Fintech R&D Tax Credit Claims: Maximising Innovation Relief in 2026

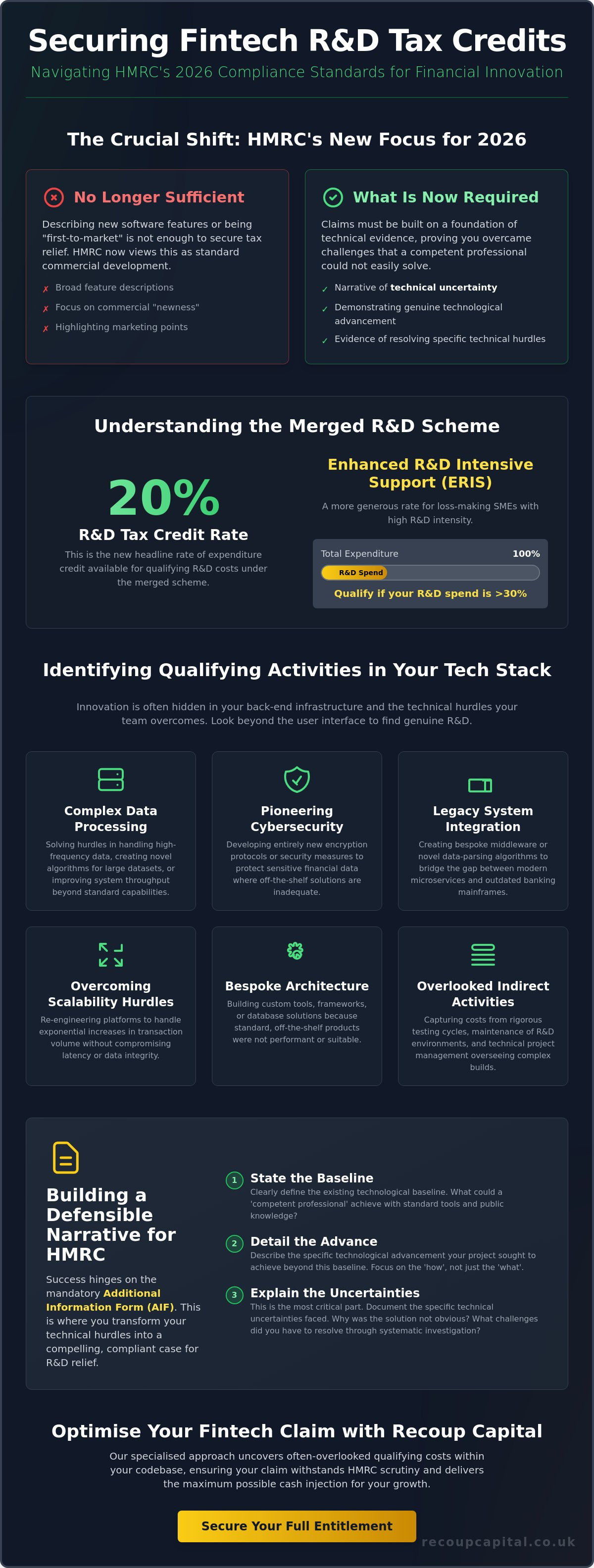

In 2026, describing your software features is no longer enough to secure your tax relief; HMRC now demands a narrative of technical uncertainty that most firms simply aren't prepared to write. You've likely felt the pressure of the Merged R&D Scheme and the increased scrutiny surrounding fintech R&D tax credit claims. It's understandable to feel uneasy about whether your latest algorithm or high-throughput platform truly meets the "competent professional" test, especially whilst HMRC enquiries are at an all-time high.

We understand that your priority is scaling your platform, not getting bogged down in tax legislation. This article reveals how to secure significant relief whilst navigating the latest HMRC compliance standards for software and financial innovation. You'll learn how to qualify for the 20% credit rate or the more generous Enhanced R&D Intensive Support (ERIS) if your R&D spend exceeds 30%. We will outline a streamlined approach to documentation that protects your engineering team's time and transforms your technical hurdles into strategic financial assets.

Key Takeaways

- Learn to distinguish between standard software features and the genuine technical advancements that HMRC now requires for a successful claim.

- Identify qualifying activities within your development cycle, such as solving complex data processing hurdles or pioneering cybersecurity protocols.

- Master the nuances of the 2026 Merged Scheme to ensure your fintech R&D tax credit claims provide the maximum possible cash injection for scaling.

- Understand the mandatory requirements for the Additional Information Form (AIF) to build a defensible narrative that withstands rigorous HMRC scrutiny.

- Discover how a specialised approach to your codebase can reveal eligible costs that are often overlooked by generalist providers.

Understanding Fintech R&D Tax Credit Claims in 2026

The UK fintech sector remains a global powerhouse of economic growth. It isn't just about flashy consumer apps or sleek user interfaces. Instead, the real value lies in the deep-tech infrastructure that powers modern finance. As we move through 2026, the opportunity for recovery remains vast, yet the path to securing it has changed. HMRC has significantly sharpened its focus, moving away from broad feature descriptions toward a rigorous examination of technical depth. Success now requires a clear distinction between commercial "newness" and genuine technological advancement.

The UK R&D tax incentive was originally designed to reward companies taking genuine technical risks. In the current climate, simply being "first to market" with a product doesn't guarantee a successful claim. You must demonstrate that your team encountered and overcame specific technical hurdles that couldn't be solved by a competent professional using standard, publicly available knowledge. This shift in scrutiny means that fintech R&D tax credit claims must be built on a foundation of technical evidence rather than marketing highlights.

The HMRC Definition of R&D for Financial Technology

For tax purposes, R&D takes place when a project seeks to achieve an advance in science or technology through the resolution of scientific or technological uncertainty. This definition is strict. A new marketing algorithm that improves customer acquisition might be commercially innovative, but it likely won't qualify if it uses established data science methods. Technical innovation, however, involves pushing the boundaries of what's possible, such as reducing latency in high-frequency trading platforms or creating entirely new encryption protocols. The "competent professional" test is the benchmark here. Your senior developers must be able to explain why the solution wasn't obvious and what technical uncertainties they had to resolve to reach the finish line.

Why Fintech Firms Frequently Under-claim

Many firms leave significant capital on the table because they assume their work is "standard" software development. This misconception often leads to missed opportunities. Beyond the core coding, businesses often overlook indirect activities that are entirely eligible for relief. This includes the time spent on rigorous testing, the maintenance of specialised R&D environments, and even the technical project management required to oversee complex builds. If your team is debating architecture or troubleshooting system integrations, you're likely performing qualifying work. Reading our guide on R&D tax credits explained can help you identify these often-ignored pockets of expenditure. By capturing the full scope of your engineering efforts, you transform your technical challenges into a strategic business asset.

Identifying Qualifying Activities in Financial Technology

Pinpointing eligible work within a complex codebase requires a shift in perspective. You shouldn't look at the final product, but rather at the technical dead ends and "trial and error" phases your developers endured. For fintech R&D tax credit claims, the most valuable narrative isn't the successful launch; it's the documentation of why a specific integration almost failed or why a standard database couldn't handle your throughput requirements.

Many firms overlook the sheer volume of qualifying work hidden in their back-end infrastructure. Whilst consumer-facing features are visible, the underlying architecture often contains the real innovation. This is particularly true when dealing with high-frequency data or distributed ledgers. Reviewing HMRC's software R&D case studies illustrates how technical challenges in data handling and system architecture form the backbone of a robust claim. If your team had to build custom tools because off-the-shelf solutions weren't performant enough, you're likely sitting on a significant claim opportunity.

Legacy Integration and Scalability Hurdles

Interfacing modern microservices with 40-year-old banking mainframes is a technical minefield. It isn't a simple matter of "plug and play." Your engineers frequently face technical uncertainty when trying to ensure data integrity and real-time synchronisation across incompatible architectures. This often involves creating bespoke middleware or novel data-parsing algorithms to bridge the gap. Scalability is another critical area. When a platform must be re-engineered to handle a 10x increase in transaction volume without a corresponding rise in latency, the solutions are rarely obvious. Documenting these phases of testing and refinement is essential for a defensible claim. If you're unsure if your integration work qualifies, you can check your eligibility here to see how these hurdles translate into relief.

Security, Encryption, and RegTech Innovation

The rise of privacy-focused finance has pushed technologies like Zero Knowledge Proofs into the mainstream. Developing these protocols involves resolving deep mathematical uncertainties that go far beyond standard library implementation. Similarly, creating fraud detection systems that leverage Machine Learning to identify anomalous behaviour in milliseconds requires significant technical experimentation. RegTech innovation is equally fertile ground. Automating complex regulatory compliance often requires overcoming significant technological gaps in how data is aggregated, verified, and reported across disparate international jurisdictions. These projects don't just solve business problems; they advance the technical state of the art in financial security.

Navigating the Merged Scheme and R&D Intensive Status

The 2026 tax landscape has undergone a significant transformation with the full implementation of the Merged Scheme. For most companies, the separate SME and RDEC paths are gone, replaced by a single, streamlined framework. This shift aims to simplify fintech R&D tax credit claims, yet it brings new nuances to how relief is calculated and captured. Understanding where your business sits in this new hierarchy is the first step toward turning your development costs into strategic assets. It isn't just about compliance; it's about ensuring your innovation is properly capitalised to fuel future growth.

The 2026 Regulatory Landscape for Fintech SMEs

For loss-making fintech startups, the Enhanced R&D Intensive Support (ERIS) remains a vital lifeline. To qualify as "R&D intensive" in 2026, your relevant R&D expenditure must be at least 30% of your total expenditure for the period. This threshold is often met by early-stage firms where developer salaries and cloud computing costs dominate the balance sheet. If you meet this 30% mark, you can access a more generous 14.5% payable tax credit. Failing to hit this ratio moves you into the standard Merged Scheme, where the taxable credit rate is 20%. Knowing which scheme applies is essential for accurate cash flow forecasting. You can explore why claim R&D tax credits to see how this capital can be reinvested into your next development sprint.

Contracted-out R&D: Who Claims the Credit?

Contracted-out work remains a complex area under the 2026 rules. Generally, the right to claim sits with the company that intended the R&D to take place. If your fintech firm hires an external software house to solve a specific technical uncertainty, you are typically the one eligible for the relief. However, the wording of your service agreements is now more critical than ever. You must ensure contracts clearly reflect that you are the risk-bearer and the initiator of the innovation.

When using Externally Provided Workers (EPWs), remember that you can usually only claim 65% of their costs. It's also important to note that for accounting periods beginning on or after 1 April 2024, costs for subcontractors based overseas are generally no longer eligible. Managing these details ensures your claim remains robust and defensible during HMRC's review of your mandatory Additional Information Form. By aligning your contracts with these regulatory requirements, you protect your firm's ability to recover vital capital whilst maintaining a transparent relationship with the tax authorities.

Building a Defensible Narrative for HMRC

The landscape of fintech R&D tax credit claims has shifted from a focus on financial figures to a demand for absolute technical transparency. Since the introduction of the mandatory Additional Information Form (AIF), the technical narrative is no longer a supplementary document; it is the core of your claim. HMRC now requires a granular breakdown of the technical uncertainties your team encountered, moving away from high-level commercial summaries toward detailed engineering logs. A successful claim in 2026 depends on your ability to prove that your work went beyond standard industry practice.

HMRC is increasingly wary of "boilerplate" descriptions that could apply to any software firm. To survive scrutiny, your narrative must be specific to your codebase and the unique hurdles of financial technology. This means move away from describing what the software does for the user and start explaining how the underlying technology was pushed to its limits. If your claim reads like a marketing brochure, it's likely to trigger an enquiry. Instead, focus on the technical "scars" of development, documenting the failed iterations and the complex problem-solving that eventually led to a breakthrough.

Documenting Systematic Investigation in Fintech

A "systematic investigation" is the methodical approach your engineers take to resolve a technical uncertainty. In the fintech space, this is rarely a linear path. Your Agile development logs, including Jira tickets, GitHub commits, and internal technical wikis, are essential pieces of evidence. These records show the evolution of a project, capturing the specific moments where standard libraries or existing protocols failed to meet your requirements. By linking these logs to your R&D tax credit submission, you provide a verifiable audit trail that demonstrates a structured attempt to advance the technical state of the art.

Avoiding Common Pitfalls in Software-Based Claims

One of the most frequent mistakes is claiming for routine maintenance or cosmetic UI/UX changes. Whilst these are essential for a polished product, they don't involve the resolution of technical uncertainty. Similarly, be cautious of using AI-generated narratives without expert oversight. HMRC has become adept at spotting generic, AI-produced text that lacks the nuance of a real engineering challenge. You must also be precise when apportioning staff time. Your developers likely spend a portion of their week on R&D and the rest on day-to-day operations; your claim must reflect this split with accuracy to remain defensible.

If you want to ensure your innovation is captured accurately without distracting your engineering team, you can start a professional assessment of your eligible activities to secure the relief your firm deserves.

Optimising Your Fintech Claim with Recoup Capital

Securing the maximum return on your innovation requires more than just a list of costs; it demands a partner who understands the binary complexities of your codebase as well as the fiscal intricacies of the Merged Scheme. At Recoup Capital, we don't just process paperwork. We act as a protective guide through the evolving regulatory landscape, ensuring your fintech R&D tax credit claims are both robust and optimised for growth. Our methodology is designed to identify the "hidden" R&D that often slips through the cracks of standard accounting practices, such as the technical uncertainties resolved during back-end architecture refactoring or complex API synchronisation.

Our partnership is built on a foundation of transparency and shared success. We operate on a success-based fee structure, which aligns our goals directly with your business growth. This approach ensures that we are fully invested in the accuracy and depth of your claim. From the initial technical assessment to the final HMRC submission, we provide a low-friction experience that minimises the burden on your engineering team. We speak the language of your developers and your finance team, bridging the gap between technical hurdles and financial recovery.

Why General Accountants Often Miss Fintech R&D

Generalist firms often struggle to translate high-level financial engineering into the specific language HMRC requires. They might see a successful platform launch where we see a series of resolved technological uncertainties. Because they lack the technical depth to recognise the R&D within complex financial architectures, they often leave significant relief on the table. By pairing our chartered tax accountants with technical specialists who have deep experience in fintech, we ensure no eligible expenditure is overlooked. This collaborative approach is a core part of claiming R&D tax credits with us, allowing your team to stay focused on the sprint whilst we handle the forensic documentation.

Your Strategic Partner for Long-Term Innovation

We view your tax relief not as a one-off refund, but as a strategic asset for your 2026 roadmap. This capital recovery provides the liquidity needed to accelerate development and scale your operations. Our commitment to a relationship-first approach means we provide rigorous forensic reporting that stands up to HMRC scrutiny, protecting your business from the stress of unexpected enquiries. We believe in demonstrating value through results rather than traditional sales pitches. If you're ready to transform your development hurdles into a primary driver of business value, you can speak with a Fintech R&D Specialist at Recoup Capital today.

Transforming Technical Debt into Strategic Capital

The 2026 landscape for fintech R&D tax credit claims is undeniably more complex, yet the potential for recovery has never been more significant for those who document their journey correctly. You've seen how identifying genuine technical uncertainty, from legacy integrations to novel RegTech algorithms, is the key to a defensible claim. By moving beyond simple feature descriptions and embracing the mandatory technical narratives required by HMRC, your firm can secure the cash injection needed to scale.

Our specialised team of Chartered Tax Accountants and technical experts is here to act as your protective guide. We understand the nuances of complex software and RegTech narratives, ensuring every eligible pound is captured whilst you focus on your product roadmap. With our success-based fee model, our goals are perfectly aligned with your long-term growth and stability.

Book a No-Cost Fintech R&D Claim Review to discover the hidden value within your codebase. Let's work together to turn your innovation into a powerful business tool and fuel your next phase of development.

Frequently Asked Questions

What qualifies as R&D in fintech software development?

Qualifying R&D occurs when your project seeks an advance in technology by resolving technical uncertainty. In the fintech sector, this often involves developing high-throughput platforms, creating advanced algorithms for real-time data processing, or building novel encryption protocols. It's important to remember that simply adding new "features" for a better user experience doesn't qualify unless the underlying development pushed the boundaries of current software engineering.

Can loss-making fintech startups claim R&D tax credits?

Yes, loss-making startups can receive a payable tax credit to provide a vital cash injection. Under the Enhanced R&D Intensive Support (ERIS) rules, eligible SMEs can claim a payable credit of 14.5% for their surrenderable losses. This ensures that even before your platform becomes profitable, your investment in innovation is recognised and rewarded by the tax system.

How far back can my fintech firm claim R&D tax relief?

You can generally submit fintech R&D tax credit claims for your two most recently completed accounting periods. This two-year window is a strict deadline, so it's essential to review your previous development cycles promptly. If you haven't claimed in the last three years, you may also need to submit a Claim Notification Form within six months of the end of the period you intend to claim for.

What is the "R&D Intensive" scheme for fintech SMEs?

The Enhanced R&D Intensive Support (ERIS) is a specific scheme for loss-making SMEs whose R&D expenditure is at least 30% of their total expenditure. This scheme is particularly beneficial for fintech firms with high developer costs and low initial revenue. It offers a total deduction of 186% on qualifying costs, which is significantly more generous than the standard Merged Scheme rate.

How does HMRC define "technical uncertainty" in financial services?

Technical uncertainty exists when a solution to a problem isn't readily deducible by a competent professional using publicly available information. In financial services, this might involve resolving latency issues in high-frequency trading or ensuring data integrity across incompatible legacy mainframes. If your senior engineers had to engage in a period of trial and error to find a viable solution, you've likely encountered qualifying uncertainty.

Do we need to provide code samples to HMRC for our R&D claim?

HMRC doesn't usually require raw code samples as part of your initial submission, but you must provide a detailed technical narrative. This narrative should explain the technological challenges and the systematic investigation your team performed. Whilst you don't need to share your entire codebase, having evidence like GitHub logs or architecture diagrams ready is vital if HMRC raises a specific enquiry.

How long does it take to receive the R&D tax credit payment?

HMRC typically aims to process most claims within 28 to 40 days of submission. However, this timeline can be extended if your claim is selected for a compliance check or if the Additional Information Form is incomplete. Working with a specialist ensures that your fintech R&D tax credit claims are structured correctly from the start, which helps maintain a brisk and efficient process.

Can we claim for R&D if we used a third-party software agency?

You can claim for costs associated with third-party software agencies, provided your firm is the initiator and risk-bearer of the R&D. Under the Merged Scheme rules for accounting periods starting after 1 April 2024, you can generally only claim for UK-based subcontractors. Costs for overseas developers are now largely excluded, so it's essential to review your supply chain to ensure your claim remains compliant.