How are R&D Tax Credits Calculated? The 2026 UK Business Guide

Applying a flat percentage to your general ledger isn't a calculation; it's a gamble with HMRC that your business cannot afford to lose. Since the introduction of the Merged Scheme and Enhanced R&D Intensive Support (ERIS) for accounting periods beginning on or after 1 April 2024, the path to financial recovery has shifted. It's entirely natural to feel a sense of confusion when determining exactly how are R&D tax credits calculated whilst trying to distinguish between qualifying and non-qualifying costs.

We understand that the requirement for a Mandatory Additional Information Form, which became compulsory on 8 August 2023, adds a layer of pressure to get the numbers right the first time. This guide will help you master the complexities of the current system to calculate your claim value with forensic precision. You'll gain a clear understanding of the 20% taxable credit rate and the 30% intensity threshold for loss-making SMEs. We'll provide a repeatable framework for identifying expenditure, ensuring you can claim your money for reinvestment with total confidence in your final figure.

Key Takeaways

- Understand why the Merged Scheme is now the primary vehicle for UK innovation and how "above-the-line" credits impact your financial recovery.

- Master exactly how are R&D tax credits calculated by following a step-by-step framework that moves from basic data collection to forensic cost identification.

- Learn to distinguish between direct R&D and Qualifying Indirect Activities (QIAs) to ensure every pound of eligible expenditure is included in your claim.

- Identify whether your business qualifies for the 20% gross credit under the Merged Scheme or the enhanced support available for R&D-intensive loss-making SMEs.

- Discover how to mitigate HMRC enquiry risks and avoid the high opportunity cost of under-claiming by identifying nuanced qualifying costs.

The 2026 Framework for UK R&D Tax Credit Calculations

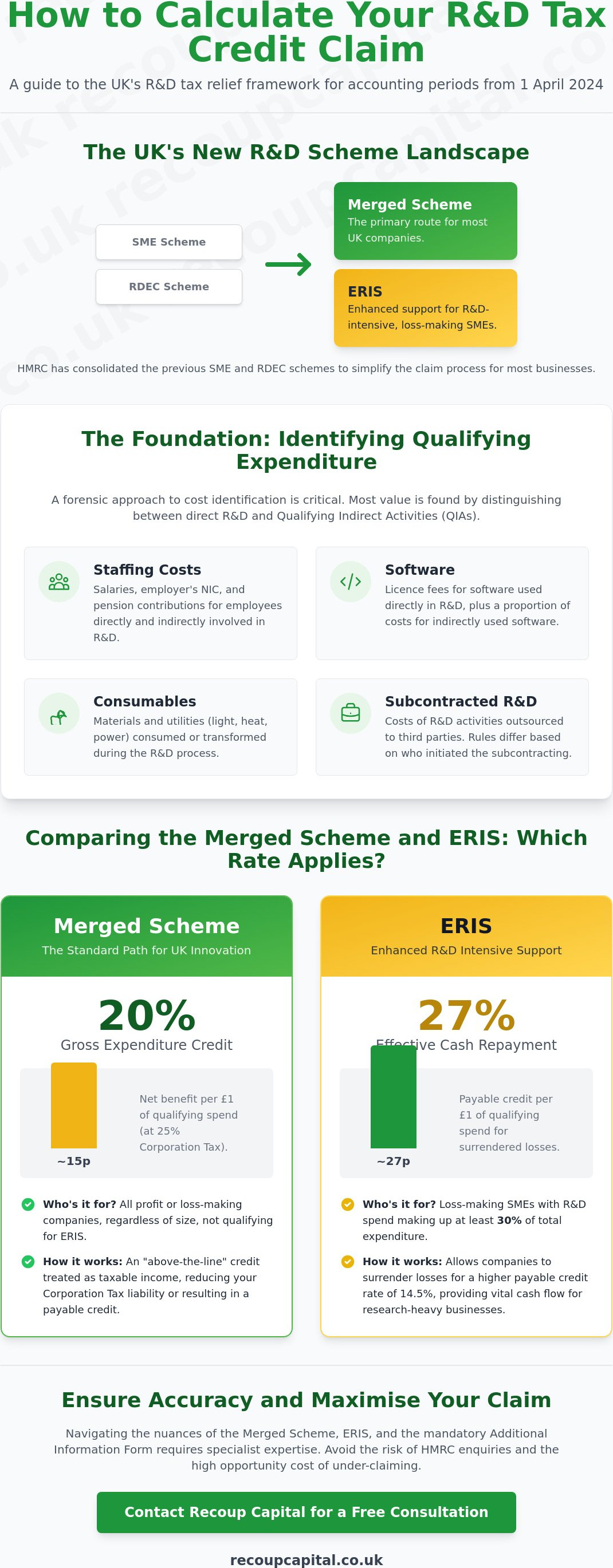

The legislative dust from the 2024 reforms has finally settled. By 2026, the Merged Scheme has become the bedrock of the UK R&D tax incentive landscape, providing a unified path for most businesses. This consolidation moved away from the fragmented SME and RDEC dual-track system, aiming to simplify how claims are processed and audited. Understanding how are R&D tax credits calculated begins with identifying which of the two primary pathways your company falls into. For most, this will be the Merged Scheme; however, for loss-making, research-heavy firms, the Enhanced R&D Intensive Support (ERIS) remains a vital lifeline. If you're unsure which path fits, reviewing how R&D tax credits are explained by specialists can help clarify your position.

The transition to the Merged Scheme wasn't just about changing rates; it was about aligning the UK with international standards and creating a more robust environment for innovation. By 2026, we've seen that this stability allows businesses to plan their long-term R&D budgets with greater certainty. Knowing how are R&D tax credits calculated under this unified system allows finance directors to forecast cash flow more accurately, particularly when dealing with the strict two-year claim deadline.

Understanding the Merged Scheme Transition

HMRC consolidated the SME and RDEC schemes into a single framework to improve consistency and reduce the administrative burden on both the taxpayer and the tax office. The primary feature of this scheme is the 20% "above-the-line" expenditure credit. This terminology is vital because the credit is treated as taxable income in your accounts, directly impacting your pre-tax profit rather than just reducing your final tax bill. For a company paying the 25% corporation tax rate, the net benefit sits at approximately 15% of qualifying spend. The Merged Scheme is the standard for all accounting periods starting on or after 1 April 2024.

Who Qualifies for ERIS in 2026?

The ERIS framework is designed specifically for loss-making SMEs where innovation is the core driver of the business. To qualify, your company must meet specific criteria:

- Intensity Threshold: Your qualifying R&D expenditure must be at least 30% of your total relevant expenditure for the period.

- SME Status: You must have fewer than 500 employees and either a turnover under €100 million or a balance sheet under €86 million.

- Financial Position: The company must be in a loss-making position to surrender losses for the 14.5% credit rate.

Startups in the biotech or deep-tech sectors often find ERIS more favourable than the Merged Scheme. It provides a higher enhancement for those prioritising research over immediate profit, allowing for significant money for reinvestment. This higher rate of recovery is a strategic tool, allowing intensive firms to extend their runway whilst they focus on high-risk technical breakthroughs.

Identifying Qualifying Expenditure: The Foundation of Your Calculation

Before you can work out your R&D tax relief, you must establish a bedrock of qualifying expenditure. It's the most critical stage in determining how are R&D tax credits calculated for your specific business. Most companies fail here because they treat it as a high-level accounting task rather than a forensic audit. A forensic approach ensures you capture every pound whilst protecting yourself from HMRC enquiries. To understand the full scope of what you can include, you might find our R&D tax credits explained guide helpful.

Distinguishing between direct R&D and Qualifying Indirect Activities (QIAs) is where the real value is found. Direct R&D covers the hands-on technical work, but QIAs include essential support functions. These might include HR, technical lead administration, and project management that directly facilitate the innovation. Identifying these requires a deep dive into your business's daily operations to ensure no eligible cost is left on the table. If you're unsure which costs qualify, a quick review of our FAQs provides instant clarity.

Staffing and Externally Provided Workers (EPWs)

Staffing costs usually form the largest part of any claim. When looking at how are R&D tax credits calculated, you must include gross pay, employer's Class 1 NICs, and employer pension contributions. For employees who split their time between R&D and standard operations, you must calculate an "R&D fraction" based on actual time spent on qualifying tasks. If you use Externally Provided Workers (EPWs), remember the 65% statutory restriction applies to their costs. In 2026, software licences are firmly established as qualifying consumables, provided they are used for the R&D project.

Subcontracted R&D and the New 2024 Restrictions

The 2024 legislative shift introduced stricter rules for subcontracted R&D. The "Contractor vs Client" rule now dictates that the company who decides to initiate and bear the risk of the R&D is usually the one entitled to claim. This prevents double-claiming for the same activity. Additionally, overseas expenditure is now largely restricted unless the work couldn't physically be performed in the UK due to specific environmental or geographical factors. Capturing these nuances is vital to ensuring your calculation is both maximised and compliant with the latest HMRC standards.

Comparing the Merged Scheme and ERIS: Which Rate Applies?

Deciding which legislative pathway fits your business is the first major hurdle in mastering how are R&D tax credits calculated. Since the 2024 reforms, most UK companies now fall under the Merged Scheme, which provides a 20% gross expenditure credit. However, for those operating at the cutting edge of innovation with high research costs relative to total spend, the Enhanced R&D Intensive Support (ERIS) offers a more lucrative alternative. Understanding these nuances is essential for any business leader asking why claim R&D tax credits? when looking to fuel future growth. As discussed in our look at HMRC R&D Tax Claim Transparency and AI, precision in choosing your scheme is now a non-negotiable part of compliance.

Calculating the Net Benefit of the Merged Scheme

The Merged Scheme uses an "above-the-line" credit of 20%. This means the credit is added to your pre-tax profit and is itself subject to Corporation Tax. If your company pays the main rate of 25%, the net benefit is 15% of your qualifying spend. For smaller companies paying the 19% small profits rate, the net benefit increases slightly to 16.2%. This calculation remains consistent even when you expand your qualifying expenditure to include data and cloud costs, which are now standard inclusions in 2026. The math is simple: multiply your qualifying spend by 0.20, then subtract the tax due on that credit amount.

The ERIS Calculation for Loss-Making SMEs

ERIS is specifically designed for loss-making SMEs that meet the "R&D Intensity" threshold. To qualify in 2026, your qualifying R&D expenditure must be at least 30% of your total relevant expenditure. You calculate this intensity by dividing your qualifying R&D spend by your total relevant expenditure for the period. If you meet this 30% mark, you can claim an additional 86% deduction on your costs, on top of the standard 100% deduction. If this creates or increases a tax loss, you can surrender that loss to HMRC for a cash credit of 14.5%.

| Calculation Factor | Merged Scheme (25% Tax) | ERIS (Loss-making) |

|---|---|---|

| Qualifying Expenditure | £100,000 | £100,000 |

| Gross Credit/Deduction | £20,000 (Credit) | £186,000 (Total Deduction) |

| Final Cash Benefit | £15,000 | £26,970 |

This table illustrates why determining how are R&D tax credits calculated for your specific circumstances is so vital. The difference in cash recovery between the two schemes for a £100,000 spend is nearly £12,000. For a startup, this represents significant money for reinvestment that could fund a new hire or a critical piece of equipment. If your intensity sits near the 30% boundary, forensic cost identification becomes the difference between a standard claim and an enhanced recovery.

A Step-by-Step Guide to Calculating Your R&D Claim Value

Moving from theory to a precise final figure requires a structured approach. Understanding how are R&D tax credits calculated in practice means following a logical sequence that transforms raw data into a compliant HMRC submission. This process isn't just about the numbers; it's about building a story of innovation that stands up to scrutiny. If you're ready to start your journey, claiming R&D tax credits with an expert partner ensures every step is handled with institutional precision.

Sector-specific nuances are often where claims are either won or lost. In the construction industry, for example, the calculation might overlap with land remediation costs if the R&D involves developing new techniques for treating contaminated soil. Ensuring these costs aren't double-counted but are correctly attributed to the R&D project is a hallmark of a high-quality claim. Once your costs are aggregated, you apply the relevant 20% Merged Scheme rate or the ERIS enhancement discussed in the previous section.

Step 1 & 2: Cost Aggregation and Rate Application

Your journey begins with a meticulous extraction of costs from your general ledger. You'll need to categorise expenditure into staffing, software, consumables, and subcontracted work. For an engineering firm, this might include the cost of materials consumed during the testing of a new structural component, whilst a software company would focus on cloud computing and developer time. It's vital to apply the 65% statutory restriction to any Externally Provided Workers (EPWs) or subcontractors correctly. Grossing up for RDEC involves adding the credit value back into your taxable income to ensure the benefit is correctly reflected in your pre-tax profit figures.

Step 3 & 4: Subsidies and Tax Return Integration

One of the most significant 2024 rule changes involves the treatment of subsidies. Under the Merged Scheme, the presence of a grant or subsidy no longer automatically bars an SME from claiming under the more favourable terms, simplifying the calculation for many innovative businesses. You must ensure that the figures in your calculation align perfectly with the Mandatory Additional Information Form (AIF) required since 8 August 2023. This form is the bridge between your spreadsheet and HMRC's systems.

The final step is integrating these figures into your CT600 Corporation Tax return. This isn't merely a data entry task. You must prepare a robust technical narrative that explains the scientific or technological uncertainty you were trying to resolve. This narrative provides the context that justifies the financial figures. If you find the integration process daunting, a detailed explanation of R&D tax credits can help you understand how the financial and technical elements of your claim must work in harmony.

Beyond the Spreadsheet: Maximising Accuracy and Mitigating HMRC Risk

Understanding how are R&D tax credits calculated is only half the battle; the other half is ensuring those figures survive HMRC scrutiny. Whilst the math might seem settled once you have applied the 20% or 14.5% rates, the underlying data must be beyond reproach. Many businesses fall into the trap of over-claiming by including ineligible costs, which is a fast track to a time-consuming enquiry. Conversely, there is a massive opportunity cost in under-claiming. We often find that companies miss out on thousands of pounds in recovery because they failed to identify nuanced indirect activities. To avoid these common calculation pitfalls, you can check our FAQs for a breakdown of where most errors occur.

General accountants are excellent for broad compliance, but they often lack the forensic focus required for R&D. They might miss the technical lead's time spent on project planning or the administrative support that keeps a lab running. These are valid Qualifying Indirect Activities (QIAs) that should be part of your total expenditure. Our forensic audit approach ensures every eligible penny is captured, turning your tax return into a strategic tool for growth rather than a mere administrative burden.

The Risks of Inaccurate R&D Calculations

By May 2026, HMRC has significantly ramped up its use of AI to flag inconsistencies in R&D math across the CT600 and the Mandatory Additional Information Form. An enquiry isn't just a financial burden; it's a reputational risk that can stall future claims and trigger wider audits. This is why success-based fees are so effective for modern businesses. They align your consultant’s goals with your own, ensuring that accuracy is prioritised over simply inflating a claim figure. It’s about securing money for reinvestment that you can actually keep, without the fear of a clawback later.

Why a Specialist Partner is Essential in 2026

Choosing the right guide is about moving from a transactional relationship to a strategic one. At Recoup Capital, we live by the slogan "Today’s adviser, tomorrow’s partner." This means our chartered tax accountants don't just process paperwork; they act as protective guides through the complexities of tax law. In sectors like construction, we identify hidden R&D in bespoke structural solutions or innovative land remediation techniques that others might overlook. If you are looking for long-term security, reading about R&D Tax Credit Specialists UK will help you choose a partner capable of delivering compliant innovation.

Our goal is to make the entire experience seamless. We offer a FREE 15 minute consultation to help you determine if your current approach to how are R&D tax credits calculated is capturing your full potential. Don't leave your financial recovery to chance; ensure your innovation is rewarded with the precision it deserves.

Securing Your Innovation Strategy for 2026

Mastering the mechanics of the Merged Scheme and ERIS is the first step toward transforming your technical challenges into money for reinvestment. By identifying every pound of qualifying expenditure with forensic precision, you protect your business from HMRC scrutiny whilst maximising your financial recovery. Understanding how are R&D tax credits calculated ensures you don't leave vital capital on the table or risk the reputational cost of an enquiry. Our team of Chartered Tax Accountants specialises in the nuanced requirements of construction and engineering R&D, providing the expertise needed to navigate the 2026 legislative landscape.

We operate on a success-based fee structure, meaning we are fully invested in the accuracy and success of your claim. This partnership-led approach removes the pressure of traditional sales pitches and focuses entirely on delivering measurable results. It is time to move beyond the spreadsheet and secure the funding your innovation deserves. Book your FREE 15-minute R&D consultation with our specialists today. We are ready to act as today's adviser and tomorrow's partner, helping your business thrive in an increasingly competitive market.

Frequently Asked Questions

How do I calculate the 30% intensity threshold for ERIS?

You calculate the intensity threshold by dividing your qualifying R&D expenditure by your total relevant expenditure for the accounting period. This threshold was set at 30% for periods starting on or after 1 April 2024. Total relevant expenditure includes almost all P&L costs, such as rent and salaries; however, it excludes capital expenditure and dividends. Meeting this 30% mark allows loss-making SMEs to access the higher 14.5% surrender rate rather than the standard Merged Scheme credit.

Can I still claim R&D credits if my project was partially funded by a grant?

You can still claim for projects supported by grants under the Merged Scheme rules. Since 1 April 2024, the presence of state aid or subsidies no longer prevents a company from claiming the 20% expenditure credit. This represents a significant simplification from the old SME scheme, where grant-funded work was often pushed into the less lucrative RDEC framework. It allows more businesses to receive money for reinvestment regardless of their funding source.

What is the net benefit of the Merged Scheme for a company paying 25% Corporation Tax?

The net benefit is exactly 15% for companies paying the 25% main rate of Corporation Tax. This is because the 20% gross credit is taxable as income. When you subtract the 5% tax due on that credit, you are left with a 15% cash benefit. Understanding how are R&D tax credits calculated in this taxable context is vital for accurate cash flow forecasting and ensuring your final claim figure is realistic.

How are staffing costs calculated if an employee only spends 50% of their time on R&D?

You apply the "R&D fraction" to the employee's total qualifying remuneration. If an engineer spends 50% of their time on innovation, you include 50% of their gross salary, employer's Class 1 NICs, and employer pension contributions in your calculation. You don't include benefits in kind or dividends. This apportioning method must be supported by evidence, such as timesheets or project logs, to satisfy HMRC's forensic requirements during an audit.

Do I need to calculate R&D credits differently for subcontracted work in 2026?

You must focus on who directed the R&D activity under the "Contractor vs Client" rules. For most claims, the 65% statutory restriction still applies to the cost of the subcontracted work. However, the 2024 reforms clarify that the company that initiates the R&D and bears the financial risk is generally the one entitled to claim. Overseas subcontracting is now largely excluded unless the work could not physically be performed within the UK.

What happens if I make a mistake in my R&D tax credit calculation?

HMRC may initiate an enquiry which could lead to financial penalties or a total clawback of the credit. Since 8 August 2023, the Mandatory Additional Information Form has made it easier for HMRC to spot mathematical inconsistencies. Penalties for "careless" errors can range from 0% to 30% of the potential tax lost. Working with a specialist partner helps mitigate this risk by ensuring your calculations are forensic and compliant from the start.

Is the R&D Expenditure Credit (RDEC) taxable?

Yes, the R&D Expenditure Credit is treated as taxable "above-the-line" income. It is added to your pre-tax profit in your accounts, meaning it is subject to Corporation Tax at either the 19% or 25% rate. This treatment ensures that the credit is visible to investors and stakeholders on the face of the balance sheet. It distinguishes the current Merged Scheme from the old SME deduction which only reduced taxable profit.

Can I calculate R&D tax credits for previous years under the old SME scheme?

You can claim under the old SME scheme for any accounting period that began before 1 April 2024, provided you are within the two-year amendment window. For those earlier periods, you can still use the 86% additional deduction and the 14.5% surrenderable credit rate. This is a common part of how are R&D tax credits calculated for businesses that are just starting their claim journey and need to look back at previous innovation cycles.