How to Calculate Patent Box Relief: A Comprehensive 2026 UK Guide

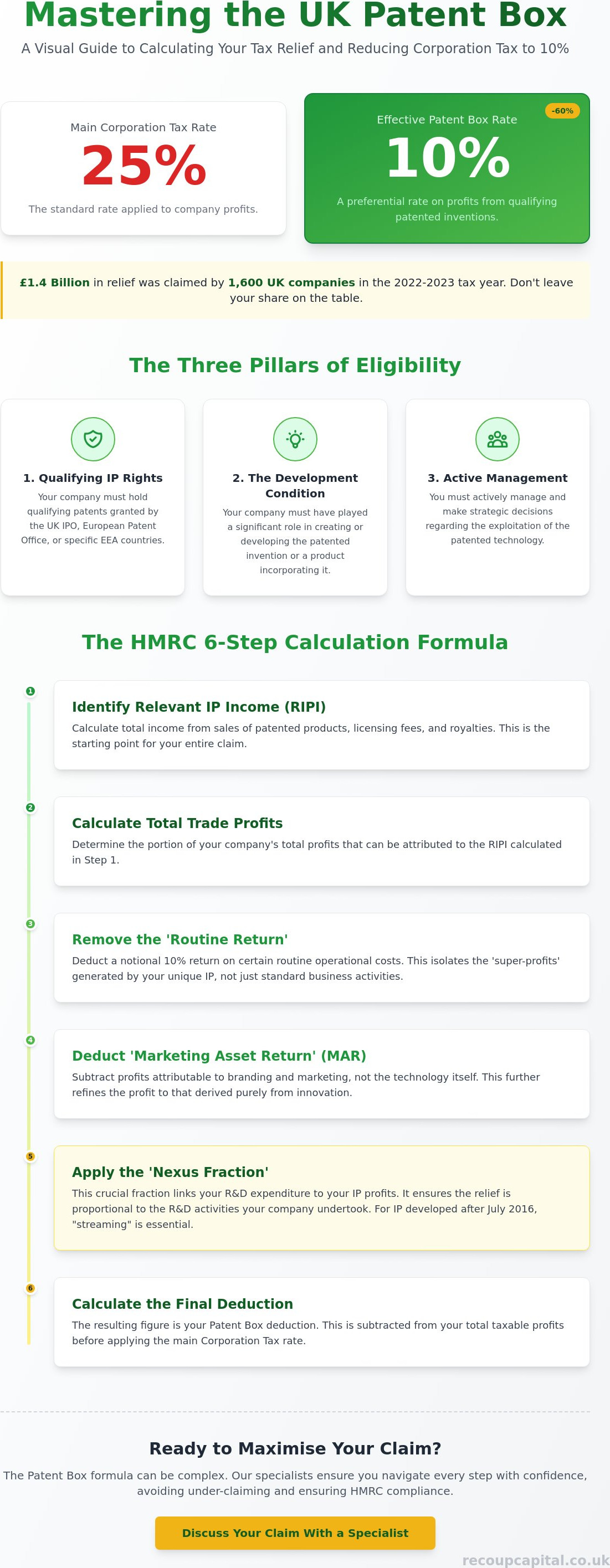

With the main Corporation Tax rate at 25%, leaving your intellectual property's tax potential untapped is a strategic oversight that costs UK innovators millions every year. In the 2022 to 2023 tax year alone, 1,600 companies successfully claimed over £1.4 billion in relief. Despite this, many directors find HMRC's technical jargon a significant barrier to entry. Mastering how to calculate patent box relief is the vital bridge between your past innovation and your future commercial growth.

It's common to feel that your breakthrough technology is trapped behind complex compliance hurdles or the fear of under-claiming. This guide provides a clear roadmap to securing the 10% preferential tax rate, ensuring your business retains more profit for reinvestment. We'll walk you through the mandatory six-step formula, the intricacies of the Nexus Fraction, and the latest 2026 compliance requirements. You'll gain the clarity needed to discuss your claim with a specialist and the confidence to transform your patents into high-impact strategic assets.

Key Takeaways

- Discover how to reduce your effective Corporation Tax rate to 10% by correctly categorising your Relevant IP Income from sales and royalties.

- Master the mandatory 6-step HMRC formula to gain a clear, step-by-step understanding of how to calculate patent box relief.

- Learn how the Nexus Fraction serves as a vital link between your past R&D expenditure and your current commercial success.

- Understand why the "streaming" method is now essential for managing any intellectual property developed or acquired after July 2016.

- Build the confidence to discuss your claim with a specialist, ensuring you don't under-claim or fall foul of the latest compliance updates.

Understanding the Patent Box: Why Calculation Accuracy Matters in 2026

The UK government designed the Patent Box scheme to keep high-value innovation and its commercial rewards within the country. Since the main rate of Corporation Tax reached 25%, the incentive's value has surged. It offers a 10% effective tax rate on profits from patented inventions, representing a massive 60% reduction in the tax due on those specific earnings. Success in 2026 relies on more than just having a patent; it requires a surgical approach to your financial data. Understanding how to calculate patent box relief correctly ensures you don't leave money on the table or invite unnecessary scrutiny from HMRC.

This relief is the natural successor to the R&D claim. We often see it as a financial lifecycle. You'll find R&D tax credits explained as the fuel for your initial technical breakthroughs, whilst the Patent Box acts as the reward for turning those breakthroughs into a profitable market presence. Using both together creates a holistic tax strategy that protects your cash flow at every stage of growth. Precision in your maths transforms a complex regulatory requirement into a powerful tool for capital recovery.

The Core Objective of the Calculation

The calculation isn't simply a matter of applying a discount to your total tax bill. Its primary purpose is to isolate the "super-profits" that only exist because of your protected intellectual property. HMRC requires you to separate your innovative profits from your routine business profits. Routine profits are the earnings any company would expect to make by performing similar activities without the benefit of unique IP. By stripping these away, you identify the specific value your patent adds to the bottom line. It's a forensic exercise that ensures the 10% rate only applies to the portion of profit truly created by your innovation.

Eligibility Check: The Foundation of Your Maths

Your calculation is only as strong as your eligibility. Before you start the maths, you must verify three critical pillars:

- Qualifying IP Rights: Your patents must be granted by the UK Intellectual Property Office, the European Patent Office, or specific EEA countries.

- The Development Condition: Your company must have played a significant role in creating or developing the IP. Simply owning a patent isn't enough; you must show you contributed to its evolution.

- Active Management: If your company is part of a larger group, you must demonstrate that you have a hand in the strategic decisions regarding the IP's development and application.

Establishing these facts is the first step in learning how to calculate patent box relief with total confidence. Without this foundation, even the most meticulous profit allocation will fail to meet HMRC's compliance standards.

The 6-Step Formula: How to Calculate Patent Box Relief

Mastering the mechanics of the claim requires following a strict, sequential process. It's not a one-size-fits-all percentage; it's a filtration system. By applying these six steps, you distill your gross earnings down to the specific profit that qualifies for the 10% rate. Learning how to calculate patent box relief involves navigating these stages with precision to ensure your CT600 tax return remains compliant whilst maximising your capital recovery.

The standard formula consists of these distinct phases:

- Step 1: Identify Relevant IP Income (RIPI) from sales, royalties, and licences.

- Step 2: Calculate the "Total Profits" of the trade associated with that income.

- Step 3: Remove the "Routine Return" to find the residual profit.

- Step 4: Deduct the "Marketing Asset Return" to isolate technology-driven profit.

- Step 5: Apply the "Nexus Fraction" to account for your R&D investment history.

- Step 6: Calculate the final Patent Box deduction for your tax return.

This process ensures that the tax benefit is strictly tied to the innovation itself rather than general business activity or brand power. If the maths feels daunting, you can always speak with our corporate finance specialists to clarify your specific figures before submitting.

Step 1: Defining Your Relevant IP Income (RIPI)

RIPI is the bedrock of your claim. It includes more than just the direct sale of a patent. You can include income from the sale of any item that incorporates a patented component, even if the patent only applies to a small part of the overall product. Licensing fees and royalties are obvious inclusions, but you shouldn't overlook revenue from patent infringement awards or insurance payouts related to your IP. According to the ICAEW guidance on Patent Box, identifying these diverse income streams early is vital for building a robust and defensible claim.

Step 3 & 4: Removing Non-IP Influences

HMRC requires you to strip away profits that don't stem directly from your technical innovation. First, you must calculate a "routine return," which is typically 10% of specific tax-deductible expenses like staffing and premises, though R&D costs are excluded from this particular deduction. Next, you must account for "marketing assets." This step removes the profit attributed to your brand name, trademarks, or market reputation. The Non-Marketing Return (NMR) is the profit remaining after both the routine return and the value of marketing assets have been stripped away. This final figure represents the pure "innovative profit" that the Patent Box regime aims to reward.

Deciphering the Nexus Fraction: Linking R&D Spend to IP Profit

The Nexus Fraction is often the most misunderstood element of the entire regime. It acts as a vital safeguard, ensuring that the tax benefits remain proportional to the actual R&D work performed by your company. HMRC uses this fraction to verify that you earned the relief through genuine innovation rather than simply acquiring a patent to reduce your tax liability. If you've already mastered the process of claiming R&D tax credits, you have a significant head start. The data used for those claims forms the financial backbone of your nexus calculation.

The core formula is expressed as your qualifying R&D expenditure plus a 30% uplift, divided by your qualifying expenditure plus acquisition costs and outsourced R&D to connected parties. The result is capped at 1. If your company performs all its R&D in-house, your fraction will likely be 1, allowing you to apply the full 10% rate to your identified profits. Understanding this ratio is a pivotal part of learning how to calculate patent box relief effectively and ensuring your claim reflects your true investment.

Maintaining high standards in your reporting is essential for a successful claim. You must align your internal documentation with the latest HMRC R&D tax claim transparency standards to ensure your fraction stands up to rigorous scrutiny during an enquiry.

Qualifying vs Non-Qualifying Expenditure

The numerator of your fraction focuses on what HMRC considers "good" costs. These include in-house R&D staff wages, materials, and subcontracting costs paid to unconnected third parties. The denominator includes these same figures but adds "bad" costs, such as the price paid to acquire the IP or R&D work outsourced to connected group companies. To protect businesses from being unfairly penalised for minor acquisition costs, the "30% Uplift" rule allows you to increase your qualifying expenditure in the numerator. This uplift often neutralises the impact of small external costs, keeping your fraction as close to 1 as possible.

Tracking R&D Spend for Patent Box

Precision is your best defence against a rejected claim. You must track your R&D expenditure for the entire life of the patent, which often spans several years before a product reaches the market. This isn't just about monitoring total spend. You need to attribute specific costs to individual patent "streams" or product families. A common pitfall for many businesses is failing to maintain these records consistently over multiple accounting periods. If you cannot prove which R&D spend relates to which specific patent, you risk a lower fraction and a smaller tax saving. Robust, real-time record-keeping is the only way to ensure you're learning how to calculate patent box relief with accuracy and long-term security.

Streaming vs Formulaic Methods: Choosing the Right Approach for Your Business

The landscape of Patent Box changed significantly with the introduction of the "New Regime." While the old formulaic approach allowed businesses to group all IP profits together, HMRC now demands a more granular view. If you are exploring how to calculate patent box relief today, you are almost certainly operating under the mandatory streaming rules. This method requires you to separate income and costs for every individual patent or product family. It ensures the tax relief directly mirrors the R&D investment for that specific asset, creating a clear nexus between your innovation and your reward.

Adopting this method requires a shift in how you view your profit and loss statements. You can no longer look at your innovative trade as a single block of activity. Instead, you must treat each patented product or process as its own micro-business for tax purposes. This level of detail provides HMRC with the transparency they require whilst giving you a clearer picture of which R&D projects are delivering the highest tax-efficient returns.

When is Streaming Mandatory?

Since 1 July 2016, the streaming method has been the only option for new entrants to the scheme. The transitional period for "old" IP, which included intellectual property created before that date, has now concluded. For your 2026 tax filings, streaming is the universal standard. If your business manages multiple disparate IP assets, you must track them separately. However, HMRC does allow for "Product Families." This is particularly useful when multiple patents cover a single item, allowing you to stream income at a product level rather than for every individual patent number. It keeps the administration manageable whilst maintaining the required transparency.

Organising Your Data for Streaming

Streaming demands a more sophisticated accounting setup than the old methods. You must be able to apportion indirect costs, such as overheads or administrative bills, across different IP streams based on a reasonable and consistent metric. Handling "Mixed Income" is another common hurdle. If only one component of a larger system is patented, you must identify the portion of the sale price attributable to that specific innovation. It's a detailed process, but it often yields more accurate relief. It prevents loss-making products from diluting the profits of your most successful inventions, ensuring your Relevant IP Profit (RP) is maximised.

| Feature | Old Formulaic Method | Mandatory Streaming (New Regime) |

|---|---|---|

| Scope | Aggregated across all IP. | Separated per patent or product family. |

| Eligibility | IP created before 1 July 2016. | Mandatory for all IP in 2026. |

| Precision | Generalised and simplified. | Granular and R&D-linked. |

If your internal systems aren't yet configured for this level of detail, we can help. Our team can assist you in structuring your corporate finance to ensure every penny of your Relevant IP Profit is captured and protected.

Maximising Your Claim: How Recoup Capital Simplifies the Calculation

The transition from understanding the theory to executing a compliant claim is where most businesses stumble. Whilst mastering how to calculate patent box relief is essential for any innovative company, the sheer volume of data required for the six-step process often leads to significant under-claiming. Many directors settle for conservative figures to avoid HMRC scrutiny, essentially leaving valuable capital on the table. By partnering with specialised R&D tax credit consultants, you transform this administrative burden into a streamlined strategic advantage.

We don't view your patent profits in isolation. A truly effective tax strategy integrates these savings with other incentives like Capital Allowances to maximise your total recovery. This holistic approach is a core part of our Corporate Finance advisory. It ensures your tax position supports your long-term growth objectives rather than just providing a one-off refund. Our success-based fee model reflects this partnership-first philosophy; we only succeed when your business secures the relief it deserves.

The Recoup Capital Methodology

Our process begins with a forensic analysis of your R&D expenditure. We don't just look at the surface. We dig deep into your project history to optimise the Nexus Fraction, ensuring every qualifying hour of work is accounted for. This forensic approach is the most reliable way to master how to calculate patent box relief without risking non-compliance. We provide end-to-end support, from the initial identification of qualifying IP rights through to the final submission to HMRC. Our team builds a comprehensive defence file for every claim, acting as a protective guide to insulate your business from the stress of potential enquiries.

Next Steps for Your Innovation Strategy

Your journey starts with a clear assessment of your current IP portfolio to determine its Patent Box readiness. We invite you to arrange a no-obligation consultation with our team to estimate your potential savings and discuss your eligibility. Securing a 15% reduction in your Corporation Tax rate provides more than just a lower bill. It creates a strategic asset that you can reinvest directly back into your next innovation cycle, fuel your expansion, or strengthen your market position. We're here to ensure your intellectual property works as hard for your balance sheet as it does for your customers.

Transforming Your Intellectual Property into Strategic Capital

Securing an effective 10% Corporation Tax rate is a powerful way to fuel your next cycle of innovation. By mastering mandatory streaming and the Nexus Fraction, you ensure your business remains compliant whilst recovering vital capital. Precision is everything. Understanding how to calculate patent box relief is the first step toward turning technical breakthroughs into long-term financial assets. These savings shouldn't be viewed as a mere refund; they're a strategic tool for future expansion.

Our team of chartered tax accountants and R&D specialists is ready to guide you through every stage of the process. With offices in London and Manchester, we provide national coverage. We operate on a success-based fee structure. This means we only win when you do. If you're ready to unlock the full value of your IP, contact Recoup Capital for a professional Patent Box assessment. Let's work together to transform your regulatory obligations into a robust engine for business growth.

Frequently Asked Questions

What is the Patent Box effective tax rate in 2026?

The effective tax rate for profits qualifying under the Patent Box regime is 10% in 2026. This provides a substantial 15% saving compared to the main Corporation Tax rate of 25%. It's a powerful incentive designed to reward businesses that choose to commercialise their technical breakthroughs within the UK rather than moving production abroad.

Can I claim Patent Box relief if my patent is still "pending"?

You cannot receive the tax reduction whilst a patent is still pending; it must be officially granted first. However, you should track the profits earned during this pending period. Once the patent is granted, you can include those accumulated profits in your first Patent Box claim, provided you elect into the scheme within the strict two-year deadline.

How does the Patent Box calculation interact with R&D tax credits?

These two incentives work together throughout the innovation lifecycle. Your history of claiming R&D tax credits is vital because those costs directly influence the Nexus Fraction. A higher ratio of in-house R&D spend typically results in a more favourable outcome when you're determining how to calculate patent box relief for your commercialised products.

Is the Patent Box calculation mandatory for all UK companies?

No, the Patent Box is an optional tax incentive that requires a formal election. Your company must choose to enter the regime by notifying HMRC in writing. Whilst the calculation is complex, the potential for a 60% reduction in your tax bill on innovative profits makes it a highly attractive choice for most intellectual property-rich businesses.

What happens if my Patent Box calculation results in a loss?

If your calculation results in a loss, that loss is carried forward to be offset against future profits within the same IP stream. You cannot use a Patent Box loss to reduce your general trading profits. This "streaming" requirement ensures that the tax benefits and risks remain strictly tied to your specific innovative activities.

Can I include profits from patents registered outside the UK?

Yes, patents granted by the European Patent Office (EPO) or specified intellectual property offices in the European Economic Area (EEA) qualify for the relief. You aren't restricted solely to UK Intellectual Property Office grants. This allows companies with a broader international protection strategy to benefit from the preferential 10% rate on their global commercial activities.

How far back can I backdate a Patent Box claim?

You generally have two years from the end of the accounting period in which the profits arose to make an election. Regarding backdating, you can capture profits from the period whilst the patent was pending, provided the application was ultimately successful. This ensures you don't lose out on tax relief during the often lengthy wait for an official grant.

Do I need a specialist accountant to calculate Patent Box relief?

Whilst you aren't legally required to use a specialist, the technical nature of the 6-step formula makes professional guidance a wise investment. Accurate record-keeping and a deep understanding of how to calculate patent box relief are essential to avoid HMRC enquiries. A specialist ensures you maximise your claim whilst maintaining total compliance with the latest 2026 regulations.