Embedded Capital Allowances on Fixtures: Unlocking Hidden Tax Relief in 2026

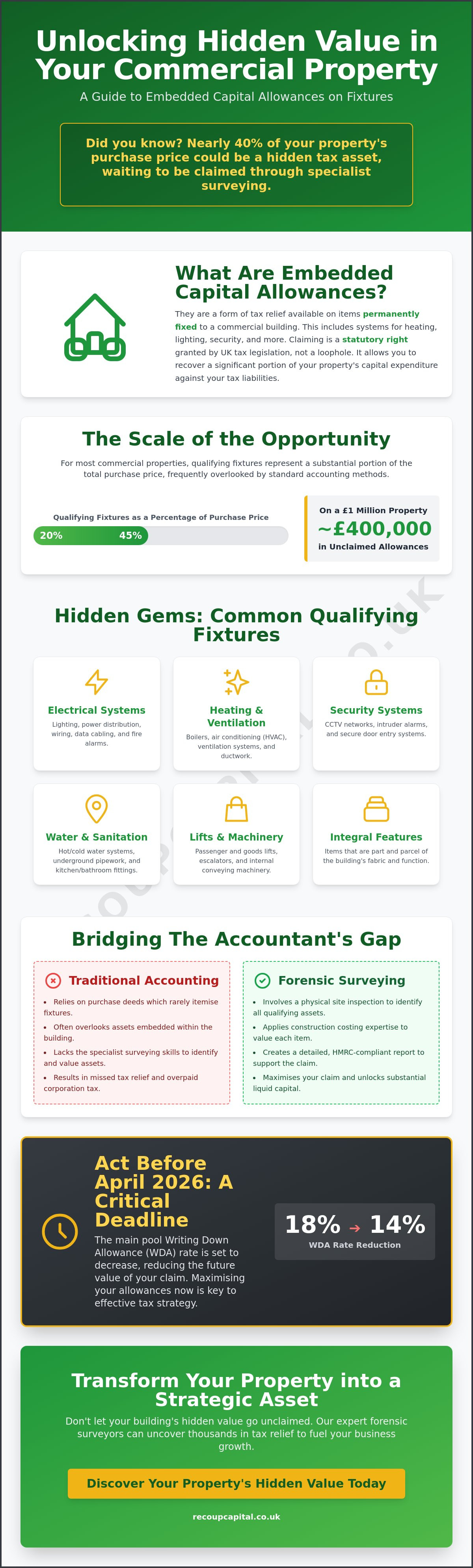

What if nearly 40% of your commercial property’s purchase price was actually a hidden tax asset that your current accounting records haven't yet touched? It's a frustrating reality for many owners who see high corporation tax bills arrive whilst they continue to invest in expensive building improvements. You likely feel that distinguishing between a simple repair and a qualifying capital improvement is an impossible task without a dedicated team of specialists at your side.

This guide will show you how to identify and claim thousands of pounds in tax relief by uncovering embedded capital allowances on fixtures through professional forensic surveying. With the main pool Writing Down Allowance set to decrease from 18% to 14% in April 2026, there's never been a more critical time to ensure your claims are both maximised and HMRC-compliant. We'll examine how permanent reliefs like the 50% special rate allowance can transform your building’s integral features into strategic liquid capital, providing the professional assurance you need to reinvest in your firm's future growth.

Key Takeaways

- Identify the high-value assets permanently fixed within your property that typical accounting methods often overlook.

- Discover how to unlock substantial hidden relief by identifying embedded capital allowances on fixtures through specialist forensic surveying.

- Navigate the 2026 statutory updates to ensure your claims remain HMRC-compliant whilst maximising your available tax deductions.

- Learn why a physical site inspection is essential for bridging the gap between a standard purchase deed and a robust, forensic tax claim.

- Reframe recovered tax as a strategic asset to fuel business growth and complement other incentives like R&D Tax Credits.

Unlocking Hidden Value: What Are Embedded Capital Allowances on Fixtures?

Imagine your commercial property as a collection of separate financial assets rather than a single brick-and-mortar structure. While your accountant likely handles the obvious items like desks or computers, a significant portion of your building's value remains locked within its very fabric. These are embedded capital allowances on fixtures. Specifically, these allowances represent tax relief on items that are permanently fixed to a commercial building, such as heating systems, security alarms, and lighting. Unlike movable equipment that sits on the floor, these assets are legally part of the property, yet they qualify for relief under the same Capital Allowances framework that governs machinery.

It's vital to understand that this is a statutory right granted by UK tax legislation. It isn't a "loophole" or a creative accounting trick. The scale of the opportunity is often startling. For most commercial properties, qualifying fixtures typically represent between 20% and 45% of the total purchase price. If you bought a property for £1 million, you could be sitting on £400,000 of unclaimed tax relief. Failing to claim embedded capital allowances on fixtures effectively means leaving your own money on HMRC's table whilst your business faces rising operational costs.

The Anatomy of an Embedded Fixture

An asset qualifies as "embedded" when it becomes part and parcel of the building fabric. The legal test often rests on the method of attachment. If removing the item would cause significant damage to the building's structure or the asset itself, it likely qualifies. We frequently uncover overlooked items like lift shafts, underground pipework, and bespoke ventilation systems. These are assets that standard purchase deeds fail to itemise, leaving them invisible to traditional bookkeeping. By using forensic surveying, we can identify these hidden components and assign them a value that HMRC accepts.

Why 2026 Is a Critical Year for Property Owners

The regulatory landscape for 2026 has introduced stricter HMRC compliance standards that require immediate attention. With the main pool Writing Down Allowance (WDA) rate reducing from 18% to 14% in April 2026, the timing of your claim directly affects its net present value. Delaying a claim isn't just a missed opportunity; it's a risk to your cash flow. Under current "pooling" requirements, if you don't identify and value these fixtures within specific windows, you may lose the right to claim them forever. Professional Capital Allowances surveying ensures you capture this value before it expires, transforming historical expenditure into a strategic business tool.

The Statutory Framework: Distinguishing Between Plant, Machinery, and Integral Fixtures

The Capital Allowances Act 2001 serves as the bedrock for all property-based tax relief, but the legislative landscape is shifting. Successfully claiming embedded capital allowances on fixtures requires a granular understanding of how HMRC classifies building components. Under the current framework, assets are generally split between the "Main Pool" and the "Special Rate Pool." The distinction is critical because it dictates the speed at which you can recover your capital. According to HMRC's definition of a fixture, an item must be installed in such a way that it becomes part of the land or building. This legal test determines whether an asset is merely a piece of equipment or a qualifying fixture that stays with the property.

A common hurdle in property transactions is the "Fixed Value" requirement. When a commercial building changes hands, both the buyer and seller must agree on the value of the fixtures via a Section 198 election. This must be completed within two years of the purchase. If this step is missed, the buyer may be permanently barred from claiming relief on those specific assets. Establishing this value early ensures that the tax benefits are preserved as strategic assets for the new owner rather than being lost to administrative oversight.

The Integral Features List: Hidden Gems in Your Building

Integral features are the most frequent source of successful claims. These include electrical systems, such as lighting and power distribution; cold water systems; and space or water heating infrastructure. High-value assets like lifts, escalators, and even powered walkways also fall into this category. Because these items are "integral" to the building's operation, they qualify for relief even though they are part of the permanent structure. Identifying these requires a specialised eye, as they are often buried deep within the construction costs.

Writing-Down Allowances (WDA) Explained

The rate of relief depends on the asset's classification. Currently, the main pool attracts an 18% WDA, while the special rate pool, which includes most integral features, sits at 6%. However, from April 2026, the main pool rate will decrease to 14%, making it vital to accelerate claims where possible. The Annual Investment Allowance (AIA) remains a powerful tool, providing 100% relief on qualifying expenditure up to a £1 million limit. If you're unsure which pool your assets fall into, a specialist review of your Capital Allowances position can provide the clarity needed to protect your investment. Managing these pools effectively also helps mitigate "balancing charges" when you eventually decide to dispose of the property.

The Accountant’s Gap: Why Embedded Fixtures Are Frequently Overlooked

Most business owners trust their accountants to handle every facet of their tax strategy. It's a logical partnership. However, a fundamental gap exists between general accountancy and forensic tax surveying. Your accountant is an expert in financial reporting and compliance, but they aren't typically trained to conduct a physical survey of a building's infrastructure. Most embedded capital allowances on fixtures are missed simply because they don't appear as individual line items on a purchase invoice or a standard completion statement. A purchase deed usually lists the property as a single lump sum. HMRC requires granular, evidence-based detail to justify a claim, and a standard set of accounts simply doesn't provide it.

This information gap often leads to "lazy" claims. These are filings that only account for the most obvious movable assets, such as office furniture or loose equipment. Whilst these claims are valid, they represent the tip of the iceberg. By ignoring the complex systems integrated into the building fabric, businesses leave substantial sums of money unclaimed. Recoup Capital bridges this gap by merging property valuation expertise with a deep understanding of tax law. We don't just review your ledger; we physically inspect the property to ensure every qualifying asset is accounted for.

The Limitations of Traditional Bookkeeping

Cost segregation is a specialist discipline rarely covered in standard accounting qualifications. It involves breaking down a property's purchase price into its component parts to identify qualifying expenditure. Relying on historical depreciation figures for tax purposes is a common pitfall. Tax law allows for relief based on the actual value of fixtures at the point of purchase, which may differ significantly from book value. When these fixtures remain unidentified, they sit as "dead capital" on your balance sheet, providing no benefit to your cash flow or reinvestment plans.

Addressing the "Already Done" Misconception

Many clients initially believe they've already claimed everything possible. It's a common misconception. Most general tax filings only capture assets purchased *after* the property was acquired. The significant relief usually lies in the assets that were already inside the building when you bought it. Your solicitor may have used a Section 198 election to fix a value during the transaction, but without specialist input, they might have inadvertently capped your claim at a nominal amount. Seeking a second opinion on your Capital Allowances position often uncovers 50% more value than a standard filing, transforming overlooked pipework and cabling into tangible liquid assets for your business.

The Forensic Surveying Process: How to Identify and Value Hidden Assets

Desktop reviews simply can't capture the full scope of embedded capital allowances on fixtures. To transform hidden infrastructure into a strategic business asset, a physical site inspection is non-negotiable. This process relies on quantity surveying principles to estimate the historical costs of items that aren't itemised in your purchase contracts. Because you bought the building as a whole, we use a "just and reasonable" apportionment method. This calculation isolates the value of qualifying plant and machinery from the non-qualifying land and structure. It ensures your claim is mathematically sound and legally defensible.

The complexity of modern commercial properties means that many qualifying items are literally buried behind walls or under floors. Standard accounting software won't flag the value of a specialised ventilation system or the electrical distribution boards hidden in a basement. Forensic surveying bridges this gap by applying construction cost data to the specific assets found within your building. This evidence-based approach is what distinguishes a successful capital recovery from a missed opportunity. It provides the granular detail HMRC expects in 2026, turning vague property costs into precise tax relief figures.

Step-by-Step: From Site Visit to Tax Submission

The journey begins with meticulous data collection. We gather your floor plans, purchase contracts, and any existing invoices for past refurbishments. Once the groundwork is laid, a specialist surveyor visits your property to identify every qualifying asset. This isn't a cursory glance. We examine everything from air conditioning units and fire alarm systems to specialised flooring and pipework. Finally, our technical team applies the correct tax treatment to every identified asset, ensuring each item is placed in the correct pool to maximise your return.

HMRC Compliance and the "Technical Report"

In 2026, a robust technical report is your primary shield against HMRC scrutiny. HMRC expects more than just a list of assets; they require a comprehensive document that explains the methodology used for valuation. A high-quality report must include detailed descriptions of the fixtures, photographs from the site survey, and explicit references to relevant case law. These legal citations justify why specific items qualify as plant or machinery under the Capital Allowances Act. It's about providing a clear, logical narrative that proves your eligibility.

Recoup Capital manages this entire liaison process with HMRC on your behalf. We handle any queries that arise, providing professional assurance that your claim remains compliant whilst delivering the best possible outcome for your cash flow. If you're ready to uncover the hidden value in your building, you can book a specialist capital allowances assessment to start the process today.

Strategic Capital Recovery: Integrating Allowances into Your 2026 Tax Strategy

Tax efficiency shouldn't exist in a vacuum. Successful firms view embedded capital allowances on fixtures as a core component of their annual financial planning rather than a one-off windfall. Correctly identifying these assets reduces your taxable profit on the CT600 corporation tax return. This directly improves your bottom line and frees up liquidity that would otherwise be lost to tax. Recovered capital becomes a strategic tool for reinvestment. Whether you're upgrading machinery, expanding your team, or funding new product development, the cash flow benefits are immediate. Our success-based fee model ensures a risk-free approach for every client. We demonstrate value through results, creating a partnership-oriented experience that prioritises your long-term business growth.

Synchronising R&D and Capital Allowances

Many businesses don't realise that property improvements and innovation often overlap in ways that double your tax benefits. If you're developing specialised engineering centres, commercial kitchens, or high-tech labs, you may be eligible for both R&D tax credits and capital allowances. Whilst R&D relief focuses on the "people" and "process" costs of innovation, capital allowances cover the physical infrastructure required to house those activities. Recoup Capital’s specialists work across both disciplines to provide a comprehensive view of your tax position. This unified strategy ensures no overlap is missed and no relief is double-counted. It maximises your total recovery and ensures your property works as hard as your research team.

Next Steps: Securing Your Business’s Financial Future

Securing these reliefs isn't an intimidating procedure when you have the right partner to handle the technical details. We begin with a no-obligation "scoping" review of your property portfolio. This process identifies the potential value of your embedded capital allowances on fixtures before you commit to a full claim. To prepare for a capital allowances consultation, simply gather your property purchase contracts and any high-level floor plans you have on file. Our team handles the rest. We manage everything from forensic surveying to final HMRC submission and liaison. We act as your protective guide through the regulatory landscape, ensuring transparency at every stage. Ready to transform your building's hidden assets into strategic capital? Book a consultation with our specialist team today and secure your business's financial future.

Transform Your Property into a Strategic Tax Asset

Identifying the hidden value within your building's fabric is more than a simple tax exercise; it's a vital step in securing your firm's financial resilience. Commercial properties often contain substantial amounts of "invisible" capital that standard accounting methods simply aren't designed to capture. By uncovering embedded capital allowances on fixtures, you turn your property's infrastructure into a strategic asset that fuels reinvestment and growth. With the 2026 legislative shifts already in motion, the urgency to audit your property portfolio has never been higher.

Recoup Capital provides a risk-free path to recovery through our success-based fee model. Our team of chartered tax accountants and forensic surveyors brings the technical depth required to maximise your claim whilst ensuring total HMRC compliance. We've built a solid track record by transforming complex regulatory requirements into approachable growth opportunities for our partners. Don't let your capital remain locked in the walls of your property. Book a specialised Capital Allowances consultation today and let us help you turn historical expenditure into a powerful strategic asset for your business's future.

Frequently Asked Questions

What are embedded capital allowances on fixtures?

These are tax reliefs available on plant and machinery that are permanently fixed to a commercial building. Whilst movable items like desks are easily identified, embedded capital allowances on fixtures apply to the "invisible" assets like electrical systems, plumbing, and lift installations. These items are typically part of the building's purchase price and require specialist surveying to identify and value for HMRC purposes.

Can I claim for fixtures if I bought the property years ago?

Yes, you can often make a claim even if the property was acquired many years ago. As long as you still own the building and the qualifying fixtures are still in use, the relief remains available. There is no time limit on how far back you can go to identify these assets, provided they haven't been claimed by a previous owner or already processed in your historical tax returns.

Why hasn’t my accountant already claimed for these embedded assets?

Most accountants focus on the purchase price as a single figure because land and buildings don't appear as individual components on a standard invoice. Identifying embedded capital allowances on fixtures requires a physical site survey and quantity surveying expertise to estimate historical costs. Accountants generally lack the specialist surveying tools and construction cost data needed to meet HMRC's stringent reporting requirements for these specific claims.

Will claiming capital allowances affect my future Capital Gains Tax (CGT)?

Claiming these allowances does not normally increase your Capital Gains Tax liability when you sell the property. HMRC rules generally allow you to claim capital allowances without reducing the base cost of the building for CGT purposes. This means you can enjoy the immediate cash flow benefits of the tax relief without being penalised when you eventually decide to dispose of the asset.

What types of commercial properties qualify for embedded fixture claims?

Almost any commercial property owned by a UK taxpayer qualifies for these claims. Common examples include offices, retail units, warehouses, and hotels. Specialist buildings such as care homes, dental practices, and manufacturing facilities often yield the highest returns due to the density of complex mechanical and electrical systems. If you pay corporation tax and own a commercial building, a claim is likely possible.

How much does a forensic capital allowance survey cost?

We operate on a success-based fee model to ensure the process is entirely risk-free for your business. This means our costs are typically a percentage of the actual tax saving we secure for you. We don't charge upfront for the initial scoping review; we prefer to demonstrate our value through results rather than through traditional consulting fees.

What is the "pooling" requirement for capital allowances on fixtures?

The pooling requirement states that a seller must "pool" the expenditure on fixtures in their tax return before a sale is completed. This ensures that the value of the fixtures is clearly established and agreed upon by both parties. If this step is missed during a transaction, the buyer may lose the right to claim any future allowances on those specific fixtures.

How long does the capital allowance claim process take?

A typical claim takes between eight and twelve weeks from the initial site survey to the final HMRC submission. This timeline allows for a thorough data collection phase, a physical inspection of the property, and the compilation of a robust technical report. Once submitted, the relief is usually reflected in your next corporation tax return or as a refund for previous years.