Research and Development Tax Checklist: A Guide for UK Limited Companies in 2026

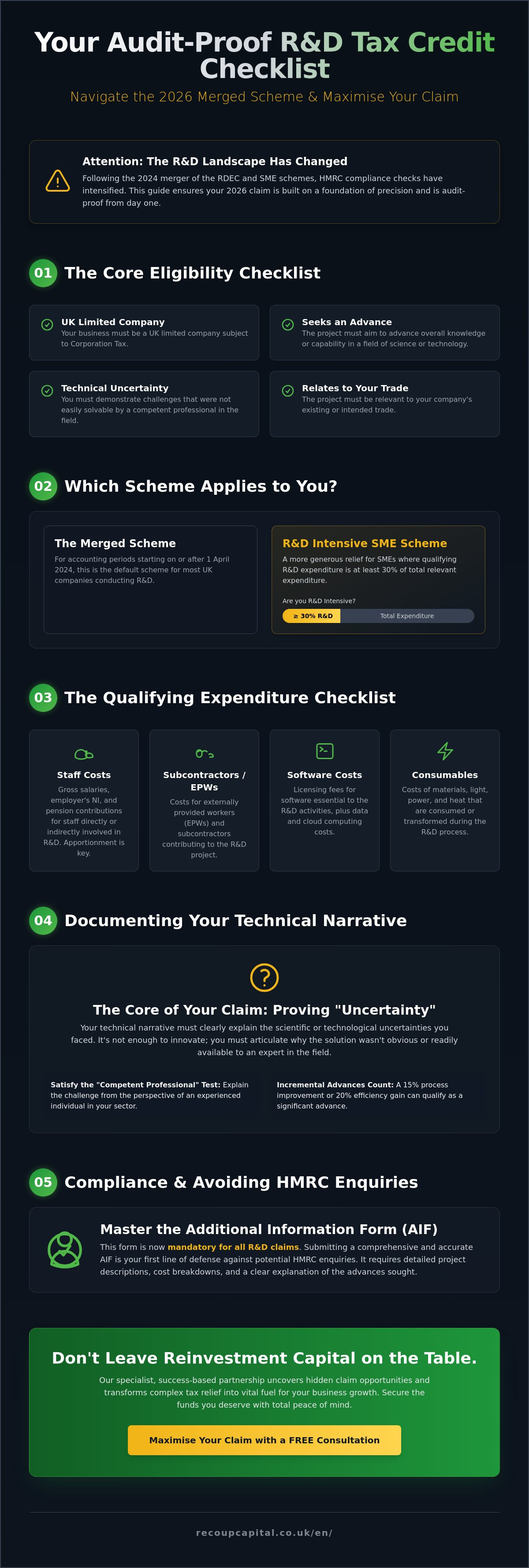

Did you know that since the 2024 merger of the RDEC and SME schemes, HMRC compliance checks have intensified, with official data showing a significant rise in detailed enquiries for research development tax claims? It is no longer enough to simply innovate; you must prove it with surgical precision. If you feel overwhelmed by the technical documentation or the complexity of the unified scheme, you are certainly not alone in that frustration.

We understand that your priority is driving your business forward, not getting lost in the weeds of tax legislation. This guide provides a comprehensive, step-by-step checklist designed to transform a daunting process into a clear "yes/no" framework for eligibility. You will learn how to identify qualifying costs, calculate your total expenditure accurately, and ensure your 2026 claim is entirely audit-proof from day one. By following this structured approach, you can maximise your claim value and secure vital money for reinvestment. We will outline everything from the initial project assessment to the final submission requirements, giving you the confidence to claim what your business deserves whilst maintaining total peace of mind.

Key Takeaways

- Identify whether your business qualifies for the Merged Scheme or the R&D Intensive SME relief to ensure you access the most beneficial rates for the 2026 tax year.

- Learn how to accurately categorise and apportion qualifying costs to maximise your research development tax claim whilst maintaining the transparency required by HMRC.

- Master the technical narrative by documenting "uncertainty" in a way that satisfies inspectors and highlights the genuine innovation within your projects.

- Stay ahead of the latest compliance standards by understanding the mandatory Additional Information Form (AIF) requirements to protect your company from potential enquiries.

- Discover how a specialist, success-based partnership can uncover hidden claim opportunities and transform tax relief into vital capital for future business reinvestment.

Understanding Research Development Tax: Is Your Business Eligible?

Is your business leaving capital on the table? Many UK directors view tax as a one-way street, yet research development tax relief serves as a powerful mechanism to reclaim costs and fuel future growth. It isn't a traditional grant or a handout. Instead, it's a statutory Corporation Tax relief that rewards UK limited companies for investing in innovation. At Recoup Capital, we view these credits as "money for reinvestment," providing the liquidity you need to hire new talent, upgrade infrastructure, or accelerate your next project.

The landscape for claims has evolved significantly. For accounting periods beginning on or after 1 April 2024, most companies now operate under the Merged Scheme. However, if your business is an R&D Intensive SME, meaning your qualifying R&D expenditure constitutes at least 30% of your total relevant expenditure, you may access a higher rate of relief. This distinction is vital for your 2026 tax planning, as the UK R&D tax incentive remains one of the most competitive in the world for high-growth firms.

HMRC assesses your claim through the "competent professional" test. They don't expect a tax inspector to understand the nuances of your software architecture or chemical formulations. Instead, they look for a statement from an experienced individual in your sector who can explain why a technical challenge was difficult and why the solution wasn't common knowledge. If a skilled professional in your industry couldn't easily solve the problem, you likely have a claim.

The Core Eligibility Checklist

- Your business must be a UK limited company liable for Corporation Tax.

- The project must seek an advance in overall knowledge or capability in a field of science or technology.

- You must be able to demonstrate that you faced technical uncertainties that were not readily resolvable by a professional in the field.

- The project must relate to your company's trade, either existing or intended.

For a more detailed breakdown of these requirements, you can find our R&D tax credits explained guide which simplifies the legislative jargon into actionable insights.

Identifying "Advances" in Your Sector

An "advance" doesn't always mean a "Eureka!" moment that changes the world. It often involves incremental technical change that appreciably improves an existing system. You might be creating a brand-new product from scratch, but you could also be modifying a manufacturing process to reduce waste by 15% or developing a software algorithm that handles data 20% more efficiently than current industry standards. If you're pursuing scientific knowledge that doesn't currently exist in the public domain, you're likely breaking new ground. We act as your expert friend, helping you identify these hidden pockets of innovation whilst ensuring your claim is robust and compliant. Today’s adviser, tomorrow’s partner; we're here to help your business thrive through a FREE 15 minute consultation.

The Qualifying Expenditure Checklist: What Can You Claim?

Identifying every eligible penny is what turns a modest claim into a source of substantial reinvestment. Under the merged scheme active in 2026, the research development tax landscape requires meticulous record-keeping. You can't just guess figures; you must apportion time and costs with surgical precision to satisfy HMRC R&D relief guidance. This ensures the credit acts as a genuine engine for growth rather than a compliance headache. Every pound identified is a pound that can be cycled back into your next breakthrough.

Staffing and Consumable Costs

Staff costs often form the largest portion of a claim. You should include gross salaries, employer Class 1 National Insurance, and pension contributions for those directly involved in the innovation process. Precision is vital here. If a lead developer spends 75% of their month on a prototype and 25% on routine maintenance, you must reflect that 75% split accurately in your figures. You can also include "indirectly active" staff. This doesn't mean the entire HR department, but it does cover technical supervisors or maintenance teams who keep R&D equipment operational. Consumables are equally important. You can claim for materials, water, fuel, and power that are either transformed or used up whilst you're resolving a technical uncertainty.

Software, Data, and Cloud Computing

By 2026, digital infrastructure has become a cornerstone of British innovation. The rules now clearly allow for the inclusion of cloud computing and data costs that are essential to the R&D process. This includes:

- Licence fees for specialised software used for CAD, coding, or simulation.

- Cloud storage costs required for housing large R&D datasets.

- Computing power used for running complex algorithms or digital stress tests.

It's important to filter these costs carefully. You must exclude software used for general business administration, such as accounting platforms or standard email services. Only the portion of the licence or usage fee directly attributable to the R&D project qualifies for relief.

Subcontractors and Externally Provided Workers (EPWs)

The merged scheme has refined how we handle external help. Generally, you can claim 65% of the relevant costs paid to subcontractors or EPWs. The distinction between "contracted out" R&D and general services is a common area of HMRC scrutiny. To qualify, you must show that the R&D was intended from the start of the contract. If you've hired a specialist to solve a specific technical problem that your internal team couldn't crack, that's a strong indicator of eligibility. Understanding Why claim R&D tax credits? helps you view these external costs as strategic investments rather than just overheads. If you're wondering how these rules apply to your specific vendors, you might want to see how we categorise expenditure to maximise your returns safely.

The Technical Narrative Checklist: Documenting the "Uncertainty"

The technical narrative is the most vital component of your HMRC submission. It's the heart of the claim. While the spreadsheets provide the "how much," the narrative provides the "why." HMRC inspectors aren't looking for a marketing brochure or a list of successful product launches. They're searching for the technical struggle. Without a clear explanation of the scientific or technological uncertainty you faced, your claim for research development tax relief will likely be rejected.

HMRC loves failures. A project that ends in a dead end is often the strongest evidence of a genuine R&D attempt. If the outcome was certain from the start, it wasn't R&D. You must move away from generic "innovation" language. Phrases like "cutting-edge" or "revolutionary" carry no weight with a technical inspector. Instead, focus on technical specificity. Describe the exact physics, coding limitations, or material constraints that blocked your path. If your team spent three months trying to integrate two incompatible APIs and failed, document that failure. It proves the solution wasn't "readily deducible" by a competent professional.

Defining the Baseline and the Advance

You must establish the "state of the art" before your project began. This isn't just your company's internal baseline; it's the industry standard. If you're improving a manufacturing process, don't just say it's "faster." Quantify the advance. State that you aimed to reduce thermal loss by 25% or increase throughput by 15 units per hour using a specific novel methodology. This clarity helps explain the mechanics of R&D tax credits to an inspector who may not be an expert in your specific niche.

Evidence and Record-Keeping Checklist

In 2026, HMRC's scrutiny of record-keeping is at an all-time high. Estimates and retrospective guesses are no longer sufficient for a robust research development tax claim. You need a contemporaneous paper trail that proves the work happened when you say it did. A lack of documentation is the quickest way to trigger an enquiry. Ensure your internal systems capture the following:

- Version control logs: GitHub or Jira history that shows iterative trials, bug fixes, and technical pivots.

- Technical whiteboard sessions: Photos of diagrams or meeting minutes that detail the specific technical roadblocks discussed.

- Time-allocation models: Robust timesheets or project management data that link specific staff hours to R&D activities rather than general commercial work.

- Prototype iterations: Evidence of physical or digital models that were tested and subsequently refined or discarded.

Think of yourself as a protective guide for the HMRC inspector. If you make their job easy by providing clear, evidence-backed technical details, your claim is much more likely to move through the system seamlessly. We view these narratives as a strategic business tool rather than a mere compliance chore.

The 2026 Compliance Checklist: Avoiding HMRC Enquiries

For many UK directors, the fear of an HMRC enquiry is the primary reason they hesitate to file a claim. This anxiety is understandable given that HMRC expanded its "Volume Compliance" team significantly between 2023 and 2025. However, an enquiry isn't a random occurrence. It's usually the result of a specific "red flag" or a lack of transparency in the digital filing. Since the mandatory introduction of the Additional Information Form (AIF) in August 2023, the process has become more structured, leaving less room for ambiguity.

HMRC now uses sophisticated risk-profiling to scan submissions. Understanding the intersection of HMRC R&D tax claim transparency and AI is vital for any business looking to secure their funding without a fight. If your data doesn't align across your AIF and your CT600 corporation tax return, the system will likely flag your company for a manual review.

HMRC Transparency Standards

Transparency is your strongest defence. You must name a responsible senior officer within your business for every claim. This ensures internal accountability. Your research development tax submission must also provide a forensic breakdown of costs. Don't just list total figures; specify software licences, consumable items, and individual staff contributions. Technical descriptions should focus on the "technological uncertainty" rather than the commercial success of the product. Avoid "marketing speak" that highlights how great the product is. HMRC only cares about why it was difficult to build.

Common Red Flags to Audit

HMRC's software looks for patterns that suggest low-effort or fraudulent claims. A common mistake is submitting "copy-paste" narratives where the technical hurdles are identical to the previous period. If your innovation hasn't evolved, your eligibility has likely ended. You should also avoid round numbers like £10,000 or £25,000 in your costings. These suggest guesswork rather than precise record-keeping. Finally, ensure your project isn't "business as usual". If a competent professional in your field could have solved the problem using standard knowledge, it won't qualify as R&D.

Before you finalise your 2026 filing, perform a final cross-reference. Ensure the figures in your technical report match the research development tax relief boxes on your CT600 exactly. Small discrepancies often trigger long, costly enquiries that could have been avoided with a simple five-minute check.

Want to ensure your documentation meets the latest 2026 standards? Learn more about our enquiry-proof process.

Maximising Your Claim with R&D Tax Credit Specialists

General accountants focus on the broad strokes of your business. They're vital for annual filings, but they often lack the technical depth required to identify every eligible activity within research development tax claims. In 2026, HMRC's scrutiny of technical justifications has reached a peak. Missing a subtle innovation in your software architecture or a bespoke engineering solution could mean leaving thousands of pounds on the table. Specialists bridge this gap by translating complex technical work into the specific language HMRC requires.

Specialist vs. Generalist: The Comparison

Specialists bring deep sector knowledge in fields like construction, food technology, and high-end engineering. This expertise allows for a robust defence during HMRC enquiries, as specialists speak the same technical language as your project leads. By choosing a specialist, you're ensuring that the narrative of your claim is as strong as the financial data supporting it. You can learn more about claiming R&D tax credits with Recoup to see how this technical focus benefits your bottom line.

Recoup Capital operates on a success-based fee model. This removes the financial barrier to entry. If your claim isn't successful, you don't pay a fee. It's a risk-free way to explore your eligibility without impacting your cash flow. We view ourselves as "Today’s adviser, tomorrow’s partner." Our goal isn't just a one-off win; it's about identifying money for reinvestment that fuels your company's future growth. We want to help your business thrive through consistent, accurate claims year after year.

Your 15-Minute Consultation Checklist

Moving from a checklist to a professional assessment is the most effective way to secure your funding. You don't need a full report ready, but having a few details to hand makes the process seamless. Prepare these points before we speak:

- A brief summary of your two or three most technical projects from the last year.

- A rough estimate of your annual staff spend and any subcontractor costs.

- Any previous feedback regarding research development tax from HMRC or your current accountant.

We've facilitated significant capital for our clients by digging deeper than the average firm. We don't believe in aggressive sales pitches. Instead, we demonstrate value through results and transparency. Ready to see what your innovation is worth? Book your FREE 15-minute consultation today and take the first step toward securing the capital your business deserves.

Turn Your 2026 Innovation into Strategic Capital

Navigating the 2026 landscape for research development tax requires more than just a list of costs. It demands a robust technical narrative and meticulous compliance to meet HMRC’s rigorous standards. By accurately identifying qualifying expenditure and documenting every technical uncertainty, you transform a complex tax process into a strategic tool for reinvestment. Don't let valuable capital sit unclaimed when it could be fuelling your next breakthrough. Our approach ensures that your claims are both maximised and protected against potential enquiries.

Recoup Capital operates from offices in London and Manchester, serving the entire UK with a dedicated team of Chartered tax accountants and technical specialists. We work on a success-based fee structure, which means our interests are perfectly aligned with your financial recovery. We've built our reputation on demonstrating value through results, helping businesses thrive without the pressure of a traditional sales pitch. It’s about more than just a refund; it’s about building a partnership that supports your long-term growth.

Ready to see what your innovation is worth? Book a FREE 15-minute consultation with our R&D specialists today. Let’s turn your technical challenges into your company's greatest financial strength.

Frequently Asked Questions

Can I claim research development tax if my project failed?

Yes, you can claim for failed projects. HMRC focuses on the attempt to resolve scientific or technological uncertainty rather than the final commercial outcome. If your team spent 450 hours trying to develop a new carbon-neutral polymer but couldn't overcome structural instability, those costs remain eligible. Failed innovation is still a valid form of research development tax activity because it proves the solution wasn't readily deducible by a competent professional.

How far back can I go when claiming R&D tax credits in 2026?

You can typically claim for the two previous accounting periods. For a company with a year-end of 31 December 2026, you have until 31 December 2028 to submit or amend a claim for the period ending in 2026. This rolling two-year window ensures you don't miss out on money for reinvestment from work completed in 2024 or 2025. It's a vital timeline to monitor to protect your business cash flow.

What is the difference between the merged scheme and the SME intensive scheme?

The merged scheme, introduced in April 2024, unified the previous RDEC and SME systems into a single expenditure credit model. However, the SME intensive scheme remains for businesses where R&D expenditure constitutes at least 30% of total spend. Intensive SMEs can claim a higher payable credit of 14.5% instead of the standard 13% net benefit under the merged scheme. This distinction provides a significant boost for high-innovation startups and specialist labs.

Does my business need to be profitable to claim R&D tax relief?

No, your business doesn't need to be profitable to benefit from research development tax relief. Loss-making UK limited companies can choose to surrender their R&D losses in exchange for a payable cash credit from HMRC. This provides immediate liquidity for reinvestment into future projects. For many of our partners, this cash injection is more valuable than a reduction in corporation tax because it fuels growth during the early, pre-revenue stages.

How long does it take for HMRC to process an R&D tax credit claim?

HMRC currently aims to process 80% of R&D tax credit claims within 40 days of receipt. While most payments arrive within this six-week window, complex filings or those selected for additional checks can take longer. We recommend submitting your claim as early as possible after your year-end to ensure a seamless transition of funds into your business bank account. Our goal is always to make this recovery process as efficient and predictable as possible.

Can I claim for R&D if the project was funded by a grant?

Yes, you can still claim if you've received a grant, though it may change how your claim is structured. Under the rules applicable in 2026, most grant-funded projects fall under the merged scheme rather than the SME intensive scheme. This prevents "double dipping" into state aid while ensuring you receive a fair credit for your independent innovation efforts. It's a complex area where expert guidance ensures you stay compliant while maximising your return.

What happens if HMRC opens an enquiry into my R&D claim?

If HMRC opens an enquiry, they'll request detailed technical reports and financial breakdowns to verify your eligibility. This isn't a cause for alarm, but it does require a proactive and transparent response within the 30-day window usually provided. We act as your protective guide during this process, handling the technical dialogue and providing the evidence needed to satisfy the inspector. Our track record shows that robust documentation is the best defence against such scrutiny.

Is "innovation" the same as "R&D" in the eyes of HMRC?

HMRC applies a much stricter definition to R&D than the general business term "innovation." While innovation might include a new marketing strategy or aesthetic design, R&D for tax purposes requires a specific advance in science or technology. You must be seeking to overcome a technical uncertainty that isn't easily solved by a professional in your field. Understanding this distinction is the first step in our free 15 minute consultation to determine your true claim potential.