Patent Calculator: Estimating Your UK Patent Box Tax Savings in 2026

What if the most daunting section of your tax return held the key to slashing your Corporation Tax bill by nearly 60%? It’s a reality many innovative UK firms overlook because the HMRC formula for Patent Box relief feels like a labyrinth designed to discourage the very innovation it aims to reward. You likely already feel that separating qualifying IP profits from your general revenue is a forensic challenge, which is why a precise patent calculator is essential to determine if the relief justifies the effort before you commit your team's time.

We’re here to show you that your intellectual property is a significant financial asset rather than a paperwork burden. This article will help you quantify your transition from the 25% main rate to a competitive 10% Corporation Tax rate for the 2026 fiscal year. We’ll outline the specific data required for a robust claim and provide a clear path to turning your technical breakthroughs into vital money for reinvestment. You’ll discover how to validate your IP’s worth and ensure your business thrives through strategic tax planning.

Key Takeaways

- Understand how the Patent Box scheme enables innovative UK businesses to reduce their Corporation Tax to just 10% on qualifying profits.

- Learn to navigate the multi-stage HMRC formula and use a professional patent calculator to estimate your potential savings for the 2026 tax year.

- Discover how to combine Patent Box claims with R&D Tax Credits to create a powerful funding strategy that supports your entire product lifecycle.

- Identify the critical data required for a successful claim, from UK IPO grant dates to auditing your Relevant IP Income (RIPI) from sales and licences.

- Recognise the importance of forensic accounting in identifying hidden qualifying income to maximise the capital available for your business’s future reinvestment.

What is a Patent Box Calculator for UK Businesses?

Is your business actually keeping the profit it deserves? For many innovative UK firms, the answer lies in a specific government incentive designed to reward home-grown brilliance. The UK Patent Box scheme allows companies to apply a lower rate of Corporation Tax to profits earned from their patented inventions. It's a powerful mechanism for financial recovery that many directors overlook.

Let's be clear about one thing. This is a corporate financial tool, not a sports betting "patent" wager. While a gambler uses a calculator to figure out returns on multiple horse racing bets, a patent calculator for business is designed to estimate tax relief on high-value intellectual property. It's about commercial strategy, not luck.

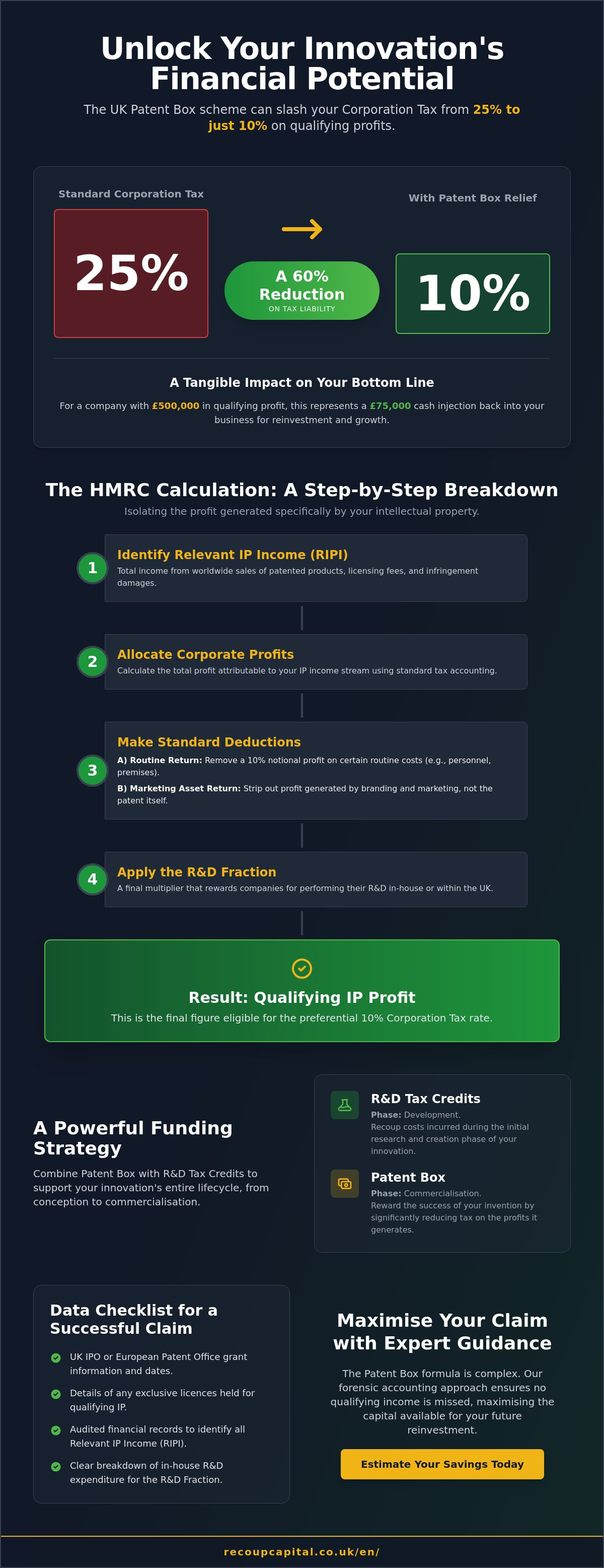

The calculation focuses on "Relevant IP Profit" (RP). This isn't just your total profit. It's a specific figure derived after removing routine returns and brand-related marketing assets. Since the main Corporation Tax rate rose to 25% in April 2023, the 10% Patent Box rate offers a massive 15% saving. That is money for reinvestment that can transform your growth trajectory and fund your next big breakthrough.

The Purpose of the Patent Box Scheme

The UK government introduced this incentive to ensure that brilliant ideas developed here stay here. It discourages companies from moving their intellectual property offshore to lower-tax jurisdictions. By rewarding the commercialisation phase, the scheme supports the entire lifecycle of innovation. It complements R&D tax credits, which cover the initial development costs. For a company with £500,000 in qualifying profit, the difference between the standard tax rate and the Patent Box rate represents a £75,000 cash injection back into the business. This isn't just a tax break; it's a strategic tool for scaling.

Who Should Use a Patent Box Tax Calculator?

Any limited company subject to UK Corporation Tax that makes a profit from patented products or processes should use a patent calculator. This includes:

- Firms holding qualifying patents granted by the UK Intellectual Property Office (IPO) or the European Patent Office (EPO).

- Businesses that have been granted an exclusive licence to use a patent, provided they meet the "active ownership" requirements set by HMRC.

- Companies looking to reinvest tax savings into further research and development to maintain their competitive edge.

If you're planning your 2026 budget, estimating these savings now is vital for accurate cash flow forecasting. At Recoup Capital, we act as your expert guide through these complexities. We're today's adviser and tomorrow's partner, helping you turn technical innovation into tangible financial success.

How the Patent Box Calculation Works: The HMRC Formula

The HMRC formula isn't a simple subtraction; it's a rigorous, multi-stage process designed to isolate the profit specifically generated by your intellectual property. Most companies start by identifying their Relevant IP Income (RIPI). This includes money earned from selling patented products, licensing fees, or even legal settlements related to patent infringement. Using a patent calculator helps simplify this, but you must understand the underlying mechanics to ensure your claim stands up to scrutiny.

A manual approach often leads to businesses either underestimating their potential return or overclaiming, which can trigger unwanted inquiries. The calculation follows a specific sequence: you determine your total profits, allocate them to the IP stream, and then apply several deductions to reach the "Relevant Profit." This ensures the tax relief only applies to the value added by the patent itself, rather than your general business operations or brand reputation.

Calculating Relevant IP Profit (RP)

To find your Relevant Profit, you must first remove the "Routine Return." HMRC assumes a 10% return on certain tax-deductible costs, such as personnel and premises, which they believe any business would earn regardless of having a patent. After this, you apply the "Marketing Asset Return" to strip away profits generated by your brand name or marketing efforts. This ensures the relief strictly rewards technical innovation. The Nexus Fraction is the ratio of in-house R&D expenditure to total R&D costs. This fraction acts as a final multiplier, rewarding companies that perform their own research and development within the UK. For a detailed breakdown of these requirements, you can consult HMRC's official guidance.

The 10% Tax Rate Application

The relief doesn't change your headline tax rate to 10% for the whole company. Instead, it functions as a deduction from your trading profits on your CT600 tax return. This deduction effectively reduces the Corporation Tax on your IP profits from the standard 25% to a lower 10% rate. It's a significant 15% saving that provides vital capital for reinvestment. Unlike a cash tax credit, this is a reduction in the tax you owe, though it can contribute to a loss that may be surrendered for a credit in specific circumstances. To see how these figures sit alongside other incentives, you can learn how to integrate tax credits into your return. Using an accurate patent calculator ensures these two distinct incentives work in harmony rather than conflicting. If you're unsure how these stages apply to your specific 2026 projections, a quick check of our frequently asked questions might provide the clarity you need.

Patent Box vs R&D Tax Credits: A Combined Approach

Understanding the distinction between R&D Tax Credits and the Patent Box is vital for any UK business looking to maximise its tax efficiency. Whilst R&D credits focus on the innovation phase, covering the costs of developing new products or processes, the Patent Box focuses on commercialisation. It provides a reduced corporation tax rate of 10% on profits derived from patented inventions. These two schemes don't just exist side-by-side; they're designed to work together to support the entire lifecycle of a product.

Using a Tax Foundation explanation of Patent Box helps clarify that this incentive aims to encourage companies to keep intellectual property within the UK. A common misconception is that claiming both constitutes "double-dipping." This isn't the case. HMRC regulations allow businesses to benefit from both, provided the claims are handled with precision. In fact, claiming R&D credits is a prerequisite for a high Nexus Fraction, which is the formula used to determine how much of your profit qualifies for the 10% rate. If you don't track your R&D expenditure accurately, your patent calculator results will likely show a significantly lower potential saving.

Synergising Your Tax Incentives

The smartest businesses use R&D tax credits to fund the initial, high-risk development of their technology. Once that technology is granted a patent, they transition into the Patent Box phase to protect their profit margins. This creates a seamless flow of capital. You can learn more about why claim both R&D and Patent Box to see how this strategy builds long-term resilience. By aligning these incentives, you ensure that every pound spent on innovation eventually contributes to a lower tax bill during the sales phase.

The Impact on Cash Flow and Reinvestment

The financial impact of combining these claims is substantial. In 2024, a mid-market engineering firm in Leeds managed to organise its tax strategy to claim both incentives, resulting in a total benefit of £185,000. This wasn't just a refund; it was "money for reinvestment" that allowed them to hire three new engineers and upgrade their favourite testing equipment. When you use a patent calculator to project your 2026 savings, you'll see how this capital can be used to outpace competitors. This strategic approach transforms tax from a mandatory cost into a tool for growth, helping your business thrive in a competitive global market.

- Innovation Phase: R&D Tax Credits provide immediate cash flow by offsetting development costs.

- Commercial Phase: Patent Box provides long-term tax relief on the resulting profits.

- Compliance: Maintaining a clear audit trail between R&D spend and patented IP is essential for HMRC approval.

Data Checklist: Preparing for Your Patent Calculation

Precision is the foundation of any reliable patent calculator result. To secure the 10% effective corporate tax rate, your data must be beyond reproach. HMRC expects a clear trail from the initial R&D expenditure to the final profit generated by the patented invention. Gathering this information early transforms a complex filing into a streamlined path toward significant tax savings.

Your first step involves the UK Intellectual Property Office (IPO). You need a definitive list of your qualifying patent numbers and their specific grant dates. Remember that the Patent Box relief only applies once a patent is granted, though you can backdate claims to the pending period once the certificate arrives. Beyond the IPO data, you must isolate your Relevant IP Income (RIPI). This isn't your total company turnover; it's the specific revenue generated from:

- The sale of products incorporating the patented invention.

- Licensing fees or royalties from third parties using your IP.

- Insurance or compensation proceeds related to the patent.

- The sale of the patent itself.

The most technical aspect of the checklist is the Nexus Fraction. This calculation ensures that the tax relief is proportionate to the R&D work actually performed by your company. You'll need to identify direct R&D expenditure, such as staff costs and consumables, and separate them from indirect costs like acquisition fees or R&D subcontracted to connected parties. Finally, you must apply a 10% routine return deduction to your qualifying profits, as HMRC assumes a portion of your success stems from standard business operations rather than pure innovation.

The Information You Need from Your Accountant

Your finance team is your greatest asset in this process. Ask them for profit and loss statements that are specifically segmented by product line or patent family. They should also provide detailed R&D project logs that align with your previous R&D tax credit claims. Consistency is vital; your Patent Box figures must reconcile with your CT600 filings to avoid unnecessary enquiries from HMRC.

Common Pitfalls in Data Gathering

A frequent error is failing to track R&D costs specifically related to the patented IP. If your R&D spend is "pooled" across the whole company, your Nexus Fraction may be diluted, which reduces your total tax saving. Another hurdle is the Marketing Asset Return. Many businesses overvalue their brand name or logo whilst underestimating the technical value of the patent. If HMRC believes your profits are driven by your reputation rather than your technology, they'll demand a higher deduction from your claim.

Whilst a digital patent calculator provides a helpful estimate, expert-led data collection is always safer than relying on automated templates. Professional oversight ensures that every pound of "money for reinvestment" is accurately identified and protected. If you're ready to see how these figures impact your 2026 forecast, learn more about the R&D nexus today.

Beyond the Calculator: Maximising Your Claim with Recoup Capital

A patent calculator provides a vital baseline for your 2026 financial planning. However, it's just the first step. HMRC requirements are increasingly rigorous. Relying solely on a digital tool often leaves significant capital on the table. We've seen innovative firms miss out on substantial portions of their potential claim because they haven't identified every qualifying income stream. Forensic accounting uncovers these hidden opportunities. Our specialists look deep into your profit and loss statements to isolate IP-derived income that standard software might overlook. This ensures your submission is both maximised and compliant.

We act as today’s adviser and tomorrow’s partner. This means we don't just file a claim and disappear. We work to reduce friction throughout the entire process. The transition from your initial calculation to actual cash recovery should be seamless. By handling the technical heavy lifting, we allow your leadership team to focus on what they do best: innovating. Our goal is to transform a complex government process into a strategic opportunity for your business growth.

- Identify hidden income: We trace qualifying profits back to specific patents.

- Ensure compliance: Our reports meet the latest HMRC transparency standards.

- Strategic reinvestment: We view your tax savings as capital for future R&D.

The Value of Specialist Tax Consultancy

HMRC's focus on transparency means your submission must be airtight. Since the 2023 updates to tax administration, the level of detail required for innovative claims has escalated. Our team ensures full compliance with these evolving standards. We provide expert support for mid-market corporate transactions and precise IP valuations. This level of scrutiny protects your firm during potential inquiries. You can explore our corporate finance advisory services to see how we integrate tax efficiency into your broader business strategy.

Next Steps: Your Free 15-Minute Consultation

Moving from a patent calculator estimate to a robust, success-based claim is a straightforward process. During your initial assessment, a chartered tax accountant reviews your technical eligibility and financial data. We don't deliver traditional sales pitches. We prefer to demonstrate value through tangible results. This 15-minute conversation identifies the money for reinvestment your business is entitled to. It's the first step toward turning a calculation into cash. Book your free 15-minute consultation today and let’s secure your firm’s financial future together.

Transform Your Intellectual Property into Reinvestment Capital

Securing a 10% effective Corporation Tax rate on patent-derived profits isn't just about compliance; it's a strategic move to fuel future growth. Whilst a patent calculator provides a useful starting point for your 2026 projections, the true value lies in the forensic application of the HMRC nexus formula. Combining these savings with R&D tax credits can significantly increase the capital available for your next breakthrough, especially as the main rate of Corporation Tax remains at 25% for many profitable businesses.

At Recoup Capital, our chartered tax accountants specialise in navigating these complexities with forensic precision. We ensure every claim meets strict HMRC standards whilst identifying the synergies between your innovation and your tax strategy. You don't have to worry about upfront costs because we operate on a success-based fee structure. We're here to act as your protective guide through the labyrinth of UK tax law, proving why we're today's adviser and tomorrow's partner.

Get a professional estimate of your tax savings with a FREE 15-minute consultation

Your innovation deserves to be rewarded. Let's work together to turn your intellectual property into a powerful engine for business growth.

Frequently Asked Questions

What is the current Patent Box tax rate in the UK for 2026?

The Patent Box tax rate for 2026 remains fixed at 10% on all relevant intellectual property profits. This represents a substantial reduction from the main Corporation Tax rate, which stands at 25% for companies with profits exceeding £250,000. By applying this reduced rate, HMRC incentivises UK companies to keep their high-value IP and innovation within the country. It's a strategic way to retain more capital for future growth and product development.

Can I use a patent calculator if my patent is still "pending"?

You can use a patent calculator to estimate potential savings whilst your application is pending, but you only claim the relief once the patent is officially granted. HMRC allows you to elect into the scheme while the patent is in the "pending" phase. This ensures you can backdate the tax relief to the date the application was first filed. It's a proactive step that prepares your business for a cash injection once the grant is confirmed.

How does the Nexus Fraction affect my Patent Box calculation?

The Nexus Fraction acts as a multiplier that adjusts your tax relief based on the proportion of R&D expenditure your company actually performed. If you outsourced 30% of your development to a connected party, your fraction might decrease, which lowers the amount of profit eligible for the 10% rate. It ensures the benefit stays with the innovators. Calculating this correctly is vital to ensure your claim complies with the OECD's "modified nexus" approach for global tax transparency.

Is it possible to claim both R&D tax credits and Patent Box relief?

Your business can benefit from both R&D tax credits and the Patent Box scheme simultaneously. Whilst R&D tax credits focus on the expenditure side of innovation, the Patent Box rewards the commercial success of the resulting products. Combining these two incentives creates a powerful financial cycle. It turns your technical development costs into immediate tax savings and your eventual sales into long-term, low-tax revenue streams for reinvestment. Many companies use both to fund their next generation of products.

What happens if my company makes a loss while holding a patent?

If your company incurs a loss on its patent-related activities, those losses must be carried forward to offset against future Patent Box profits. You don't use these specific losses to reduce your main Corporation Tax liability on non-patent income. This "streaming" of profits and losses ensures the 10% rate applies only to the net success of your IP. It's a technical area where precise accounting prevents you from losing out on future tax benefits when the patent becomes profitable.

Do I need a specialist to calculate my Patent Box relief, or can my general accountant do it?

While any qualified accountant can technically submit a claim, using a specialist ensures you don't leave money on the table through missed expenditure or incorrect streaming. The calculation involves complex steps, including the removal of routine returns and brand equity value from your profits. A specialist acts as your protective guide, navigating HMRC's detailed requirements. This partnership-oriented approach minimises your risk whilst maximising the capital available for your business to thrive and innovate.

What types of IP qualify for the Patent Box scheme in the UK?

Qualifying IP includes patents granted by the UK Intellectual Property Office, the European Patent Office, or specific EEA member states. Beyond standard patents, the scheme also covers plant breeders' rights and certain medicinal or botanical protection certificates. If your business holds an exclusive licence to use a patent owned by another entity, you might also qualify for the 10% rate. This breadth allows various sectors, from tech to agriculture, to access vital tax relief for their inventions.

How far back can I backdate a Patent Box claim?

You can generally backdate a Patent Box claim for up to two years from the end of the relevant accounting period. This window allows you to recover tax paid on profits generated whilst your patent was still pending, provided you elected into the scheme at the right time. Our team helps you identify these opportunities, ensuring you don't miss out on historical savings. It’s a seamless way to bolster your current cash flow using your past innovation success.