R&D Tax Credits for Subsidised Projects: A 2026 UK Compliance Guide

If you've secured a government grant to fuel your latest innovation, have you inadvertently signed away your right to further tax relief? It's a question that keeps many financial directors awake, especially with the 2026 compliance landscape looking more rigorous than ever. The reality is that claiming R&D tax credits for subsidised projects isn't forbidden; it's simply a matter of choosing the correct legislative path. Whether you're utilising the Merged R&D Scheme or the Enhanced R&D Intensive Scheme (ERIS), external funding doesn't have to be a barrier to capital recovery.

We understand the frustration of feeling penalised for being proactive with your funding strategy. You've done the hard work of securing investment, and now you want to ensure every penny of qualifying expenditure is accounted for correctly. This guide provides the clarity you need to master these complexities under the latest HMRC rules. We'll break down the 20% gross credit rate for the merged scheme, the 30% intensity threshold for ERIS, and the vital steps to ensure your 2026 filings remain entirely compliant and secure.

Key Takeaways

- Understand how the transition to the Merged R&D Scheme for periods starting after 1 April 2024 simplifies the landscape for businesses receiving external support.

- Master the nuances of claiming R&D tax credits for subsidised projects to ensure you don't miss out on capital recovery due to grants or third-party funding.

- Learn to distinguish between notified state aid and commercial subsidies to protect your claim from HMRC enquiries and the "double dipping" trap.

- Identify "hidden" subsidies within commercial contracts where customer-funded costs might impact your eligibility for specific relief rates.

- Discover how a forensic technical assessment can transform your financial returns into strategic assets whilst maintaining total compliance with the latest HMRC manuals.

Defining Subsidised R&D Under Modern HMRC Rules

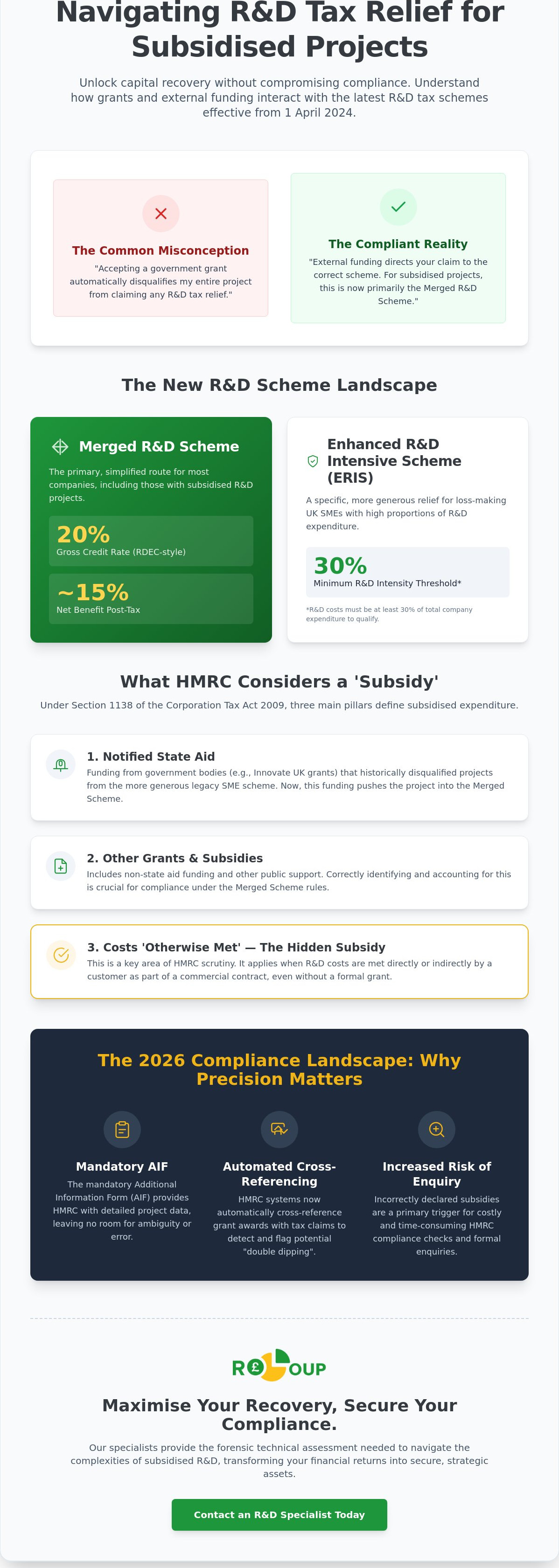

Many business leaders believe that accepting a grant is a binary choice; you either take the upfront funding or you claim the tax relief later. This is a misconception that can cost your business thousands in untapped capital. In the 2026 compliance environment, the presence of a subsidy doesn't automatically disqualify your innovation. Instead, it acts as a signpost, directing your claim toward the specific legislative pathway that ensures you remain compliant whilst maximising your return.

HMRC's definition of subsidised expenditure has evolved significantly to keep pace with modern corporate finance. They aren't just looking for a cheque from Innovate UK. They're looking at the economic reality of who is ultimately bearing the financial risk of the research. In 2026, HMRC scrutinises these projects more heavily because the transition to the Merged R&D Scheme has changed how different types of funding interact with your tax return. The goal is to prevent "double dipping" where a company might receive both a direct grant and the full SME-style relief on the same pound of expenditure.

The Legal Framework: Section 1138 and Beyond

Within the broader context of the UK R&D Tax Credit Scheme, Section 1138 of the Corporation Tax Act 2009 serves as the foundation for these rules. It identifies three distinct pillars of subsidies: Notified State Aid, non-state aid grants, and costs that are "otherwise met" by a third party. This third pillar is often the most contentious. It includes the "met directly or indirectly" clause, which captures scenarios where a customer pays for the R&D as part of a commercial contract.

HMRC's updated manuals make it clear that if your project costs are covered by a client, even without a formal grant agreement, that expenditure is considered subsidised. Subsidised R&D is defined as any research activity where the associated costs are met directly or indirectly by a person other than the claimant company; a distinction that now dictates the specific mechanics of your claim under the 2026 Merged Scheme.

Why Subsidies Matter for Your Corporation Tax Return

Correctly claiming R&D tax credits for subsidised projects requires a granular look at your ledger. Filing under the wrong scheme or failing to declare a subsidy can trigger an enquiry, especially now that the Additional Information Form (AIF) is a mandatory requirement for all submissions. HMRC uses the data from these forms to cross-reference grant awards with tax claims, leaving little room for error.

By treating your R&D claim as part of a wider innovation funding strategy, you can balance grants and tax relief effectively. Under the Merged Scheme, the net benefit sits at approximately 15% for most companies. This creates a stable environment where you can plan long-term research without fearing that a new grant will collapse your entire tax strategy. It's about precision and partnership, ensuring your technical advancements translate into tangible financial assets.

How Grants and State Aid Impact Your Innovation Funding

Securing a grant is often a milestone for any growing business. However, the type of funding you accept dictates the ceiling of your future tax relief. When managing R&D tax credits for subsidised projects, the distinction between Notified State Aid and other forms of support is paramount. Historically, the UK system was binary; if you received even a nominal amount of Notified State Aid for a project, that entire project was disqualified from the more generous SME scheme. While the 2026 rules under the Merged Scheme have softened this impact, understanding the legacy of these rules is vital for businesses filing for earlier accounting periods.

HMRC's scrutiny of grant-funded projects has intensified as they look to ensure that companies aren't claiming for costs that have already been covered by the taxpayer. This doesn't mean you should avoid grants. It simply means your documentation must be robust enough to withstand a compliance check. By categorising your funding correctly from the outset, you can protect your claim's integrity and ensure you're accessing the maximum relief available under the latest legislative framework.

Notified State Aid: The SME Scheme "Deal-Breaker"

Under the old dual-scheme system, Notified State Aid was a notorious hurdle. Because the SME scheme itself was considered State Aid, EU regulations prevented "cumulation", effectively banning businesses from receiving two types of State Aid for the same expenditure. This created the "all or nothing" rule. If you accepted a £5,000 Smart Grant, you might have lost tens of thousands in SME relief, forced instead to claim via the lower-rate RDEC. You can find more detail on these historical scheme differences on our R&D tax credits explained page. For 2026 filings, the Merged Scheme offers a more unified approach, though the categorisation of your funding still influences your overall innovation funding strategy.

De Minimis Aid and Non-State Aid Grants

Not all government money carries the "State Aid" tag. De Minimis aid, which refers to small amounts of support that don't distort competition, is treated differently. HMRC typically allows you to claim the unsubsidised portion of your R&D project through the SME scheme for older periods or the Merged Scheme today. Similarly, grants from local councils or private sector subsidies don't usually trigger the same "deal-breaker" rules as Notified State Aid. It's also worth considering how your capital allowances interact with these grants; if a grant pays for a piece of R&D equipment, you cannot claim the same cost twice. According to HMRC's definition of subsidised expenditure, any funding that meets your costs directly or indirectly must be carved out of your qualifying expenditure.

How do you know if your grant is Notified State Aid? Use this quick checklist:

- Does the grant offer letter explicitly mention "State Aid" or "GBER"?

- Was the funding provided by a national body like Innovate UK?

- Is the grant intended to incentivise a specific type of research?

- Does the award exceed the De Minimis threshold (usually €300,000 over three years)?

If you're unsure about your funding's status, speaking with a specialist can provide the clarity needed to protect your claim's value whilst maintaining full compliance.

Navigating the Merged R&D Scheme vs Historical SME Rules

The transition to the Merged R&D Scheme for accounting periods starting on or after 1 April 2024 represents the most significant shift in the UK tax landscape for a generation. For years, businesses had to grapple with two distinct sets of rules, often finding themselves penalised for being proactive in securing grant funding. In 2026, the landscape is far more unified. The old "all or nothing" barrier, which forced subsidised projects into the less generous RDEC scheme, has been dismantled for most claimants. This change allows for a more streamlined approach to innovation funding, though it requires a deeper understanding of how "above-the-line" credits interact with your financial statements.

The 2026 Merged Scheme Landscape

Under the current framework, most companies now claim a taxable expenditure credit. This credit is calculated as a percentage of your qualifying R&D costs and is recognised as income in your accounts, rather than just a reduction in your tax liability. This visibility is helpful for loss-making firms, as it provides a clear metric of R&D value on the balance sheet. However, with this transparency comes a higher demand for digital precision. As discussed in our guide on HMRC R&D Tax Claim Transparency and AI, the move toward mandatory digital filing means your data must be beyond reproach from the moment of submission.

| Scheme Type | Gross Credit Rate | Typical Net Benefit |

|---|---|---|

| Merged R&D Scheme | 20% | 15% - 16.2% |

| ERIS (R&D Intensive) | 186% Total Deduction | ~27% |

Accounting for Subsidies in the Merged Era

When managing R&D tax credits for subsidised projects, the primary task is "netting off" the expenditure. If a project costs £100,000 and you receive a £30,000 grant, you generally claim the credit on the remaining £70,000. It is vital to maintain contemporaneous records that clearly show which costs were met by which funding stream. This prevents overlap and ensures that the PAYE and NIC caps, which limit the payable credit to £20,000 plus 300% of relevant liabilities, are calculated accurately.

For those qualifying for the Enhanced R&D Intensive Scheme (ERIS), the rules are even more favourable. If your R&D expenditure exceeds 30% of your total expenditure, you can access the higher 27% benefit even if your projects are subsidised. In 2026, the Merged Scheme simplifies the R&D landscape by treating subsidised and non-subsidised expenditure with a unified RDEC-style credit for most firms. This creates a more predictable environment for long-term planning, allowing you to focus on technological breakthroughs rather than legislative loopholes.

Subcontracting and Customer Funding: The 'Hidden' Subsidy Trap

The most frequent misconception we encounter in 2026 is the belief that if a business hasn't received a formal grant, their R&D cannot be considered subsidised. This is a dangerous assumption that can lead to significant compliance risks. HMRC's lens is much broader; they're looking for any scenario where the costs of your innovation are "met directly or indirectly" by another person. This means your standard commercial contracts could be the very thing that triggers the rules for R&D tax credits for subsidised projects, even without a penny of public funding involved.

The landmark case of Quinn (London) Ltd v HMRC remains a vital touchstone for this discussion. In that instance, the tribunal ruled that a commercial payment for a finished product shouldn't automatically be treated as a subsidy for the R&D that created it. While this was a victory for the taxpayer, HMRC has since refined its approach. In 2026, the focus has shifted toward the specific wording of your agreements. If your contract stipulates that a client is paying you to solve a specific technical uncertainty, HMRC may argue that the client is the one truly funding the R&D activity.

When Your Client Funds Your Innovation

Identifying "hidden" subsidies requires a forensic look at your commercial agreements. A major red flag is when a contract is structured so that the financial risk of the R&D sits with the customer rather than your business. If your payment is contingent on achieving a specific technological breakthrough, or if the client retains all intellectual property rights from the outset, you're likely in subsidised territory. These nuances are often influenced by how your corporate finance is structured, as the visibility of project funding across your group can impact how HMRC perceives the "met" costs of your research.

The Construction Sector Challenge

Construction and engineering firms are frequently targeted for enquiries because their R&D is almost always intertwined with a specific client project. HMRC often argues that because the end client pays for the building or infrastructure, they're also paying for the R&D required to design it. To protect your claim, you must be able to distinguish between "business as usual" construction and the specific activities undertaken to resolve scientific or technological uncertainties. Practical tips for construction firms include:

- Ensure contracts separate the cost of standard delivery from R&D-specific consultancy.

- Maintain records that show your firm bore the financial loss if the R&D failed.

- Identify which technical uncertainties were resolved for your own firm's advancement, not just the client's brief.

Because these sector-specific traps are so complex, choosing a partner who understands the difference between a commercial sale and a funded research project is essential. You can learn more about this in our guide on R&D Tax Credit Specialists UK, which explores how to select an advisor who can navigate these regulatory hurdles whilst protecting your bottom line.

If you're concerned that your current customer contracts might be interpreted as subsidies, let us perform a no-cost assessment of your agreements to ensure your 2026 filings are built on solid ground.

Maximising Capital Recovery with Professional R&D Specialists

Managing R&D tax credits for subsidised projects requires more than just a standard accounting review. It demands a forensic technical assessment that bridges the gap between your engineering breakthroughs and HMRC's stringent 2026 manuals. At Recoup Capital, we don't just process paperwork. We act as a protective guide, scrutinising the interaction between your funding streams and your technical uncertainties to ensure no capital is left on the table. Our approach transforms a complex regulatory burden into a streamlined opportunity for business growth, ensuring that your technical narrative is as robust as your financial data.

Our success-based fee model ensures that our interests are perfectly aligned with your own. There is no upfront cost to explore your eligibility, making it a risk-free way to discover the true value of your innovation. This structure allows you to gain a clear understanding of your claim's potential without impacting your immediate cash flow or operational budgets. From initial discovery to final credit recovery, we provide end-to-end support, including direct liaison with HMRC should any questions arise. We believe in a relationship-first philosophy, positioning ourselves as long-term partners invested in your future innovation rather than just service providers.

The Recoup Capital Advantage: Why Specialist Support Matters

General accountants are excellent for day-to-day compliance, yet they often lack the technical depth required for complex subsidised R&D cases amongst diverse sectors. Our team includes chartered tax accountants who specialise in the nuances of the 2026 Merged Scheme and the Enhanced R&D Intensive Scheme (ERIS). We understand how to defend a claim before an enquiry even happens by building a robust technical narrative from the outset. This proactive stance is vital in an era where HMRC is using advanced data analytics to cross-reference grant awards with tax submissions. We ensure your Additional Information Form (AIF) is meticulously prepared whilst maintaining professional clarity and total transparency.

Next Steps: Reclaiming Your Innovation Capital

The journey to maximising your return begins with a low-friction, no-cost introductory consultation. We'll review your project history, grant award letters, and commercial funding agreements to identify untapped potential. Once we've identified your tax savings, we reframe them as strategic assets; capital that can be reinvested into your next breakthrough or used to scale your operations. This transformation from a tax refund to a strategic business tool is at the heart of what we do. Innovation shouldn't be stalled by regulatory confusion or the fear of "double dipping" with grants. Book a consultation with our R&D specialists today to secure your 2026 compliance and unlock the full value of your research.

Future-Proof Your Innovation Funding Strategy

The 2026 landscape demands a shift from reactive filing to proactive strategy. By understanding how the Merged R&D Scheme treats grants and commercial subsidies, you've already taken the first step toward safeguarding your innovation capital. Whether you're navigating the complexities of Notified State Aid or identifying hidden subcontracting traps in construction contracts, the goal is clear: total compliance without sacrificing your claim's value.

Navigating R&D tax credits for subsidised projects doesn't have to be a source of regulatory anxiety. Our team of chartered tax accountants brings specialised expertise to complex engineering and construction claims, ensuring your technical narrative aligns perfectly with HMRC's latest expectations. With our success-based fee model, you can explore your eligibility with complete confidence and zero upfront risk. It's time to turn your financial returns into strategic tools for long-term growth.

Secure your R&D tax relief with a specialised technical assessment from Recoup Capital. Your next technological breakthrough deserves a funding partner that understands the details as well as you do.

Frequently Asked Questions

Can I claim R&D tax credits if I received an Innovate UK grant?

Yes, you can still claim tax relief if you've secured an Innovate UK grant. Under the 2026 rules, you simply need to "net off" the grant amount from your total qualifying expenditure. This ensures you aren't claiming tax relief on costs already met by the taxpayer. It's a transparent way to balance direct funding with tax incentives whilst maintaining full compliance with HMRC's latest manuals.

How does the Merged R&D Scheme change how subsidies are treated?

The Merged R&D Scheme simplifies the process by dismantling the old "all or nothing" rule that previously pushed state-aided SMEs into the less generous RDEC scheme. Now, most companies receive a unified 20% gross credit on their unsubsidised R&D costs. This change provides greater certainty for businesses that utilise multiple funding streams, as the tax relief mechanism remains consistent regardless of whether a project is partially funded by a grant.

What happens if only part of my R&D project was subsidised?

If your project is partially subsidised, you only claim tax relief on the portion of the expenditure your company actually paid for. For example, if a £100,000 project received a £40,000 grant, you would calculate your credit based on the remaining £60,000. Accurate record-keeping is essential here to show exactly which costs were covered by the subsidy and which were met by your own internal funds.

Is Notified State Aid still a problem for R&D claims in 2026?

Notified State Aid is no longer the "SME scheme killer" it once was, but it still requires careful handling in 2026. For companies qualifying for the Enhanced R&D Intensive Scheme (ERIS), the 30% intensity threshold must be met regardless of subsidies. For everyone else, the Merged Scheme treats State Aid like any other subsidy, requiring you to deduct the funded amount from your claim whilst still accessing the 20% credit.

Can I claim R&D tax credits for work I was paid to do by a client?

You can often claim for client-funded work, but the contract wording is critical to determine if it counts as subsidised R&D. If your client meets the costs of the research directly or indirectly, HMRC will likely treat this as a subsidy. You must demonstrate that your firm still faced the technical uncertainty and bore the financial risk if the technological breakthrough wasn't achieved to protect the claim's integrity.

What is the difference between a subsidy and subcontracted R&D?

A subsidy is funding that meets your costs, whereas subcontracted R&D refers to who actually performs the research. If you pay a third party to resolve a technical uncertainty for you, that's subcontracting. If a client pays you to do the research, that's often a subsidy. The Merged Scheme has specific rules for both, so distinguishing between "who pays" and "who does the work" is vital for your 2026 filings.

How do I know if my grant is considered "Notified State Aid"?

Your grant award letter is the first place to look for references to "Notified State Aid," "GBER," or "State Aid" regulations. National funding bodies like Innovate UK typically provide this type of aid. If the grant is small and from a local authority, it might be "De Minimis" aid instead. In 2026, our specialists can review your funding agreements to ensure every pound is categorised correctly before you submit your return.

Will HMRC enquire into my claim if I declare a subsidy?

Declaring a subsidy doesn't automatically trigger an HMRC enquiry, but it does mean your Additional Information Form (AIF) must be beyond reproach. HMRC uses these forms to cross-reference grant databases with tax claims to prevent "double dipping." By providing a forensic breakdown of your R&D tax credits for subsidised projects, you demonstrate transparency and reduce the risk of a compliance check whilst securing your innovation capital.