Agritech R&D Tax Credits UK: Unlocking Innovation in 2026

If you believe agritech R&D tax credits UK are reserved for scientists in white lab coats, you're likely leaving tens of thousands of pounds on the table. With the average SME claim in the agricultural sector reaching £42,373, the reality is that innovation happens in the field and the barn just as often as the laboratory. Whether you're developing new crop varieties or refining precision irrigation systems, your daily problem-solving could be a significant source of capital recovery.

It's understandable if the recent transition to the Merged R&D Scheme feels daunting. Between the strict six-month deadline for the Claim Notification Form and the increased focus on the Additional Information Form, the fear of HMRC enquiries is a genuine concern for many. You've worked hard to innovate; the last thing you want is a complex regulatory hurdle standing in the way of your progress.

This article promises to demystify the 2026 rules and show you exactly how to secure the tax relief you deserve. We'll explore the specific projects that qualify under current HMRC standards, explain the 20% credit rate for the Merged Scheme, and highlight the enhanced support available for R&D-intensive businesses. By the end, you'll have a clear roadmap to maximise your returns and transform that relief into a strategic asset for your future business growth.

Key Takeaways

- Learn how to identify hidden innovation within your farming operations by applying the core scientific and technological uncertainty tests.

- Understand the financial mechanics of the 2026 Merged Scheme and how the 20% credit rate can be reframed as a strategic asset for business growth.

- Discover the essential compliance steps, including the mandatory six-month deadline for the Claim Notification Form, to secure your agritech R&D tax credits UK claim.

- Gain insights into the forensic approach required to accurately distinguish your eligible R&D expenditure from standard commercial production costs.

- Explore how partnering with a sector specialist ensures your claim meets modern HMRC standards whilst maximising capital recovery for reinvestment.

What are Agritech R&D Tax Credits in the UK?

Agritech R&D tax credits UK are a powerful corporation tax incentive designed to reward companies that invest in science or technology to solve agricultural challenges. This government-backed initiative provides a mechanism for businesses to recover a portion of their investment in innovation, effectively reducing the financial risk of experimentation. The UK's R&D tax credit scheme has undergone significant reform to streamline the process, yet the agricultural sector remains one of the most under-utilised industries for this relief. Many farmers and agritech developers don't realise that their daily problem-solving qualifies as research and development.

HMRC statistics from 2022 showed an 11% reduction in R&D expenditure within the agriculture, forestry, and fishing sector. This trend is concerning because the sector is actually a hotbed of innovation. We need to shift the narrative from "white coats" to "wellies." Your laboratory isn't a sterile room with petri dishes; it's the field, the greenhouse, and the livestock pen. If you're attempting to improve crop yields through novel soil treatments or developing bespoke sensors for precision farming, you're conducting field-based science. These activities are essential for the UK's transition toward a high-efficiency, sustainable agricultural future.

The Economic Impact of Innovation in 2026

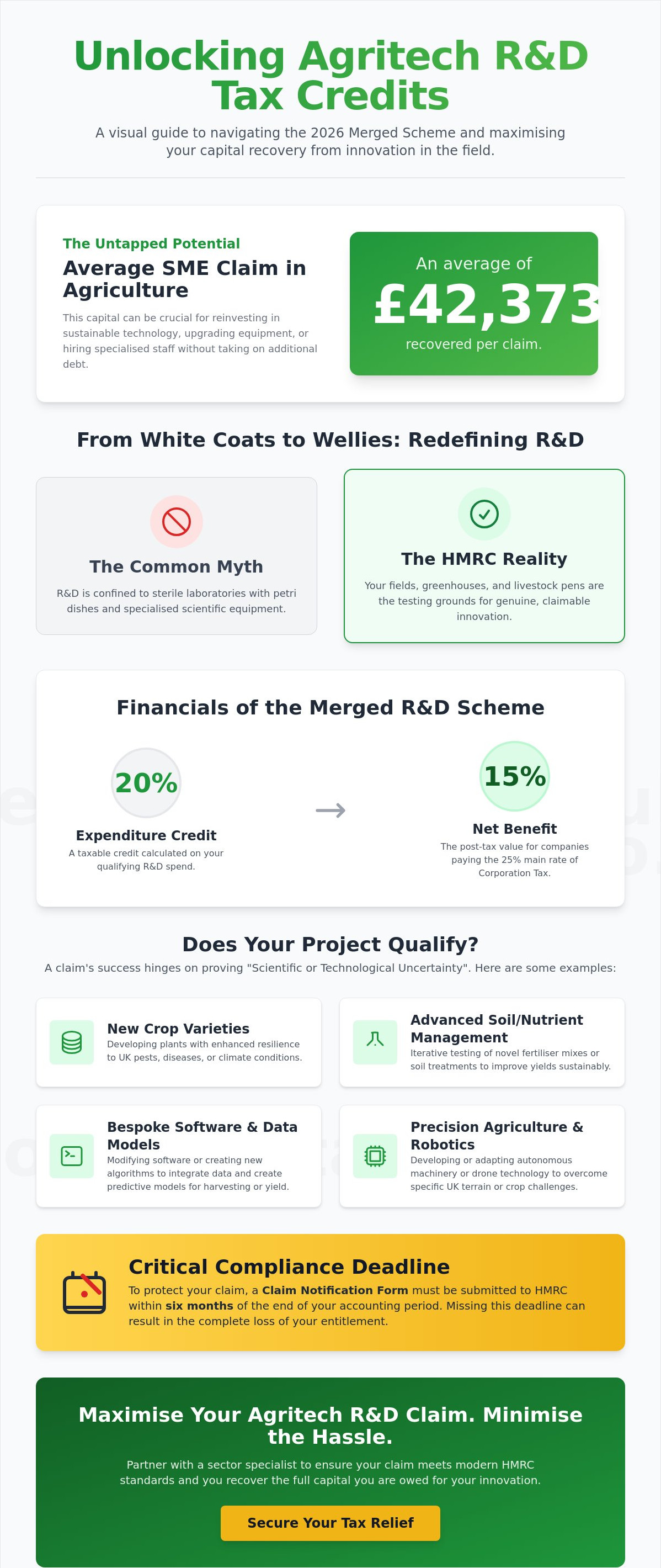

By 2026, these credits have evolved into a strategic asset for business scaling. The UK government previously committed £270 million to the agritech sector through the Farming Innovation Programme, and tax relief acts as a vital secondary pillar of support. With the 2050 Net Zero agricultural targets looming, the pressure to innovate has never been higher. Reclaiming capital through R&D allows you to reinvest in the sustainable technology required to remain competitive. For many, the average SME claim of £42,373 provides the necessary liquidity to upgrade equipment or hire specialised staff without taking on additional debt.

Who is Eligible to Claim?

To qualify for this incentive, your business must be a UK limited company liable for Corporation Tax. Under the Merged R&D Scheme, which applies to accounting periods starting on or after 1 April 2024, the rules for SMEs and large enterprises have been unified. This scheme offers a taxable expenditure credit of 20%, which results in a net benefit of 15% for companies paying the main rate of Corporation Tax. It's a common misconception that receiving a grant disqualifies you from claiming. Whilst grants can complicate the process, you can often still secure significant relief. It's essential to understand how R&D tax credits work alongside other funding to ensure your claim is fully compliant and maximised.

Qualifying Agritech Projects: Identifying Hidden R&D

Identifying qualifying projects for agritech R&D tax credits UK requires looking beyond the simple purchase of new equipment. The core of every successful claim is the "Scientific or Technological Uncertainty" test. This means you must be attempting to achieve a result that isn't readily deducible by a competent professional in the field. If you're simply using off-the-shelf software to track yields, you aren't innovating. However, if you're modifying that software to integrate disparate data sets from legacy machinery to create a predictive harvest model, you've likely crossed the threshold into R&D. Customisation becomes innovation when the solution requires a bespoke technological leap that didn't previously exist.

Broadening the scope of innovation in the UK agritech sector involves recognising biological advancements that often go unclaimed. Developing crop varieties with enhanced resilience to specific UK pests or experimenting with genetic improvements to increase protein content in forage crops are classic examples of qualifying science. These projects often involve iterative testing and high failure rates; these uncertainties are the hallmarks of eligible activity. You don't need a lab to be a scientist. The trial plots on your farm where you test new fertiliser ratios or drought-resistant seeds are your testing grounds.

Precision Agriculture and Robotics

Precision agriculture isn't just about owning a drone. It involves overcoming technological bottlenecks, such as developing autonomous machinery capable of navigating complex UK terrains where standard GPS fails. Integrating multi-spectral imaging with AI for real-time nutrient application requires bespoke software development and complex sensor integration. When you're solving IoT connectivity issues in remote "dead zones" to ensure real-time data flow, you're actively engaging in qualifying R&D.

Sustainability and Regenerative Tech

Meeting the UK's Net Zero targets requires radical innovation in soil health and waste reduction. Qualifying projects include developing novel carbon sequestration monitoring techniques or creating low-impact biological pest controls that replace traditional chemicals. If you're engineering circular economy systems to transform food waste into high-value fertilisers through new processing methods, your work likely qualifies. These sustainability-focused breakthroughs are vital drivers for modern agritech R&D tax credits UK claims.

If you're unsure whether your current project meets these criteria, you can explore our claiming guide to see how we help identify these hidden opportunities.

Navigating the Merged R&D Scheme in 2026

The landscape for agritech R&D tax credits UK changed fundamentally on 1 April 2024 with the introduction of the Merged Scheme. This legislative shift replaced the previous dual-track system with a single, unified framework. HMRC's goal was to simplify the process; however, the transition requires a more rigorous approach to documentation. Whether you're a precision-farming startup or an established machinery manufacturer, you're now likely operating under this centralised expenditure credit system. It's vital to follow the official government R&D guidance to ensure your claim aligns with these modern standards.

Success in 2026 depends on understanding how your specific financial position dictates your return. The Merged Scheme provides a taxable credit of 20% on qualifying expenditure. For businesses paying the main rate of Corporation Tax at 25%, this results in a net benefit of 15%. Whilst this is a reduction from the old SME scheme rates, the focus has shifted toward rewarding high-quality, evidence-backed innovation. If your company is loss-making, the credit is subject to a notional tax rate of 19%, leaving you with a net cash benefit of 16.2%.

Understanding the New Rates

For agritech startups where R&D is the primary focus, the Enhanced R&D Intensive Support (ERIS) remains a critical lifeline. If your qualifying R&D expenditure accounts for at least 30% of your total business spend, you may qualify for a higher rate of relief. ERIS offers an additional 86% deduction on top of the standard 100% deduction; it also allows for a payable tax credit of 14.5% for surrenderable losses. This can provide a net benefit of approximately 27%, making it an essential tool for scaling capital-intensive biological or robotic projects. Additionally, if your innovation results in a patent, the Patent Box can further reduce your effective tax rate on profits derived from that IP.

Compliance and the Additional Information Form (AIF)

The most significant hurdle in the current regime is the mandatory Additional Information Form (AIF). This digital submission must be filed before your Company Tax Return. It requires a detailed breakdown of costs and a technical narrative that links every pound spent to a specific technological uncertainty. You can't rely on generic accounting descriptions; you need technical input that speaks HMRC's language. Missing the Claim Notification Form (CNF) deadline, which is just six months after your accounting period ends, can invalidate your entire claim for agritech R&D tax credits UK. You can learn more about the R&D claim process to ensure your internal workflows meet these strict new deadlines.

Preparing a Compliant Agritech Claim

Securing agritech R&D tax credits UK in 2026 requires more than just a collection of invoices and receipts. HMRC now expects a forensic approach to claim preparation. This means you must establish a robust methodology that clearly separates your standard commercial production from your innovative activities. In a farm environment, where research often happens alongside day-to-day operations, this distinction is vital. You need to identify the exact moment a project moves from routine farming into a phase of technological experimentation. Documentation must be contemporaneous; waiting until the end of the year to reconstruct your R&D narrative is a significant risk.

One of the strongest indicators of a genuine claim is documented failure. If your new irrigation algorithm worked perfectly on the first attempt, HMRC might argue the solution was professionally obvious. True innovation involves trial, error, and the resolution of technical uncertainties. Keeping records of "unsuccessful" R&D projects isn't just good practice; it's a key indicator that you're pushing the boundaries of current technology. These failures provide the evidence needed for a technical narrative that can withstand the scrutiny of an HMRC enquiry.

Qualifying Expenditure Categories

Identifying what you can claim is as important as identifying why you're claiming. Staff costs often form the bulk of a claim, but you must accurately apportion time. If a farm manager spends 30% of their month troubleshooting a bespoke autonomous tractor system, only that 30% of their salary, NIC, and pension contributions is eligible. Consumables also qualify if they're "transformed" or consumed during the R&D process. This includes fuel used specifically for testing new machinery or water and nutrients used in a controlled vertical farming experiment.

Subcontracted R&D remains a complex area under the 2026 Merged Scheme rules. Whilst you can generally claim 65% of relevant subcontractor costs, you must navigate the restrictions on overseas expenditure that began for periods starting after 1 April 2024. Your technical specialists must be UK-based unless specific, narrow exceptions apply. Ensuring these costs are correctly categorised is the difference between a successful return and a rejected filing.

Avoiding Common Pitfalls and Enquiries

HMRC is increasingly vigilant regarding "routine" agricultural work being mislabelled as R&D. Simply implementing a new software package you bought off-the-shelf won't qualify. You must demonstrate how you've modified or integrated technology to solve a specific uncertainty. If you're unsure where the line is drawn, reviewing Common R&D tax credit FAQs can help clarify the distinction between standard business improvements and qualifying innovation. Specialist review is no longer a luxury; it's a necessity to ensure your documentation is "HMRC-ready" from the outset.

If you want to ensure your innovation is fully protected and your recovery is maximised, you can start with a professional HMRC-ready claim assessment today.

Why Partner with Recoup Capital for Agritech R&D?

Choosing a partner to handle your agritech R&D tax credits UK is a decision that directly impacts your long-term innovation strategy. Many generalist accountants overlook the technical nuances of agricultural science, which often leads to significant capital being left on the table. We bridge the gap between complex tax legislation and the practical realities of the field. Our approach isn't about merely processing paperwork; it's about building a relationship-first partnership that protects your interests whilst maximising your recovery. We act as your protective guide through the regulatory landscape, ensuring your claims are robust, compliant, and reflective of your true innovative effort.

We operate on a success-based fee structure, which ensures our goals are perfectly aligned with your capital recovery. There is no aggressive sales pressure here. Instead, we prefer to demonstrate our value through the results we achieve for our clients. By transforming complex regulatory procedures into approachable opportunities, we help you focus on what you do best: innovating the future of British agriculture. From the initial technical discovery to the final HMRC liaison, we provide end-to-end support that simplifies the path to reinvestment.

Our Proven Methodology

Our specialists are trained to identify "hidden" R&D that generalists often miss. Whether it's the specific calibration of a drone for variable rate application or the unique challenges of developing regenerative soil treatments, we understand the science. The Recoup Capital "Technical Audit" is a cornerstone of our process. We don't just write a narrative; we stress-test it against modern HMRC standards to ensure it stands up to scrutiny. If you're wondering why choose Recoup Capital?, the answer lies in our ability to translate your field-based science into the precise technical language required by the Merged Scheme.

Strategic Capital Recovery

We reframe your tax credit as a strategic asset rather than a simple refund. In the capital-intensive world of agritech, these funds act as a vital tool for acquiring new assets, hiring technical specialists, or funding your next breakthrough project. This perspective shifts the narrative from mere tax compliance to a proactive business growth strategy. For a broader look at selecting the right partner for your needs, you can explore our guide on R&D Tax Credit Specialists UK.

Our commitment is to your future, not just your current filing. We look for long-term collaboration opportunities where we can help you navigate the evolving agritech R&D tax credits UK landscape year after year. Secure your no-obligation agritech R&D assessment today and discover the true value of your agricultural innovation.

Transforming Your Agricultural Innovation into Strategic Capital

The landscape of 2026 demands a fundamental shift in how we view the "field-based laboratory." You've seen how identifying hidden innovation and navigating the Merged Scheme's 20% credit rate can unlock significant liquidity for your business. By moving beyond routine operations and embracing a forensic approach to compliance, your daily problem-solving becomes a powerful driver for growth. It's time to stop leaving eligible capital in the soil and start reframing your tax relief as a strategic asset.

At Recoup Capital, our team of chartered tax accountants specialises in the unique technical nuances of the agricultural sector. We act as protective guides with a proven track record of defending submissions against HMRC enquiries; our success-based fee structure means there are no upfront costs. This ensures our goals are entirely aligned with your capital recovery and long-term innovation. If you're ready to see what your hard work is worth, book your free agritech R&D assessment with Recoup Capital today to secure the agritech R&D tax credits UK your business deserves.

The path to a more sustainable, high-efficiency future starts with the capital you've already earned through your ingenuity. We look forward to helping you claim it.

Frequently Asked Questions

Can farm businesses claim R&D tax credits for improving soil health?

Yes, farm businesses can claim if the project involves overcoming a specific scientific or technological uncertainty. If you're developing bespoke carbon sequestration methods or novel microbial treatments that haven't been proven in your specific environment, the work likely qualifies. Simply following standard soil management practices or using off-the-shelf fertilisers doesn't meet the criteria for innovation.

How much can an agritech company expect to receive back from HMRC?

Profit-making companies under the Merged Scheme typically receive a net benefit of 15% of their qualifying expenditure. For loss-making, R&D-intensive SMEs, the return can reach approximately 27% through the Enhanced R&D Intensive Support (ERIS) scheme. According to 2022 HMRC statistics, the average claim for an SME in the agricultural sector was £42,373, though your specific return depends on your total qualifying spend.

Is the R&D tax credit scheme still available for SMEs in 2026?

Yes, the scheme remains fully available for SMEs in 2026, though most now claim under the Merged R&D Scheme. This unified system replaced the old dual-track regime for accounting periods starting on or after 1 April 2024. SMEs that spend at least 30% of their total expenditure on R&D can still access higher rates of relief through the ERIS framework.

Does developing a new type of organic pesticide qualify as R&D?

Formulating a new organic pesticide is a classic example of a project that qualifies for agritech R&D tax credits UK. The process requires significant biological experimentation and iterative testing to prove efficacy whilst ensuring environmental safety. Because the outcome of such complex chemical or biological formulations isn't certain at the outset, the staff time and materials used during development are eligible costs.

What happens if my agritech R&D project is unsuccessful?

You can still claim for projects that fail to reach their technical goals. In fact, HMRC often views technical failure as strong evidence that a genuine "uncertainty" existed, which is a core requirement for any claim. As long as you can document the scientific challenges you tried to overcome, the expenditure incurred during the attempt remains fully eligible for tax relief.

How far back can I claim agritech R&D tax credits in the UK?

You can generally claim for the two most recent completed accounting periods. The statutory deadline is exactly two years after the end of the accounting period in which the R&D expenditure was incurred. It's essential to act quickly, as missing this window means you'll permanently lose the opportunity to recover capital from those earlier years of innovation.

Can I claim R&D tax credits if my project received a government grant?

Yes, you can still claim R&D tax relief even if you've received a grant. Under the Merged Scheme rules, the presence of a grant doesn't automatically disqualify you or force you into a lower rate of relief as it sometimes did under the old SME scheme. However, the way your grant interacts with your R&D expenditure must be carefully documented to ensure you aren't double-claiming for the same costs.

What is the "Additional Information Form" and why is it mandatory?

The Additional Information Form (AIF) is a compulsory digital submission that must be filed before you submit your Company Tax Return. HMRC introduced this to improve transparency and reduce fraudulent claims by requiring a detailed technical narrative for every project. It forces companies to link their costs directly to specific technological uncertainties, making it a vital component of any compliant agritech R&D tax credits UK submission.