Overcoming Scientific or Technological Uncertainty: A Guide for UK R&D Tax Credits

What if the technical failures you have been trying to hide are actually the most valuable assets in your business? Many UK companies miss out on substantial capital recovery because they view "uncertainty" as a sign of weakness rather than the primary engine of innovation. In the eyes of HMRC, overcoming scientific or technological uncertainty isn't just a hurdle; it's the very definition of qualifying R&D. If you have ever struggled to distinguish between routine problem-solving and genuine technical advancement, you're certainly not alone. The fear of an HMRC enquiry often stems from a lack of clarity in how these challenges are defined and documented.

You deserve to feel confident that your technical narratives reflect the true scale of your innovation whilst meeting the rigorous 2026 compliance standards. This guide will help you master the core eligibility criteria for R&D tax relief, showing you exactly how to transform your toughest technical obstacles into successful claims. We'll explore a clear framework for identifying qualifying projects and provide the tools you need to maximise your tax relief through accurate, evidence-based reporting. By the end of this article, you'll see your technical failures as a strategic business tool for future growth.

Key Insights

- Understand why overcoming scientific or technological uncertainty is the fundamental pillar of your claim and how to identify it using the competent professional test.

- Learn how to distinguish between routine technical fixes and qualifying innovation by applying a practical project audit framework to your current operations.

- Secure your claim against HMRC scrutiny by mastering the 2026 documentation requirements for detailed and compliant technical narratives.

- See how common challenges in construction, engineering, and land remediation often qualify as R&D when viewed through a specialist lens.

- Discover how to maximise your claim through a success-based collaboration with chartered tax accountants who reframe tax relief as a strategic asset.

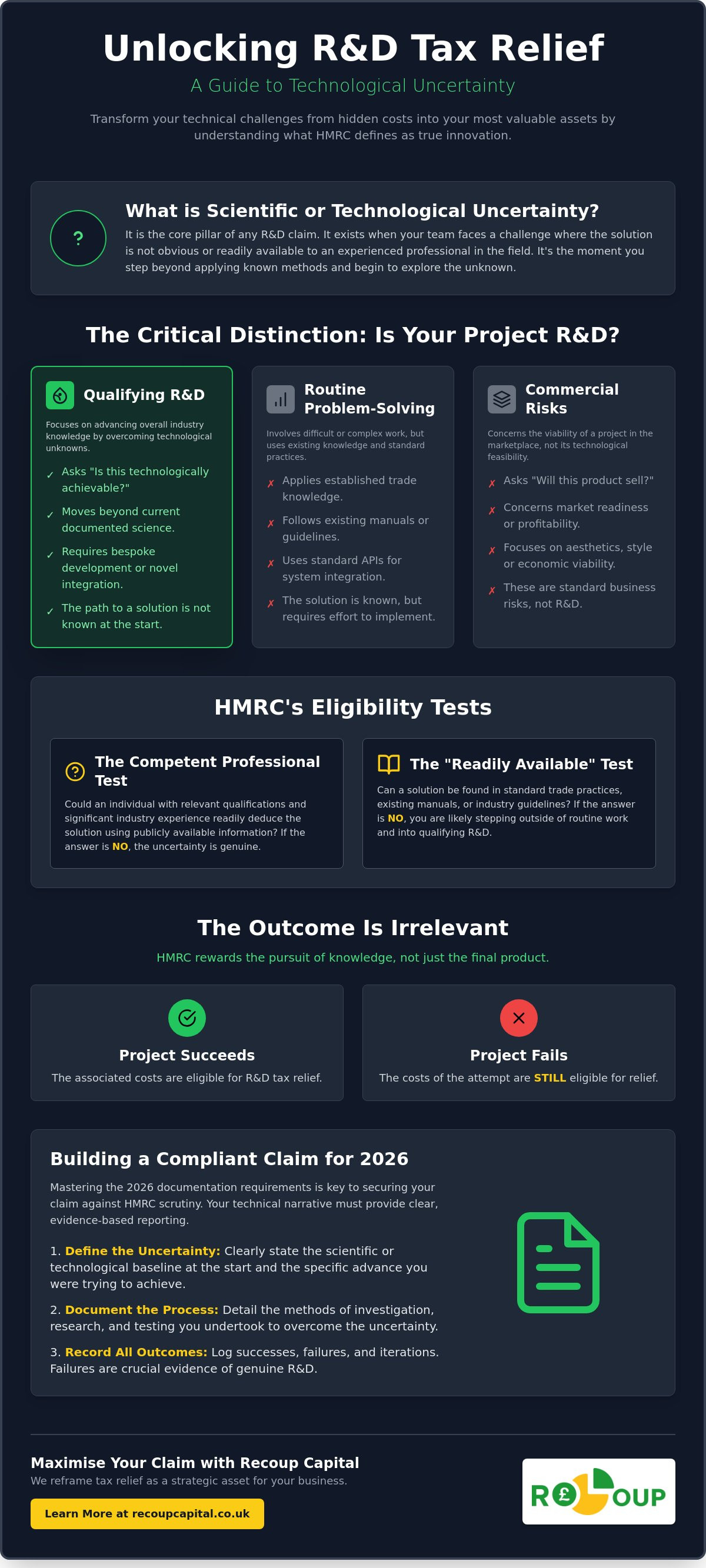

What is Scientific or Technological Uncertainty in R&D?

Scientific or technological uncertainty is the heartbeat of every successful claim. It is the core pillar that supports the entire structure of the UK's tax relief system. Without it, you simply have a standard business project. HMRC specifically looks for evidence that your team faced a challenge where the solution was not obvious. If your lead engineers or scientists were unsure if a goal was even achievable, you have likely found the starting point for a robust claim.

It is vital to distinguish between business uncertainty and technical uncertainty. Business uncertainty asks whether a product will sell, if the market is ready, or if the project will be profitable. These are commercial risks that every company takes. Technical uncertainty, however, asks whether the laws of science or the current limits of technology allow the project to work at all. The process of overcoming scientific or technological uncertainty is what separates a standard upgrade from a qualifying breakthrough. It involves moving beyond what is already known and documented in your industry.

HMRC uses the "competent professional" as their benchmark for these claims. This is an individual with relevant qualifications and significant experience in the specific field. If this expert cannot readily point to a solution or find a path forward using publicly available information, the uncertainty is genuine. We often find that businesses underestimate their own innovation because their internal experts are so used to solving "impossible" problems that they view it as just another day at the office.

The HMRC Definition for 2026

Under the merged scheme rules that apply to 2026 filings, the requirement for an "advance" in the field remains mandatory. You cannot achieve a genuine advance without first identifying a specific uncertainty. It is the friction caused by this unknown factor that creates the opportunity for relief. Crucially, your project doesn't need to be a commercial success to qualify. Even if the technical hurdles proved too high and the project ended in failure, the costs associated with the attempt are still eligible. HMRC rewards the pursuit of knowledge and the attempt to innovate, not just the final product. This principle is fundamental to R&D Tax Credits globally, ensuring that companies aren't penalised for taking technical risks.

Why Routine Work Does Not Qualify

HMRC inspectors frequently apply the "readily available" test to filter out routine work. If a solution could be reached by a competent professional through standard trade practice or by following existing manuals, it won't qualify. Routine work is the "how-to" of your industry; it's the application of established knowledge to a familiar problem. Whilst these tasks are essential for business, they don't represent a shift in the baseline of technology. Qualifying R&D happens when you step off the map. If you're unsure where your work sits on this spectrum, you can find R&D tax credits explained in our detailed guide to help you categorise your activities correctly.

Identifying Uncertainty vs. Routine Technical Problems

Distinguishing between a difficult day at work and a qualifying R&D project is often the biggest hurdle for UK businesses. Many companies assume that if a project is "hard," it must be R&D. However, HMRC draws a sharp line between routine technical problems and genuine uncertainty. Routine work involves challenges that a skilled professional can resolve by applying established trade knowledge or standard industry practices. To identify qualifying activity, you must look for the moments where the path forward was entirely obscured.

Consider the difference between system integration and bespoke development. If your team is connecting two software packages using a standard API, they are performing routine integration. This is an exercise in existing knowledge. If, however, they must build a bespoke interface because the underlying data structures are fundamentally incompatible, they are likely overcoming scientific or technological uncertainty. The uncertainty here isn't just about how long the task will take; it's about whether the integration is even technologically feasible under the specific constraints of your project.

Even "standard" industry challenges can contain qualifying R&D if the specific environment prevents standard solutions from working. For example, a construction firm dealing with unusual soil instability might find that every "routine" method fails. At that point, the project shifts from standard engineering to experimental development. If you are unsure where your project sits on this line, you might want to explore the process of claiming R&D tax credits to see how these distinctions are applied in practice.

The Competent Professional Test

HMRC relies on the "competent professional" to validate a claim. This individual should possess relevant qualifications and a proven track record in the field. Their struggle to find a solution is your primary evidence. If this expert cannot find a solution in the public domain or through standard testing, you have reached the "state of the art" limit. As detailed in the HMRC internal manual, the inability of such a professional to readily resolve the problem is a core indicator of qualifying R&D.

Systematic Investigation vs. Happy Accidents

HMRC doesn't just want to see that you solved a problem; they want to see how you solved it. A "happy accident" or a lucky guess won't suffice for a claim. You must demonstrate a planned approach that involves testing, evaluating, and refining. Systematic investigation is a methodical process of testing and refining technical solutions. This approach requires you to document failed hypotheses and abandoned prototypes. These "failures" are actually valuable evidence, as they prove that the solution was not readily available and required a rigorous scientific process to uncover.

Documenting Uncertainty for HMRC Compliance in 2026

HMRC has significantly tightened its requirements for technical narratives as we move into 2026. The introduction of the mandatory Additional Information Form (AIF) means your submission must be more than a simple summary of project goals. It must be a forensic account of your technical journey. To succeed, your documentation needs to speak HMRC’s language, focusing on the granular details of why a solution was not readily available. Vague descriptions of "hard work" or "innovation" are no longer sufficient to secure relief under the merged R&D scheme.

Transparency is now the primary metric for compliance. HMRC is increasingly using sophisticated tools to identify AI-generated claims that lack authentic technical depth. These "templated" narratives often fail to capture the specific nuances of a project, triggering immediate red flags. You must provide a human-authored account that demonstrates a genuine process of overcoming scientific or technological uncertainty. Collecting evidence in real-time is the most effective way to build this narrative. Consider this checklist for your development phase:

- Project logs and time-sheets specifically linked to technical roadblocks.

- Email trails discussing failed hypotheses or unexpected technical results.

- Photographs or digital captures of prototypes, testing environments, or failed site samples.

- Minutes from technical strategy meetings where a change in direction was required due to technological failure.

The Technical Narrative Structure

A compliant narrative follows a logical three-step progression. First, you must define the baseline technology. This involves explaining the "state of the art" in your industry and why existing solutions were inadequate. Second, you must identify the specific technological gap or uncertainty. This is the "why" of your claim. Finally, you must detail the work done to resolve that gap. This section should focus on the systematic investigation process, including the testing and refining mentioned in previous sections, rather than the commercial outcome.

Avoiding HMRC Enquiries

Common red flags that trigger audits include using overly promotional language or focusing on business benefits rather than technical challenges. HMRC inspectors are trained to look for "routine" descriptors that suggest the work was standard practice. Presenting technical failures as proof of uncertainty is a powerful strategy; it shows that the solution was not obvious even to a competent professional. For more insight into how modern compliance is evolving, you can read about HMRC R&D Tax Claim Transparency and AI to ensure your documentation stays ahead of the curve.

Sector Examples: Uncertainty in Action

Theory only takes you so far. To truly understand if your work qualifies for relief, you must look at how these principles apply to the grit and reality of your specific industry. In heavy sectors like construction and engineering, the process of overcoming scientific or technological uncertainty often begins when standard site protocols fail. What might look like a "difficult" project to a manager is often a qualifying R&D opportunity to a specialist who knows how to spot the technical unknown.

Construction and Civil Engineering

In the construction sector, uncertainty frequently arises from the environment itself. A project might require developing new methods for building on unstable or contaminated land where traditional piling techniques are ineffective. If your engineers have to design a bespoke foundation system because the soil behaviour is unpredictable, they are facing a technological gap. Similarly, integrating complex renewable energy systems into legacy building structures often presents significant hurdles. You aren't just installing off-the-shelf tech; you're solving the problem of how two fundamentally different eras of engineering can work together without compromising structural integrity. These challenges are perfect entry points for claiming R&D tax credits, as they move beyond routine project management into the territory of experimental development.

Developers should also consider the financial impact of Land Remediation Relief. When you are forced to innovate to remove asbestos or treat arsenic-heavy soil, the technical narrative often overlaps with R&D. If the remediation requires a new chemical process or a bespoke mechanical filtration system, you may be eligible for both reliefs, significantly boosting your capital recovery.

Manufacturing and Food Technology

Manufacturing and food technology firms face their own unique set of uncertainties, particularly regarding chemistry and scale. Overcoming shelf-life uncertainties whilst removing artificial preservatives is a classic example. You might know how to make the product in a test kitchen, but maintaining that stability at a commercial level is a different challenge. Scaling production often reveals technological uncertainties that were invisible at the prototype stage. Moving from a five-litre lab beaker to a five-thousand-litre industrial vat can change the thermodynamics and chemical reactions of a product entirely. If your team is spending weeks adjusting temperatures, pressures, and flow rates to prevent product degradation, they are operating in a space where overcoming scientific or technological uncertainty is a daily reality.

If these scenarios sound familiar, you may be sitting on unclaimed tax relief that could be reinvested into your next project. You can speak with our specialists to audit your project portfolio and ensure no qualifying innovation goes unrecognised.

Maximising Your Claim with Recoup Capital

Securing a successful R&D tax credit claim in 2026 requires more than just a list of expenses. It demands a partnership with specialists who can translate your technical breakthroughs into the precise language HMRC expects. At Recoup Capital, we act as a protective guide through the complexities of the UK’s regulatory landscape. Our approach is built on a foundation of transparency and reliability, ensuring that your business receives the maximum relief whilst remaining fully compliant with the latest standards. We don't just process paperwork; we invest in your long-term innovation strategy.

Our success-based fee model is a core part of this commitment. By aligning our rewards with your results, we ensure that our team is as motivated as yours to uncover every qualifying activity. This relationship-first philosophy means there is no aggressive sales pressure. Instead, we demonstrate our value through the quality of our technical narratives and the quantitative success of our claims. We employ chartered tax accountants who work alongside technical experts to bridge the gap between the workshop floor and the tax office. This dual expertise is essential for accurately overcoming scientific or technological uncertainty in a way that satisfies rigorous HMRC scrutiny.

Our Technical Assessment Process

Many general accountants often miss the nuances of technological uncertainty because they focus primarily on the financial ledger. Our specialists take a different approach. We conduct in-depth technical interviews to identify "hidden" R&D that your team might consider routine. We look for the friction points in your projects, the failed prototypes, and the abandoned hypotheses that actually form the strongest evidence for a claim. From this initial discovery to the final HMRC submission, we provide end-to-end support. We handle the forensic detail of the technical narrative, ensuring every word serves to demonstrate how you were overcoming scientific or technological uncertainty throughout the development process.

The Strategic Advantage of Capital Recovery

We believe in reframing tax credits as strategic assets rather than simple refunds. The capital recovered through a successful claim isn't just a one-off payment; it's a tool for future growth. Reinvesting these returns allows you to accelerate your innovation cycles, hire specialised talent, or invest in new equipment that pushes your technical boundaries even further. This cycle of innovation and recovery creates a powerful momentum for your business. If you are ready to see how your technical challenges can be transformed into a strategic advantage, you should contact Recoup Capital for a no-cost technical assessment. Let us help you navigate the path to successful capital recovery with confidence and clarity.

Transforming Technical Hurdles into Strategic Growth

Your technical challenges aren't just obstacles to be cleared; they're the essential evidence needed to fuel your next phase of growth. By correctly identifying and documenting the process of overcoming scientific or technological uncertainty, you shift your R&D narrative from a cost centre to a strategic business asset. Whether you're navigating the complexities of a contaminated site or scaling a new manufacturing process, the friction you encounter is exactly what HMRC wants to reward. It's about recognising that your most difficult projects often hold the greatest financial potential.

Recoup Capital acts as your proactive guide through this regulatory landscape. Our team of chartered tax accountants and R&D specialists brings deep expertise in complex sectors like construction and engineering to every claim. We operate on a success-based fee structure; we only win when you do. This partnership-oriented approach ensures your technical narratives meet the highest 2026 compliance standards whilst maximising your capital recovery. Book your free technical R&D assessment with Recoup Capital and let's turn your technical hurdles into the capital your business needs to thrive. Your innovation deserves to be recognised and rewarded.

Frequently Asked Questions

Can I claim R&D tax credits if my project failed to overcome the uncertainty?

Yes, you can claim for unsuccessful projects because HMRC rewards the attempt to innovate rather than the final result. The process of overcoming scientific or technological uncertainty carries an inherent risk of failure. Costs incurred whilst attempting to find a solution are qualifying expenditures, provided you can demonstrate a systematic investigation took place. In many cases, a technical failure serves as the most compelling evidence that a solution was not obvious.

How do I prove that a solution was not "readily available" to a competent professional?

You prove this by demonstrating that a skilled professional in your field could not resolve the problem using standard trade knowledge. if your lead engineer consulted industry manuals, searched technical journals, or attempted standard testing without finding a path forward, the solution was not "readily available". Documentation of these initial searches and the subsequent lack of public information is essential for a compliant 2026 submission.

What is the difference between a scientific advance and a technological advance?

A scientific advance involves expanding fundamental knowledge in a field such as biology or physics to understand how the world works. A technological advance focuses on the practical application of science to create improved products, services, or processes. Whilst the two often overlap, the majority of UK claims involve technological advancement, where a company develops a bespoke solution to a specific engineering or manufacturing challenge.

Is "overcoming uncertainty" required for every R&D project claim?

Yes, identifying and overcoming scientific or technological uncertainty is a mandatory requirement for every R&D tax credit claim in the UK. Without a specific technical uncertainty, HMRC views the work as routine business activity or standard project management. It is the presence of a challenge that cannot be solved through existing knowledge that makes the project eligible for tax relief under current guidelines.

How has the definition of technological uncertainty changed for 2026?

The core definition remains consistent, but the 2026 compliance standards demand much higher transparency and granular detail. Under the merged scheme, companies must use the Additional Information Form (AIF) to provide forensic technical narratives. HMRC now places a greater emphasis on the specific "why" behind the uncertainty, moving away from broad descriptions toward a clear account of the technical roadblocks encountered.

Can software development count as overcoming technological uncertainty?

Software projects qualify when they resolve a technical unknown in computer science, such as developing a new data encryption method or a complex algorithm. Routine web development or standard app building using existing frameworks usually doesn't count. The project must push the boundaries of what is technologically possible rather than just applying existing tools to a new business problem.

What documentation does HMRC expect to see regarding technical uncertainties?

HMRC expects to see contemporary evidence created during the development phase of the project. This includes project logs, design blueprints, test results, and minutes from technical strategy meetings. They want to see a clear trail of the systematic investigation used to tackle the uncertainties. Retrospective summaries are often viewed with scepticism; real-time documentation is your best defence against an enquiry.

Does a project qualify if we used existing technology in a completely new way?

Using existing technology qualifies if the new application creates unforeseen technical challenges that standard trade knowledge cannot solve. If adapting a tool for a new environment requires you to resolve problems that a competent professional hasn't faced before, it becomes R&D. The uncertainty lies in whether the technology can perform in that specific new context, requiring a systematic process of testing and refinement.