How to Avoid an HMRC R&D Enquiry: A Comprehensive Guide for 2026

Did you know that while HMRC enquiry rates have dipped to 17 percent, the intensity of each investigation has reached an all-time high? It's a daunting figure for any business leader who values their time and professional standing. You likely feel that the threat of a financial clawback or a heavy administrative burden shouldn't be the price of claiming your rightful incentives. Understanding how to avoid an HMRC R&D enquiry is no longer about staying under the radar; it's about building a robust, evidence-based narrative that satisfies the latest 2026 compliance standards. We agree that your innovation deserves to be rewarded without the stress of a looming audit hanging over your accounts.

This guide promises to show you the strategic steps and rigorous documentation standards required to protect your claims from scrutiny. We'll preview the mandatory Additional Information Form (AIF) requirements, the nuances of the 30 percent R&D intensity threshold, and the specific methodologies that lead to a clean claim. By the end, you'll have the confidence to treat your tax credits as a strategic asset for growth rather than a regulatory gamble.

Key Takeaways

- Understand the transition from random sampling to targeted "volume compliance" to better anticipate HMRC's modern scrutiny methods.

- Discover how to avoid an HMRC R&D enquiry by identifying common red flags, such as data inconsistencies and high-risk sector profiles, before you submit.

- Learn why contemporaneous documentation is non-negotiable and how real-time record-keeping prevents the rejection of retrospective claim re-creations.

- Implement a proactive "Technical Uncertainty" audit to ensure your innovation narratives align perfectly with the latest 2026 HMRC guidelines.

- Shift the focus from mere paperwork to strategic capital recovery by leveraging specialised expertise that protects your business from financial clawbacks.

Understanding the Shift: Why HMRC R&D Enquiries are Rising in 2026

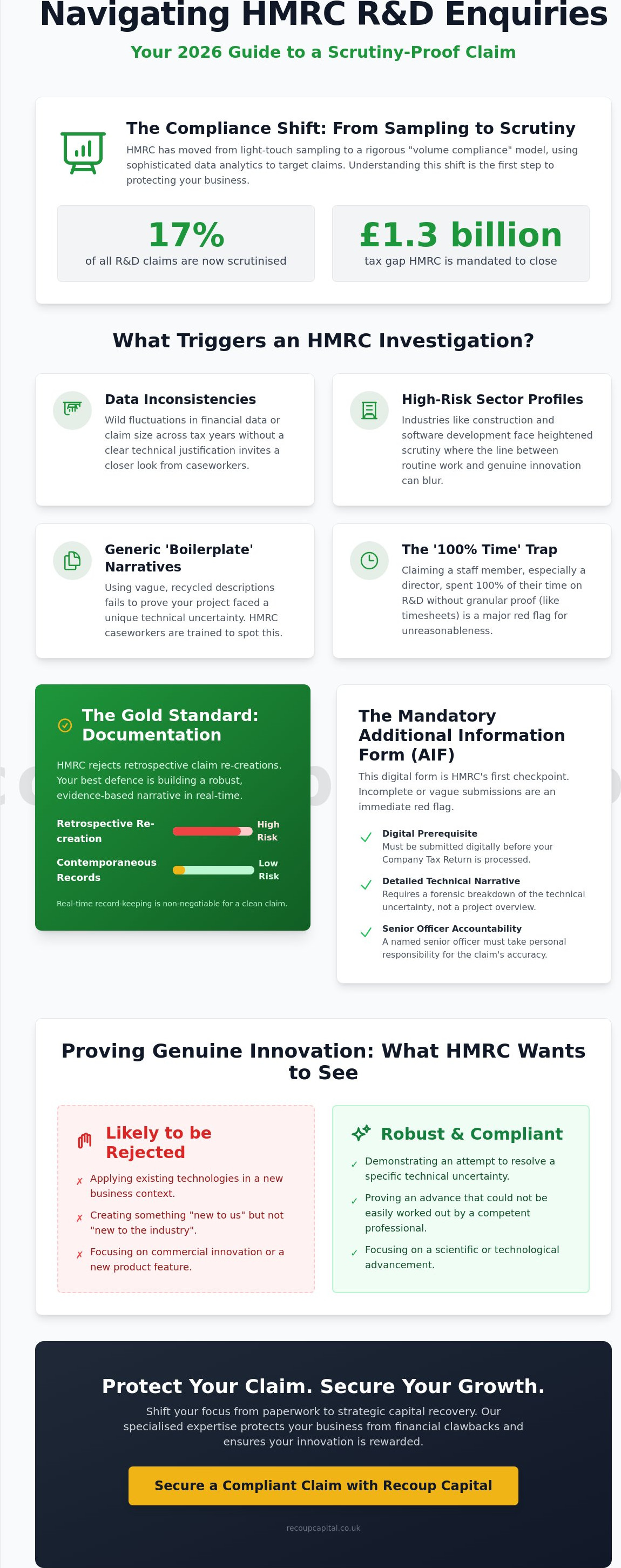

HMRC is on a mission. With a mandated goal to close a £1.3 billion tax gap, the department has transitioned from light-touch sampling to a rigorous volume-compliance model. Formally, an R&D enquiry is a compliance check conducted under the powers granted by the Finance Act 1998. Whilst these checks were once rare, the current landscape sees around 17 percent of all claims being scrutinised. This shift means that even legitimate, well-intentioned companies are being caught in the net amongst a wider crackdown on perceived error and fraud.

The UK tax incentive for R&D was originally designed to stimulate growth, but the current enforcement climate is more focused on policing the boundaries of that incentive. Understanding how to avoid an HMRC R&D enquiry begins with recognising that the rules of engagement have changed. HMRC now uses sophisticated data analytics to flag anomalies across thousands of submissions simultaneously. If your financial data appears inconsistent across different tax years, or if your claim lacks a forensic evidence trail, you are no longer just a random number; you are a target.

The Impact of the Additional Information Form (AIF)

The mandatory Additional Information Form has fundamentally altered the filing landscape. Since its introduction, every claim must be accompanied by this digital submission before the Company Tax Return is even processed. Incomplete forms or vague descriptions act as an immediate red flag for HMRC's automated risk-assessment tools. Crucially, the form requires a named senior officer within your organisation to take personal responsibility for the accuracy of the claim. This move ensures accountability, making it vital that your internal team fully understands the technical justifications behind every pound claimed.

HMRC's Evolving Definition of Innovation

Perhaps the most significant hurdle in 2026 is HMRC's increasingly narrow interpretation of what qualifies as R&D. There is a sharp distinction between commercial innovation; which might involve a new product for your customers; and a scientific or technological advancement. Many claims are rejected because they simply apply existing technologies in a new business context. To satisfy a caseworker, you must demonstrate that your project sought to resolve a specific technical uncertainty that could not be easily worked out by a competent professional in the field. For a deeper look at how automated systems are changing these reviews, see our guide on HMRC R&D Tax Claim Transparency and AI. Learning how to avoid an HMRC R&D enquiry requires moving beyond "new to us" and proving your work is "new to the industry."

Identifying the Red Flags: What Triggers an R&D Investigation?

HMRC's modern compliance systems don't just look for errors; they look for patterns. Whilst many directors assume enquiries are random, the reality is that specific "behavioural" triggers now alert HMRC's algorithms. These automated checks compare your submission against vast datasets to identify anomalies that suggest a lack of rigour. Understanding these triggers is the first step in learning how to avoid an HMRC R&D enquiry before you even hit submit. If your financial data fluctuates wildly between tax years without a clear technical explanation, you're essentially inviting a caseworker to look closer.

Sector-specific scrutiny is also at an all-time high in 2026. HMRC has identified industries like construction and software development as high-risk zones. In these fields, the line between standard commercial work and genuine innovation often blurs. If your technical narrative reads like a generic project overview rather than a forensic breakdown of a technical challenge, it will likely be flagged. Avoiding "boilerplate" language is essential. Caseworkers are trained to spot descriptions that have been recycled from industry textbooks or previous claims, as these fail to prove that your specific project faced a unique uncertainty.

Another common pitfall is the "100 percent trap." Claiming that a staff member, particularly a senior director, spent every single working hour on R&D is a massive red flag. Without granular proof or timesheets, HMRC will likely challenge the validity of the entire claim. If you're unsure how your current documentation stacks up, you can find more detail on the criteria in our guide on R&D tax credits explained.

Financial Anomalies and Benchmarking

HMRC now uses sophisticated benchmarking to compare your R&D spend against industry averages for companies of your size. If your costs are significantly higher than your peers, the system demands a justification. Round numbers are another avoidable risk. Submitting a claim for exactly £50,000 or £10,000 suggests a "best guess" rather than a calculated total. In 2026, subcontracted costs are receiving extra attention, especially regarding the strict rules on overseas expenditure. Every pound must be traceable to a specific activity that meets the HMRC's compliance approach standards.

The "Competent Professional" Test

A central pillar of any investigation is the "Competent Professional" test. HMRC wants to know who led the project and what their specific qualifications are. Failing to name a lead technical specialist; such as a senior engineer or lead developer; often triggers an enquiry. You must be able to prove that the technical problem you solved was not "readily deducible" by another professional in your field. If a solution was available in a public forum or a standard manual, it doesn't qualify as R&D. To learn how to avoid an HMRC R&D enquiry, you must document why your specific team's expertise was required to overcome a hurdle that stumped the wider industry.

The Gold Standard for Contemporaneous Documentation

Documentation isn't just a chore. It's your primary defence. Contemporaneous evidence refers to records created whilst the R&D work was actually happening. HMRC prioritises these over anything else. If you're trying to figure out how to avoid an HMRC R&D enquiry, you must move away from retrospective re-creations. Caseworkers are increasingly sceptical of narratives written months after the fact; they want to see the raw, unpolished proof of the journey. A claim built on memory is a claim built on sand.

Linking your financial expenditure directly to technical milestones is the key. It isn't enough to present a total figure for staff costs. You need to show that those costs were incurred specifically to overcome a defined hurdle. Interestingly, project failures are some of the best evidence you can provide. A project that failed to reach its commercial goal often provides the clearest proof of genuine technical uncertainty. It shows that the solution was not "readily deducible" and required a level of trial and error that qualifies for relief. Don't hide your mistakes; document them as proof of your innovation.

Essential Technical Records to Maintain

Your technical file should act as a diary of innovation. HMRC expects to see the evolution of your solution through project plans, blueprints, and iteration logs. Minutes of technical meetings are invaluable; they capture the moments when uncertainties were identified and discussed. Don't forget testing protocols. Results that show a series of failed attempts before a breakthrough demonstrate the very essence of the R&D process. These records prove that your team was operating at the edge of current knowledge.

Robust Financial Record Keeping

Accuracy in your accounts is vital. Timesheets are the backbone of a successful claim, but they must distinguish between R&D activities and routine business operations. For a thorough breakdown of what costs qualify, see our guide on R&D tax credits explained. Learning how to avoid an HMRC R&D enquiry involves maintaining a forensic trail for every pound spent. You should also keep:

- Detailed invoices for materials used specifically in the R&D process.

- A clear methodology for apportioning utility and overhead costs based on actual usage.

- Records of subcontractor agreements that clearly define the technical scope of work.

By building this forensic trail, you transform your claim from a simple request into an unassailable strategic asset. This proactive approach ensures that if HMRC does come knocking, you have the evidence ready to go.

A Proactive Checklist: How to Enquire-Proof Your Submission

Prevention is the most effective strategy. Before you file, you need a rigorous final check. Understanding how to avoid an HMRC R&D enquiry means looking at your submission through the lens of a sceptical caseworker. A proactive audit ensures that your narrative is watertight and your financial data is beyond reproach. Don't wait for a letter from HMRC to start digging through your records. By the time you submit, your "defence file" containing all supporting evidence should already be complete and ready for inspection.

A key part of this process is cross-referencing your Additional Information Form (AIF) with your CT600. If the figures on your digital submission don't match your tax return exactly; HMRC's automated systems will flag the claim for a manual review. This simple data consistency check is a frequent cause of avoidable delays. You must also perform a "competent professional" review of the technical descriptions. This involves having your lead technical specialist verify that the language used accurately reflects the technical challenges faced; rather than just the commercial goals of the project.

Reviewing the Technical Narrative

Your technical report must do more than list your achievements. It needs to provide a clear baseline. Does the report explicitly state the level of technology that existed before the project began? You must define your technological advancement in non-commercial terms. HMRC isn't interested in your market share; they want to know how you pushed the boundaries of science or technology. Ensure the specific uncertainties are described as problems that couldn't be solved easily by a competent professional using standard industry knowledge.

Pre-Submission Financial Integrity Checks

Financial accuracy is the foundation of a "clean" claim. In 2026, HMRC is particularly focused on ensuring that capital expenditure isn't incorrectly categorised as revenue R&D. Whilst both are important; they are treated differently for tax purposes. You must also verify that any grants or subsidies have been correctly accounted for; as these can significantly alter your claim's eligibility under the merged scheme or ERIS. Finally, check that your staff costs include only qualifying pension and NIC contributions; as including non-qualifying benefits is a common error that triggers investigations.

If you want to ensure your claim meets these high standards and is processed without delay; our team can assist you with claiming R&D tax credits effectively. Taking these steps now creates a layer of protection that lasts long after the credit has been paid into your account.

Partnering for Protection: The Recoup Capital Approach

Whilst your general accountant is vital for day-to-day compliance, the specialised nature of R&D requires a different level of technical depth. Generalists often lack the specific engineering or software expertise needed to challenge a caseworker's technical queries. Learning how to avoid an HMRC R&D enquiry is as much about who prepares your claim as it is about the data itself. We act as a protective guide through these complexities, ensuring that every narrative is backed by forensic evidence that satisfies the most rigorous standards of 2026.

Our approach is built on transparency and results. Recoup Capital operates on a success-based fee model, which means our interests are perfectly aligned with yours. We don't just aim for the largest possible claim; we aim for the most compliant one. By having chartered tax accountants manage all HMRC liaison, we provide a professional buffer that reduces the administrative burden on your team. This partnership transforms a potentially intimidating regulatory procedure into a streamlined opportunity for business growth.

Our Forensic Claim Methodology

We identify qualifying activities that generalists often overlook, particularly in complex sectors. Our process involves building a bulletproof technical and financial evidence trail from the ground up. This is especially critical in industries where innovation is woven into daily operations, such as Construction R&D Tax Relief. We don't rely on generic descriptions. Instead, we map every pound of expenditure to a specific technical milestone, ensuring your submission is robust enough to withstand any volume-compliance algorithm. This forensic level of detail is the most effective way to demonstrate technical uncertainty clearly.

Long-Term Collaboration and Enquiry Support

Our relationship doesn't end when the claim is submitted. We're committed to a long-term collaboration that includes full enquiry support. If HMRC does raise a query, we handle the defence on your behalf, using the evidence files we prepared before the filing. This proactive, partnership-oriented style ensures you can focus on your core business whilst we protect your interests. We choose to reframe your financial returns as strategic assets. These aren't just refunds; they're capital tools designed to fuel your next phase of innovation.

Choosing the right partner is the final step in mastering how to avoid an HMRC R&D enquiry. If you value a relationship-first approach that prioritises your bottom line without compromising on compliance, discover why claim with Recoup Capital to secure your business's future. We're here to ensure your innovation is rewarded, protected, and put to work.

Securing Your Innovation for the Long Term

The landscape of 2026 requires a fundamental shift in how you approach your tax incentives. By moving away from retrospective re-creations and embracing a forensic, real-time documentation strategy, you protect your business from unnecessary scrutiny. We've explored the importance of the "Technical Uncertainty" audit and the value of identifying specific behavioural triggers before they alert HMRC's algorithms. Mastering how to avoid an HMRC R&D enquiry isn't just about compliance; it's about transforming your returns into strategic assets that fuel future growth without the fear of financial clawbacks.

Our team of specialist chartered tax accountants is ready to act as your protective guide. With a proven track record in high-scrutiny sectors like construction, we ensure your claim is robust enough to withstand the most detailed reviews. We operate on success-based fees with no upfront costs, ensuring our interests remain perfectly aligned with your long-term success. It's time to claim with confidence and focus on what you do best: innovating for the future.

Speak to a Specialist about Protecting Your R&D Claim

Frequently Asked Questions

What is the most common reason HMRC opens an R&D enquiry?

The most frequent trigger is a technical narrative that remains too vague or fails to distinguish between routine commercial work and genuine innovation. HMRC's automated systems flag claims where financial data doesn't align perfectly with the CT600 or the Additional Information Form. If your submission lacks project-specific details or uses "boilerplate" language, it's often selected for a manual compliance check.

How far back can HMRC go when enquiring into R&D tax credit claims?

HMRC typically has a 12-month window from the statutory filing deadline to open an enquiry into a corporation tax return. However, this window can extend significantly if they suspect a deliberate understatement or a loss of tax. In cases of discovery assessments, the period can stretch to six years for careless errors or twenty years for deliberate non-compliance. Maintaining a robust long-term evidence trail is a vital part of knowing how to avoid an HMRC R&D enquiry.

Can I still claim R&D tax credits if my project was a technical failure?

You can absolutely claim for projects that didn't reach their commercial or technical goals; in fact, failures often provide the strongest proof of eligibility. A project that fails demonstrates that the solution wasn't "readily deducible" by a competent professional in your field. Documenting your failed iterations and the reasons why a specific approach didn't work provides the forensic evidence HMRC needs to verify genuine technical uncertainty.

What happens if HMRC disagrees with my definition of technical uncertainty?

HMRC will usually issue a formal "check of facts" letter requesting further clarification or specific evidence to support your technical claims. If they remain unconvinced after reviewing your response, they may seek to reduce the qualifying expenditure or reject the claim entirely. This is why having a specialist lead the technical dialogue is essential; they ensure your advancements are framed correctly within the specific legislative framework.

How long does a typical HMRC R&D enquiry take to resolve in 2026?

Most enquiries currently take between six and twelve months to reach a resolution, depending on the complexity of the technical questions involved. Whilst HMRC aims for efficiency, the back-and-forth nature of detailed compliance checks can extend the timeline significantly. Providing a comprehensive "defence file" at the very start of the process can help resolve these queries much faster than a reactive approach.

Does using an R&D specialist increase or decrease my chance of an enquiry?

Working with a reputable specialist significantly decreases the likelihood of an investigation by ensuring your claim meets the highest documentation standards. High-quality, well-structured submissions are far less likely to trigger HMRC's risk-based algorithms. It's a proactive step that demonstrates to HMRC that you've taken reasonable care in preparing your claim, which is a key factor in how to avoid an HMRC R&D enquiry.

What is the penalty if HMRC finds an error in my R&D claim?

Penalties are calculated as a percentage of the "potential lost revenue" and vary based on the behaviour that led to the error. For a careless inaccuracy, penalties generally range from 0 to 30 percent, whilst deliberate errors carry much higher charges that can exceed 70 percent. HMRC often reduces these penalties if you provide a full, unprompted disclosure and cooperate fully during the compliance check.

How much contemporaneous evidence is considered "enough" by HMRC?

There is no fixed page count, but your evidence must be sufficient to substantiate the technical journey and the costs incurred. HMRC looks for a logical mix of project plans, meeting minutes, and testing results that align with your financial records. The key is quality over quantity; every piece of evidence should serve to prove that a specific qualifying activity took place and involved technical uncertainty.