Is My Project an Advance in Science or Technology? The R&D Tax Credit Guide

What if the technical roadblock that nearly derailed your last project was actually your company's most valuable financial asset? Many directors hesitate to claim R&D tax credits because they assume their work isn't "groundbreaking" enough, yet the real question isn't about prestige. The core of a successful claim is asking: is my project an advance in science or technology according to HMRC's specific, technical definitions? You don't need to be splitting atoms to qualify; you simply need to be resolving uncertainties that a competent professional in your field couldn't easily fix.

It's natural to feel some trepidation regarding complex terminology or fear an enquiry if your project seems standard. We understand that this confusion often leads to missed opportunities for capital recovery whilst your competitors move ahead. This guide provides the precise criteria used to define a technological advance, helping you determine if your project qualifies for significant relief under the 2024 merged scheme rules. We will explore the framework for explaining your innovation clearly, ensuring you have the confidence to pursue a claim and transform your technical hurdles into strategic business growth.

Key Takeaways

- Learn the distinction between a simple internal improvement and a genuine industry-wide breakthrough to ensure your work meets HMRC's strict eligibility criteria.

- Identify the specific technical uncertainties within your workflow by asking "is my project an advance in science or technology" that a competent professional could not readily solve.

- Discover how to apply the "Competent Professional Test" to benchmark your innovation against existing knowledge and validate the technical merit of your claim.

- Understand the systematic methodologies needed to document your R&D activities and build a robust technical report that withstands HMRC scrutiny.

- See how partnering with specialists can transform your technical challenges into strategic financial assets through a transparent, success-based fee model.

Defining an Advance in Science or Technology for UK Tax Relief

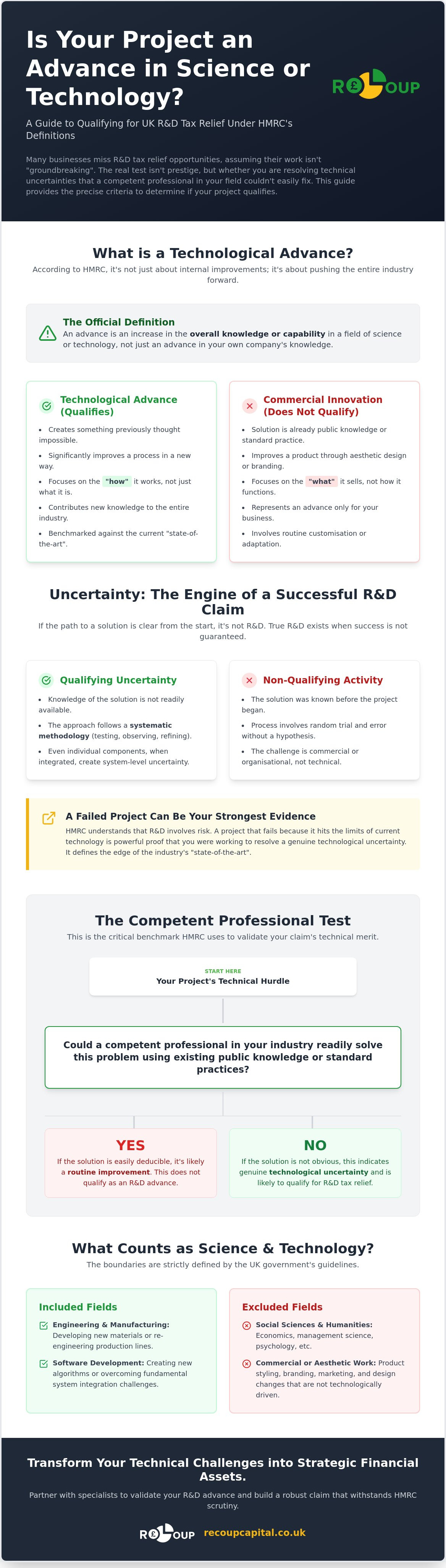

Identifying a qualifying project begins with the Department for Science, Innovation and Technology (DSIT) guidelines. These rules state that an advance is an increase in the overall knowledge or capability in a field of science or technology. As part of the wider UK tax incentive for R&D, this definition serves as the foundation for every claim. To accurately answer the question, "is my project an advance in science or technology?", you must look beyond your own workshop or office. If the solution to your problem is already public knowledge or is available through standard practice, it doesn't represent an advance in the field, even if it's entirely new to your business.

HMRC draws a sharp line between commercial advances and technological ones. Developing a product that sells better because of its aesthetic design or clever branding is a commercial success, but it won't qualify for R&D tax credits. A technological advance occurs when you create something that was previously thought impossible or significantly improve a process in a way that wasn't previously understood by professionals in your industry. It's about the "how" rather than the "what".

The Distinction Between Innovation and Advance

Marketing teams often use the word "innovation" to describe any new feature or minor tweak. Whilst these changes are important for business growth, they rarely meet the threshold for tax relief. HMRC is looking for an increase in "overall knowledge". This means your project must contribute something to the industry that wasn't there before. You need to benchmark your work against the current "state-of-the-art" technology. If a competent professional in your sector could look at your problem and easily deduce the answer using existing tools, you are likely dealing with company-specific innovation rather than a qualifying advance.

What Science and Technology Includes (and Excludes)

The Role of Scientific or Technological Uncertainty in Your Claim

Scientific or technological uncertainty is the engine of a successful R&D tax credit claim. If you knew exactly how to solve your technical problem before you began, you weren't conducting research and development. According to official government guidelines, uncertainty exists when knowledge of whether something is scientifically possible or technologically feasible is not readily available. This is the pivot point when asking "is my project an advance in science or technology". If the path to a solution is not clear to a professional working in the field, you have found the uncertainty required to justify a claim.

HMRC distinguishes between a systematic process and simple trial and error. Randomly testing different materials or code snippets without a clear hypothesis rarely qualifies. To meet the threshold, your work must follow a structured methodology of testing, observing, and refining. Whilst many directors fear that a failed project signifies a poor investment, HMRC views it differently. A failed project is often the strongest proof of uncertainty. If you spent months attempting to overcome a technical barrier and ultimately found it was impossible with current technology, you've successfully identified the limits of the industry's "state-of-the-art".

System Uncertainty: When Components Clash

The "Readily Deducible" Threshold

HMRC asks a simple but challenging question: was the solution obvious to a competent professional? If the answer could be found by "googling it" or reading a standard technical manual, the project fails the test. This is why documenting your "dead ends" is so important for your claim. Every time you tried a standard industry solution and it failed to work, you were proving that the answer was not readily deducible. If you are struggling to separate standard problem-solving from qualifying R&D, you might find it helpful to see how these definitions apply to your specific industry sector.

By focusing on the hurdles that forced your team to think beyond standard practice, you build a narrative of genuine technical challenge. This documentation transforms a simple project log into a robust evidence base for your tax relief claim, ensuring you receive the credit your innovation deserves.

Industry-Wide Advance vs. Internal Innovation: The Competent Professional Test

HMRC doesn't expect you to be an expert in tax law, but they do expect you to employ an expert in your technical field. This individual, known as the "Competent Professional", is the benchmark for your claim. To answer "is my project an advance in science or technology", you must view the work through their eyes. A competent professional typically possesses relevant qualifications, such as a degree in engineering or computer science, paired with several years of industry experience. Their opinion is the cornerstone of your technical report because they can distinguish between a simple business hurdle and a genuine technological gap. This focus on expert-led assessment aligns with broader international standards, as seen in the OECD analysis of the R&D scheme, which highlights how the UK incentivises genuine innovation over routine business activities.

The distinction between an industry-wide advance and internal innovation is vital. If your project was only an advance because your team lacked the training that others in the industry already have, it won't qualify. The challenge must be one that would baffle any professional with the right skills and experience. It's about pushing the "state-of-the-art" rather than just catching up with your competitors. A competent professional must lead the R&D assessment to ensure the technical narrative correctly identifies where standard practice ended and innovation began.

Standard Practice vs. Qualifying R&D

Distinguishing between routine work and R&D is often the most difficult part of a claim. Standard practice involves using existing knowledge and tools to achieve a predictable outcome. If your team is simply "doing their job" by applying known solutions to known problems, it won't count as an advance. Routine adaptation of existing tools, even if the result is a better product, does not meet the threshold if the path to that result was clear. The following table illustrates the difference:

| Standard Practice (Non-Qualifying) | R&D Advance (Qualifying) |

|---|---|

| Routine software bug fixing or security patching. | Developing a new algorithm to solve a previously unresolvable latency issue. |

| Adapting a standard manufacturing process for a new client. | Re-engineering a process to work with a material never successfully used in that context. |

| Integrating two standard APIs using existing documentation. | Creating bespoke middleware to manage data conflicts between incompatible legacy systems. |

Evidence of a Professional’s Uncertainty

To prove an advance, you must demonstrate that your lead professional was genuinely stuck. This isn't about personal capability; it's about the lack of available industry knowledge. You can evidence this through internal technical logs, minutes from brainstorming sessions, or records of failed attempts to find solutions in peer-reviewed journals and industry forums. If the answer wasn't in the "manual", you were likely moving into R&D territory. For a deeper dive into these nuances, you can read more about R&D tax credits explained. This documentation proves that the uncertainty was real and that your project was seeking a genuine increase in overall technological capability.

Methodologies for Evidencing Your Advance to HMRC

Proving your technical merit requires more than just a list of costs; it demands a structured narrative that aligns with HMRC's rigorous standards. Since August 2023, every claim must be accompanied by an Additional Information Form (AIF). This digital submission is mandatory and requires granular detail about each qualifying project. To successfully answer "is my project an advance in science or technology", you must translate your internal development logs into a technical report that highlights the resolution of uncertainty. Retrospective guessing at the end of the financial year is a common pitfall that often leads to rejected claims. Maintaining real-time documentation ensures that the nuances of your technical challenges are captured whilst they are still fresh.

The Four-Step Documentation Framework

A robust claim follows a logical progression that mirrors the scientific method. By adopting this framework, you provide the clarity HMRC needs to validate your innovation:

- Step 1: Baseline the current state. Clearly describe the existing technology or knowledge in your field before your project began. This establishes the "state-of-the-art" you intended to surpass.

- Step 2: Define the specific hurdle. Identify the exact technological uncertainty that standard practice could not resolve. Be precise about why current solutions were inadequate.

- Step 3: Detail the systematic testing. Record the experiments, analysis, and iterations your team performed. This proves that your progress was the result of a deliberate R&D process.

- Step 4: Articulate the resulting advance. Explain what new knowledge or capability was gained. Even if the project failed, the knowledge of why it failed is a qualifying advance.

Avoiding Vague Language in Technical Narratives

Specific terminology is the language of successful claims. HMRC inspectors are trained to spot vague buzzwords that mask a lack of technical depth. Words like "bespoke," "complex," or "innovative" are frequently flagged because they describe a commercial outcome rather than a technological process. To strengthen your narrative, replace these qualifiers with technical metrics and data. Instead of saying a system was "complex," describe the specific latency constraints or data throughput issues your engineers faced. Using hard data makes it much easier for an inspector to agree that your project is an advance in science or technology.

Building a claim that stands up to scrutiny requires a blend of technical insight and tax expertise. If you are unsure how to structure your evidence, you can learn more about claiming R&D tax credits with a specialist partner. Our team helps you bridge the gap between your technical work and HMRC's expectations, ensuring every qualifying activity is documented correctly from the outset.

Partnering with Recoup Capital to Validate Your R&D Advance

Deciding to move forward with a claim is a significant step for any business. At Recoup Capital, we don't view ourselves as a mere paperwork processor. We operate as a long-term partner, acting as a protective guide through the complexities of HMRC's evolving regulations. Our success-based fee model ensures that our goals are perfectly aligned with yours; we only win when you do. This transparent approach removes the financial risk of exploring your eligibility, allowing you to focus on what you do best: innovating.

Our team is composed of chartered tax accountants and technical specialists who speak your language. We understand that providing a definitive answer to "is my project an advance in science or technology" requires more than just a surface-level glance at your accounts. It requires a deep dive into the technical hurdles your team has overcome. By combining financial expertise with industry-specific knowledge, we ensure that your claim is robust, compliant, and maximised to reflect the true value of your R&D efforts.

The Recoup Technical Assessment Process

The core of our methodology lies in our technical interviews. We sit down with your competent professionals to extract the technical "advance" that might otherwise remain hidden in project logs. This process is particularly vital in sectors like construction or food technology, where innovation is often woven into the fabric of daily problem-solving rather than occurring in a laboratory. As experienced R&D tax credit specialists UK, we know how to identify qualifying activities in environments where the work feels like "just doing the job". We help your team articulate their breakthroughs in a way that meets the high bar set by the 2024 merged scheme requirements.

Transforming Innovation into Strategic Capital

We believe that R&D tax relief should be viewed as a strategic asset for future growth rather than a one-off windfall. The capital recovered through a successful claim can be reinvested into new equipment, talent, or further research, creating a cycle of continuous innovation. Our commitment to "enquiry-proofing" means we build every claim to withstand the highest levels of scrutiny. We provide the institutional credibility you need to claim with confidence, transforming your technical challenges into a powerful tool for business expansion. If you are ready to explore the potential within your latest project, you can book a no-cost introductory consultation to begin your journey toward capital recovery.

Transform Your Technical Hurdles into Strategic Growth

Determining whether your latest development meets the threshold for tax relief is a strategic decision that can reshape your company's financial future. By now, you should have a clearer perspective on the central question: is my project an advance in science or technology? Success depends on moving beyond routine adaptation and identifying the genuine technical uncertainties that forced your team to innovate. When you document these challenges through a systematic framework, you transform technical roadblocks into robust evidence for capital recovery.

Recoup Capital acts as your protective guide, ensuring your claim is built on institutional credibility and expert analysis. Our team of specialist chartered tax accountants and technical experts provide proactive HMRC enquiry support, giving you the peace of mind to pursue the relief you deserve. Because we operate on a success-based fee structure, you can explore your eligibility without any upfront financial risk. This partnership-oriented approach allows us to focus entirely on delivering value through results.

Discover if your project qualifies with a specialist R&D assessment and start reframing your innovation as a strategic asset for long-term growth. Your technical breakthroughs deserve to be recognised and rewarded.

Frequently Asked Questions

Is my project an advance if it has already been done by a competitor?

Yes, you can still qualify if a competitor's solution is not publicly available or is held as a trade secret. When asking is my project an advance in science or technology, the focus is on whether the knowledge was accessible to your team. If you cannot find the answer in the public domain, your work represents a genuine attempt to increase the overall knowledge in your field.

Can I claim for an advance in science if my project failed to reach its goal?

Failed projects are often the strongest candidates for tax relief because they demonstrate undeniable scientific or technological uncertainty. If your project failed to reach its goal despite a systematic approach, you've still gained knowledge about what doesn't work. HMRC recognises that R&D is inherently risky; as long as you were seeking an advance, the costs remain qualifying under the current rules.

Does "new to my company" count as an advance for R&D tax credits?

Simply being "new to your company" does not qualify as an advance for R&D tax credits. To meet the threshold, your project must aim to increase the overall knowledge or capability in the wider field of science or technology. If a competent professional in your industry could've readily solved the problem using existing tools or public knowledge, it's considered standard practice rather than R&D.

What is the "Competent Professional" test in an R&D claim?

The Competent Professional test is a benchmark used to determine if a project's hurdles were truly difficult. HMRC looks for the opinion of someone with relevant qualifications and experience who can confirm the solution wasn't obvious. This individual helps define whether the question is my project an advance in science or technology can be answered with a "yes" based on industry-wide standards.

How much detail does HMRC require to prove a technological advance?

HMRC requires significant detail through the mandatory Additional Information Form (AIF) and a supporting technical report. You must baseline the current state of technology, define the specific uncertainties, and outline the systematic testing performed. Vague descriptions won't suffice; you need to provide technical metrics and data that clearly articulate the advance in knowledge your project achieved during the relevant accounting period.

Can software development be considered an advance in technology?

Software development is frequently considered a technological advance if it involves overcoming technical hurdles rather than just functional ones. Creating a new user interface might be innovative, but it isn't R&D. However, developing new algorithms, improving data processing speeds beyond current limits, or integrating incompatible legacy systems often requires the resolution of genuine technological uncertainty that a professional couldn't easily solve.

Is a commercial improvement the same as a technological advance?

A commercial improvement is not the same as a technological advance. Commercial success might involve better branding, lower price points, or aesthetic changes that appeal to customers. A technological advance, however, must involve an increase in the underlying capability or knowledge of the technology itself. HMRC only provides relief for the latter, focusing on the technical "how" rather than the commercial "what".

What happens if HMRC disagrees that my project was an advance?

If HMRC disagrees with your assessment, they may open an enquiry to scrutinise your claim further. This is why having a robust technical report and real-time documentation is so vital for every project. When you partner with specialists, you receive proactive enquiry support to defend your position. We help you present the technical facts clearly to ensure your innovation is correctly recognised.