

- Technical uncertainty: This exists when a competent professional in your field doesn't know, at the outset, if a particular result is achievable or how to achieve it.

- Scientific or technological advancement: Your project must aim to create an overall increase in the knowledge or capability of your industry, not just your own business.

- Systematic investigation: You must demonstrate a logical process of research, testing, and iteration. This isn't about "trial and error" in a vacuum; it's about documented experimentation.

- Resolution of uncertainty: The claim highlights how you attempted to solve the problem, even if the final outcome was a decision to abandon the project.

Why Manufacturing Leads the UK Innovation Index

UK manufacturers face unique pressures, from high energy costs to a constant demand for bespoke, low-volume production. These challenges force an incredible level of ingenuity. When you're forced to redesign a process to reduce waste by 15% or modify legacy machinery to handle sustainable new polymers, you're moving the "state of the art" forward. This constant drive for efficiency is why the sector remains the largest beneficiary of these incentives. For a deeper dive into the mechanics of the scheme, you can explore R&D tax credits explained to see how these principles apply beyond the manufacturing floor.

The HMRC Benchmark: Distinguishing R&D from Routine Engineering

HMRC doesn't just take your word for it. They apply a rigorous "Competent Professional" test to every claim. This person is typically an experienced engineer or technical lead who possesses the standard knowledge of the industry. If this individual could solve your production problem by simply looking it up in a manual or applying established engineering principles, the project fails the R&D test. It's vital to distinguish between commercial uncertainty and technical uncertainty. Whilst "will this product sell?" is a valid business concern, HMRC only cares about "can we physically make this work?".

The benchmark for an "advance" is also strictly defined. You aren't just comparing your project to your company's previous capabilities; you're comparing it to the state of the art for the entire sector. If a competitor has already solved the problem and the solution is public knowledge, your efforts to catch up don't qualify as R&D. Understanding these nuances is easier when you examine specific manufacturing R&D tax relief examples, which highlight the boundary between routine work and genuine innovation.

The "Non-Obvious" Rule

Technical uncertainty is the gap between existing knowledge and the desired outcome. If the path to a solution is clear from the start, it's routine engineering. Standard product customisation, such as adjusting the dimensions of a steel frame for a specific client or performing routine maintenance on a CNC machine, falls outside the scope of the scheme. These activities are predictable. Genuine R&D requires a "non-obvious" solution that only emerges through rigorous experimentation and technical struggle. For those looking for more clarity, the official HMRC guidelines on qualifying R&D provide the definitive legal framework for these distinctions.

Documenting the Technical Roadblocks

HMRC inspectors aren't just looking for your successes; they're looking for your "dead ends." These failed attempts are the strongest proof that technical uncertainty existed. If everything went perfectly according to plan, an inspector might argue the solution was obvious. Since the introduction of the mandatory Additional Information Form (AIF) in 2023, the requirement for detailed, contemporaneous evidence has only intensified. You must show the systematic investigation as it happened.

Keeping precise notes whilst the project is active ensures you don't lose track of claimable costs. If you're unsure how your current documentation stacks up, it's worth considering why claim specialists are so focused on the technical narrative. This level of detail protects your business during HMRC enquiries and ensures your financial returns are treated as strategic assets rather than mere paperwork.

5 Real-World Manufacturing R&D Tax Relief Examples

Theoretical definitions only go so far. To truly understand if your shop floor activities qualify, you need to see how these rules apply to actual production challenges. Many directors mistakenly believe that only successful projects count toward a claim. In reality, some of the strongest manufacturing R&D tax relief examples involve projects that were ultimately abandoned. HMRC values the technical journey and the attempt to resolve uncertainty, regardless of whether the final product hit the market. These scenarios illustrate the "Problem-Investigation-Outcome" framework that underpins a robust technical narrative.

Example 1: Bespoke Automation and Robotics Integration

Problem: A mid-sized automotive supplier attempted to integrate a high-speed robotic arm into a legacy assembly line built in the 1990s. The existing PLC (Programmable Logic Controller) used a proprietary, outdated language that couldn't communicate with the modern robot's API, causing dangerous synchronisation lags.

Investigation: Engineers spent six months developing bespoke middleware to translate signals in real-time. This required extensive testing of signal latency and the creation of custom algorithms to prevent collision risks during power fluctuations.

Outcome: The systems were successfully synchronised, reducing cycle times by 12%. The time spent by engineers and the materials used during the testing phase all formed part of a successful claim.

Example 2: Sustainable Material Development

Problem: A packaging manufacturer sought to replace traditional oil-based plastics with a new bio-composite material derived from agricultural waste. However, the new material lost structural integrity at 45°C, making it unsuitable for standard shipping conditions.

Investigation: The technical team experimented with various chemical binders and fibre densities. They conducted dozens of thermal stress tests to find a composition that maintained rigidity without sacrificing biodegradability. Providing a practical perspective on manufacturing R&D claims often highlights this type of material science as a high-value activity.

Outcome: Whilst they achieved a higher thermal threshold of 60°C, the material became too brittle for high-speed folding. Even though the project was paused, the investigation into chemical binders qualified as R&D.

Example 3: Process Optimisation for Waste Reduction

Problem: A metal casting firm faced a 15% scrap rate due to microscopic fractures that only appeared after the cooling process. Standard cooling protocols couldn't prevent these inconsistencies.

Investigation: The firm invested in a custom thermal monitoring system and developed an adjustable mould cooling process. They ran multiple iterations to simulate different cooling gradients and their impact on the metal's molecular structure.

Outcome: The scrap rate dropped to 4%. This advancement in process capability moved the firm's technical baseline forward, qualifying the staff costs and energy used during the trials for relief.

Maximising Your Claim: Qualifying Costs and 2026 Compliance

By 2026, the transition to the merged R&D scheme is complete. Most manufacturing firms now operate under a single framework that provides a 20% gross credit on qualifying expenditure. For profitable companies, this usually results in a net benefit of approximately 15%. However, loss-making SMEs that are "R&D intensive" (spending at least 30% of their total costs on qualifying R&D) can access the Enhanced R&D Intensive Support (ERIS) scheme. This provides a more generous cash repayment of up to 27%. Identifying these opportunities within manufacturing R&D tax relief examples is the first step toward transforming your technical hurdles into strategic capital.

Direct Costs: Staff, Materials, and Utilities

Staff costs typically form the largest portion of a manufacturing claim. This includes gross salaries, employer National Insurance contributions, and pension contributions. You must accurately apportion the time your engineers, CAD designers, and shop floor managers spend on specific R&D projects. If a production manager spends 40% of their week resolving a technical bottleneck, 40% of their qualifying costs can be included. Consumable items are also vital; these are materials "used up" or transformed during the prototyping and testing phase. If you've scrapped three tonnes of aluminium whilst perfecting a new extrusion technique, that material cost is claimable. Additionally, software licences used specifically for R&D, such as high-end simulation or modelling tools, are eligible for relief.

Navigating the New HMRC Compliance Standards

HMRC's focus on compliance has intensified. Since August 2023, every claim must be accompanied by a mandatory Additional Information Form (AIF). This digital submission requires a detailed technical narrative that explains the uncertainty you faced and the systematic investigation you performed. In 2026, vague descriptions are no longer tolerated. You must link your costs directly to the technical challenges described in your narrative. This level of detail ensures your claim is robust enough to withstand the stricter compliance checks currently being implemented by HMRC.

Writing these narratives requires a blend of technical engineering knowledge and tax expertise. If the prospect of digital submissions and rigorous documentation feels like a barrier to your innovation, it's time to seek specialist guidance. You can begin claiming R&D tax credits with the support of a partner who understands how to translate your shop floor successes into a compliant, high-value claim.

Partnering for Success: How Recoup Capital Secures Your Relief

Identifying qualifying activity is only half the battle. Securing the relief requires a meticulous approach that satisfies HMRC's 2026 standards whilst protecting your business from unnecessary risk. At Recoup Capital, we operate on a success-based fee model. This means we only win when you win, aligning our goals directly with your business growth and capital recovery. We don't rely on traditional sales pitches; instead, we demonstrate our value through a track record of quantitative success and technical precision.

Our process is led by a dual-disciplinary team. We pair chartered tax accountants with technical specialists who speak the language of the factory floor. This combination ensures that every technical nuance is captured and translated into a robust financial claim. We act as your protective guide through the complexities of the regulatory landscape, handling everything from the initial discovery to direct HMRC liaison. By examining the manufacturing R&D tax relief examples relevant to your specific sub-sector, we can accurately benchmark your potential return and ensure no stone is left unturned.

Our Methodology: The Technical Audit

Many general accountants focus on the obvious R&D, but our technical audit is designed to uncover the "invisible" innovation happening in your production cycles. We look beyond the ledger to the technical roadblocks your team solves daily. These are the moments where "standard engineering" fails and innovation begins. By building an enquiry-proof technical report, we ensure your claim is defended by evidence rather than estimates. Whether you're a precision engineering firm in Cornwall or a large-scale manufacturer in Caithness, our national reach ensures you have access to specialised expertise regardless of your location. We take the time to understand your specific manufacturing R&D tax relief examples to build a narrative that resonates with HMRC inspectors.

Beyond the Claim: Long-Term Strategic Growth

We view tax relief not just as a refund, but as a strategic business tool for future innovation. Reinvesting this capital allows you to tackle the next generation of automation or sustainable material challenges. Our partnership-oriented approach also extends to other areas of capital recovery, such as capital allowances on your manufacturing facilities and machinery. This holistic focus on your bottom line ensures you aren't leaving money on the table that could be used to scale your operations. Our relationship-first philosophy means we remain by your side as your business evolves, helping you turn technical successes into long-term financial assets.

Your innovation deserves more than just a processed form. It requires a dedicated partner invested in your future. Book a no-obligation consultation with our specialists today to discover the true value of your technical breakthroughs.

Transform Your Technical Challenges into Strategic Assets

The manufacturing landscape in 2026 demands constant adaptation, and the technical hurdles you overcome on the shop floor are more than just operational costs. By distinguishing routine engineering from genuine innovation and maintaining rigorous documentation for the mandatory Additional Information Form, you protect your business whilst unlocking significant capital. These manufacturing R&D tax relief examples demonstrate that whether you're integrating legacy systems with modern robotics or perfecting sustainable materials, your technical struggle has tangible financial value.

At Recoup Capital, our team of Chartered Tax Accountants and manufacturing specialists works alongside you to ensure every qualifying activity is captured accurately. We operate on a success-based fee model, reflecting our commitment to delivering results rather than delivering a traditional pitch. This partnership-led approach transforms complex regulatory procedures into a streamlined opportunity for long-term growth. It's time to treat your technical breakthroughs as the strategic assets they truly are.

Speak to an R&D Specialist about your manufacturing projects today and take the first step toward securing the relief your business deserves.

Frequently Asked Questions

Can I claim R&D tax relief if my manufacturing project failed?

Yes, you can claim for failed projects. HMRC's primary interest is the attempt to resolve technical uncertainty, not the final commercial success. If your engineers spent months trying to integrate a new alloy that eventually proved too brittle for production, those costs remain eligible. Failed projects often provide the strongest evidence of genuine research and development because they demonstrate that the solution wasn't obvious to a competent professional.

What counts as a "consumable" in a manufacturing R&D claim?

Consumables include any materials transformed or "used up" during the R&D process. In a manufacturing context, this typically covers raw materials used for prototypes, scrap metal from trial runs, and the energy consumed during testing phases. If you produce a batch of components to test a new cooling gradient and those parts cannot be sold because they are destructive samples, the material costs qualify for relief.

How far back can I claim R&D tax credits for my manufacturing business?

You can file a claim up to two years after the end of the accounting period in which the expenditure was incurred. This rolling window allows you to look back at previous technical challenges that you might have overlooked at the time. For example, if your year-end was December 2024, you have until December 2026 to submit your claim for that period.

Do I need to be a "high-tech" company to qualify for R&D relief?

No, you don't need to be a "high-tech" firm to qualify. R&D tax relief is available to any company that seeks a technological advancement by overcoming uncertainty. Whether you're a traditional foundry improving casting methods or a food manufacturer developing new preservation techniques, the focus is on technical problem-solving. Many manufacturing R&D tax relief examples involve traditional industries modernising their legacy processes through bespoke engineering.

How long does it take for HMRC to process a manufacturing R&D claim in 2026?

HMRC generally aims to process claims within 40 days, though this can vary depending on the complexity of the submission and current enquiry levels. Since the introduction of the mandatory Additional Information Form (AIF), the initial digital check is faster, but the bar for technical detail is higher. Ensuring your technical narrative is robust from the outset is the most effective way to prevent delays or follow-up enquiries.

What is the difference between SME and RDEC schemes for manufacturers?

Most businesses now operate under the single merged scheme, which provides a 20% gross credit. The previous distinction between the SME and RDEC schemes has been largely consolidated to simplify the process. However, loss-making SMEs that are "R&D intensive" can still access the Enhanced R&D Intensive Support (ERIS) scheme, provided at least 30% of their total operating costs are spent on qualifying R&D activities.

Can I claim for the time my shop-floor staff spent on a prototype?

Yes, you can claim for the time shop-floor staff spend directly contributing to an R&D project. If your machine operators are involved in testing a new production line setup or monitoring trial runs for a prototype, their proportional gross salary, NI, and pension contributions are eligible. It's essential to keep accurate records of the time spent on these specific tasks to satisfy HMRC's apportionment requirements.

Do I need to submit a technical report with my CT600?

You must submit a mandatory Additional Information Form (AIF) online before or at the same time as your CT600 tax return. Whilst a separate technical report isn't strictly mandatory in the traditional sense, the AIF requires the same level of detailed technical narrative. This form is the primary tool HMRC uses to assess the validity of your claim, making technical precision and clear documentation more important than ever.